Is Rayonier’s Wider Q1 Loss Reframing the Earnings Growth Narrative for RYN?

Rayonier Inc. RYN | 0.00 |

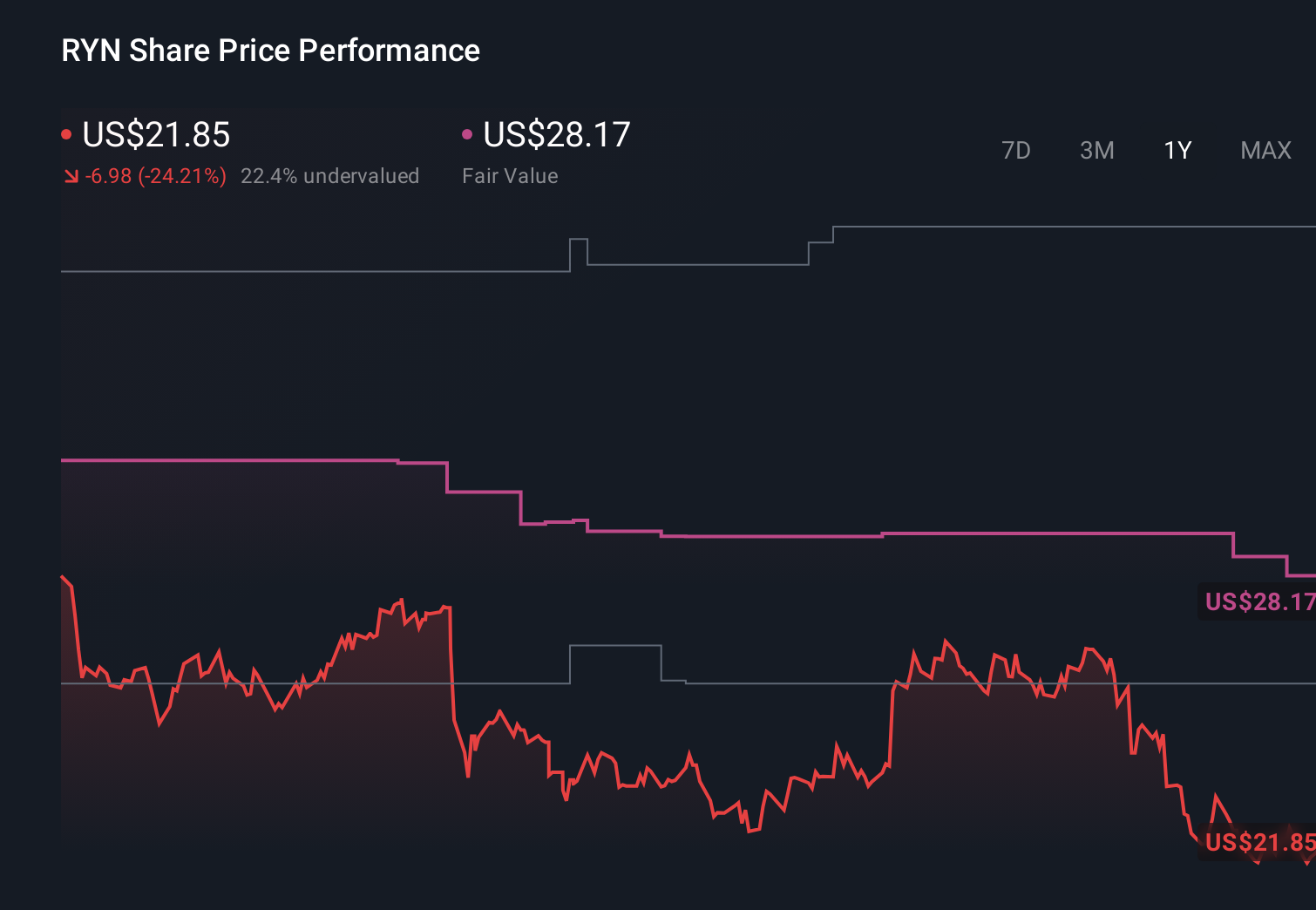

- Rayonier Inc. has reported results for the first quarter ended March 31, 2026, posting a net loss of US$12.4 million compared with US$3.4 million a year earlier, and a basic and diluted loss per share of US$0.05 versus US$0.02–0.04 previously.

- The widening loss highlights pressure on profitability at the start of 2026, raising questions about how current operations align with the company’s longer-term growth and diversification ambitions.

- We’ll now examine how this wider first-quarter net loss may affect Rayonier’s existing investment narrative around earnings growth and portfolio diversification.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Rayonier Investment Narrative Recap

To own Rayonier today, you need to believe in its timberland and wood products platform as a long term cash flow and asset value story, even as near term earnings remain bumpy. The wider Q1 2026 net loss of US$12.4 million puts extra focus on how quickly the merged Rayonier and PotlatchDeltic operations can stabilize profitability. Right now, the key near term catalyst is merger integration, while execution risk around combining two timber and wood products portfolios feels more pronounced after these results.

The most relevant recent development alongside this loss is the completion of the PotlatchDeltic merger in late January 2026, which reshaped Rayonier’s leadership and operating structure. With a new CEO, CFO, and expanded credit facilities of up to US$1,809.5 million, the investment case now leans heavily on whether integration efficiencies and scale benefits can offset current profitability pressure and support the company’s earnings and diversification ambitions over time.

Yet even as the merger promises cost and scale benefits, investors should be aware of how Rayonier’s higher timber concentration could amplify...

Rayonier's narrative projects $1.5 billion revenue and $255.1 million earnings by 2029. This requires 46.6% yearly revenue growth and a $187.0 million earnings increase from $68.1 million today.

Uncover how Rayonier's forecasts yield a $26.83 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Before this weak quarter, the most optimistic analysts were assuming revenue could grow about 49.7% a year and earnings reach roughly US$275.2 million, which is a much more upbeat story than the climate and demand risks many of us worry about. This latest loss may cause both the cautious and the bullish camps to revisit their assumptions, so it is worth comparing these very different views side by side.

Explore 7 other fair value estimates on Rayonier - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Rayonier research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Rayonier research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rayonier's overall financial health at a glance.

No Opportunity In Rayonier?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.