Is Rackspace Technology (RXT) Above Fair Value After Its AMD AI Expansion Deal?

Rackspace Technology, Inc. RXT | 0.00 |

Rackspace Technology (RXT) is in focus after agreeing to source 30 MW of AMD GPU and CPU capacity across its global data centers from 2026 to 2028, while planning substantial workforce reductions.

Against this backdrop, Rackspace Technology’s share price has moved sharply, with a 30 day share price return of 45.90% and a very large 90 day gain. The 1 year total shareholder return of 376.81% contrasts with a 5 year total shareholder return that is still down 66.01%. This suggests momentum has picked up recently as investors reassess the company’s AI and cloud positioning and risk profile.

If Rackspace Technology’s AI push has caught your attention, this could be a good moment to see what else is moving in the space through 52 AI infrastructure stocks

Rackspace Technology now trades above both its analyst target of US$4.90 and an internal fair value estimate, after a sharp rebound from deeply negative 5 year returns. Is the market overreacting to the AI story, or still pricing in real risk?

Most Popular Narrative: 15.4% Overvalued

With Rackspace Technology last closing at $6.58 against a widely followed fair value estimate of $5.70, the current price already bakes in a rich narrative around its AI and cloud ambitions.

With deep, multifaceted partnerships across major hyperscalers and innovative AI firms, Rackspace is uniquely poised to access new, high-growth markets through joint go-to-market efforts, cross-selling, and first-mover advantages, driving robust top-line growth beyond what is currently reflected in guidance.

Curious what revenue path, margin uplift, and future earnings multiple have to line up to reach that fair value? The full narrative spells out a detailed earnings bridge, a specific profitability step up, and the pricing power assumptions behind it, but keeps some important tensions between growth and ongoing losses that are worth seeing in context.

Result: Fair Value of $5.70 (OVERVALUED)

However, Rackspace Technology still faces revenue pressure in both cloud segments and relies on cost efficiencies and vendor prepayments, which could challenge the bullish AI narrative.

Another View: Rackspace Technology Through a Sales Multiple Lens

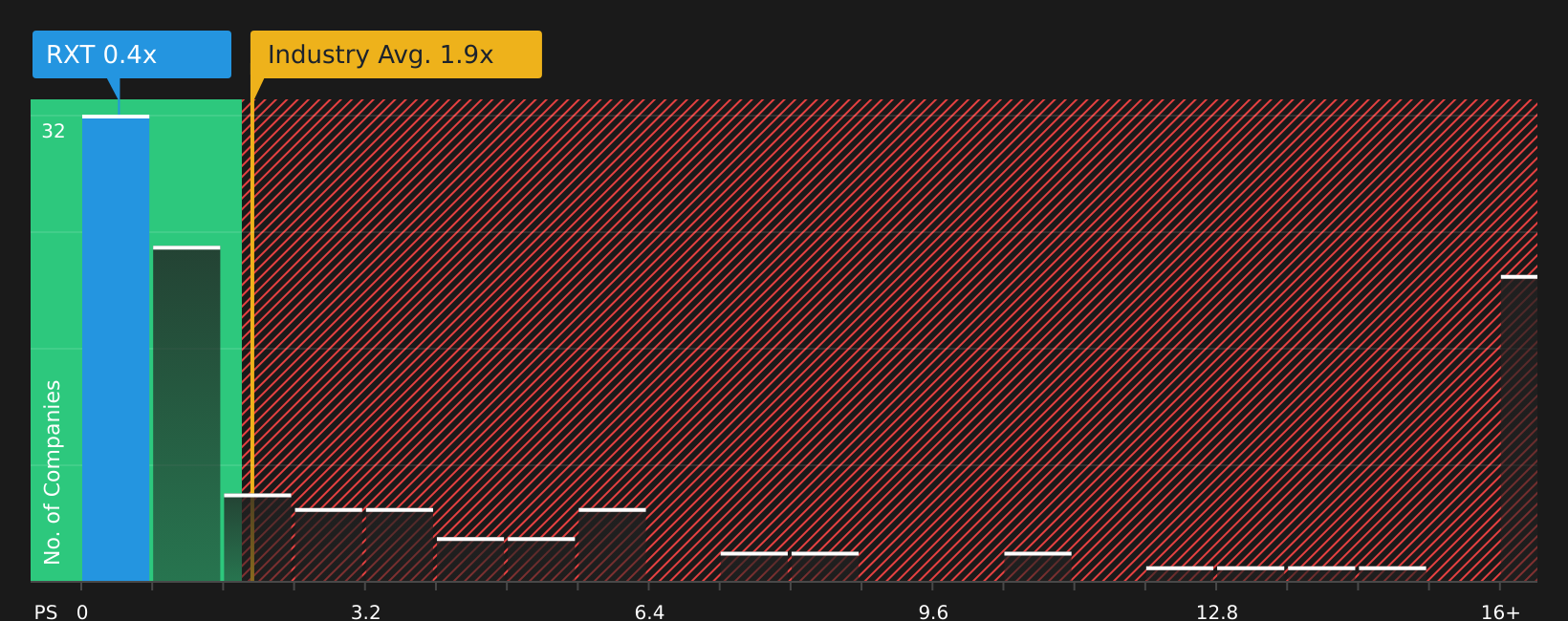

The narrative and fair value work around Rackspace Technology flag the stock as trading above a US$5.70 estimate, yet the market is still only paying a P/S of 0.6x compared with 1.9x for the wider US IT industry, a 25.8x peer average, and a 1.2x fair ratio.

If sentiment on Rackspace’s AI and cloud story holds or improves, could that gap to both peers and the fair ratio close, or is the current discount a sign that investors remain focused on losses, balance sheet strain, and forecast revenue growth of about 1.6% a year?

Next Steps

If the mixed sentiment around Rackspace Technology leaves you undecided, you may want to check the numbers for yourself and weigh both sides through 1 key reward and 4 important warning signs

Looking For More Investment Ideas Beyond Rackspace Technology?

Rackspace Technology might be front of mind today, but your next strong idea could come from casting the net a little wider using focused screeners on Simply Wall St.

- Spot potential mispricings early by checking companies that appear attractively valued with solid fundamentals through the 44 high quality undervalued stocks.

- Manage risk by focusing on companies with resilient finances using the 72 resilient stocks with low risk scores.

- Identify potential future standouts before they attract broader attention by scanning the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.