Is Restructuring Subsidiaries in Bermuda a Turning Point for International Seaways’ Efficiency Strategy (INSW)?

International Seaways, Inc. INSW | 0.00 |

- Earlier this month, International Seaways announced amendments to its existing credit facilities, enabling the redomiciliation of its vessel-owning and intermediate holding subsidiaries from the Marshall Islands and Liberia to Bermuda, with the process targeting completion by the end of the fourth quarter of 2025 and incurring between US$3 million and US$5 million in related costs.

- This corporate restructuring is intended to enhance operational and tax efficiency while giving the company greater flexibility for future strategic initiatives.

- We'll consider how International Seaways' move to redomicile key subsidiaries to Bermuda might influence its long-term operational and financial profile.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

International Seaways Investment Narrative Recap

To invest in International Seaways, you need to believe in the ongoing relevance of global crude and product tanker markets and the company’s ability to maintain earnings power despite sector volatility. The recent decision to redomicile vessel-owning subsidiaries may improve long-term flexibility, but it is not likely to materially impact the near-term catalyst of extended trade routes or the primary risk of energy transition-driven demand uncertainty.

Among recent developments, the October 2025 amendments to major credit facilities directly enabled the redomiciliation process and signaled a proactive approach in aligning the company’s structure with evolving operational requirements. This is closely linked to International Seaways’ need for agility as shifting refinery locations and regulations drive changes in global shipping patterns, a key source of recent demand.

Conversely, investors should note that accelerating global energy transition trends could reduce the need for tanker transport...

International Seaways is projected to achieve $848.0 million in revenue and $288.7 million in earnings by 2028. This outlook is based on annual revenue growth of 2.0% and represents a $50.1 million increase in earnings from the current $238.6 million.

Uncover how International Seaways' forecasts yield a $53.50 fair value, a 16% upside to its current price.

Exploring Other Perspectives

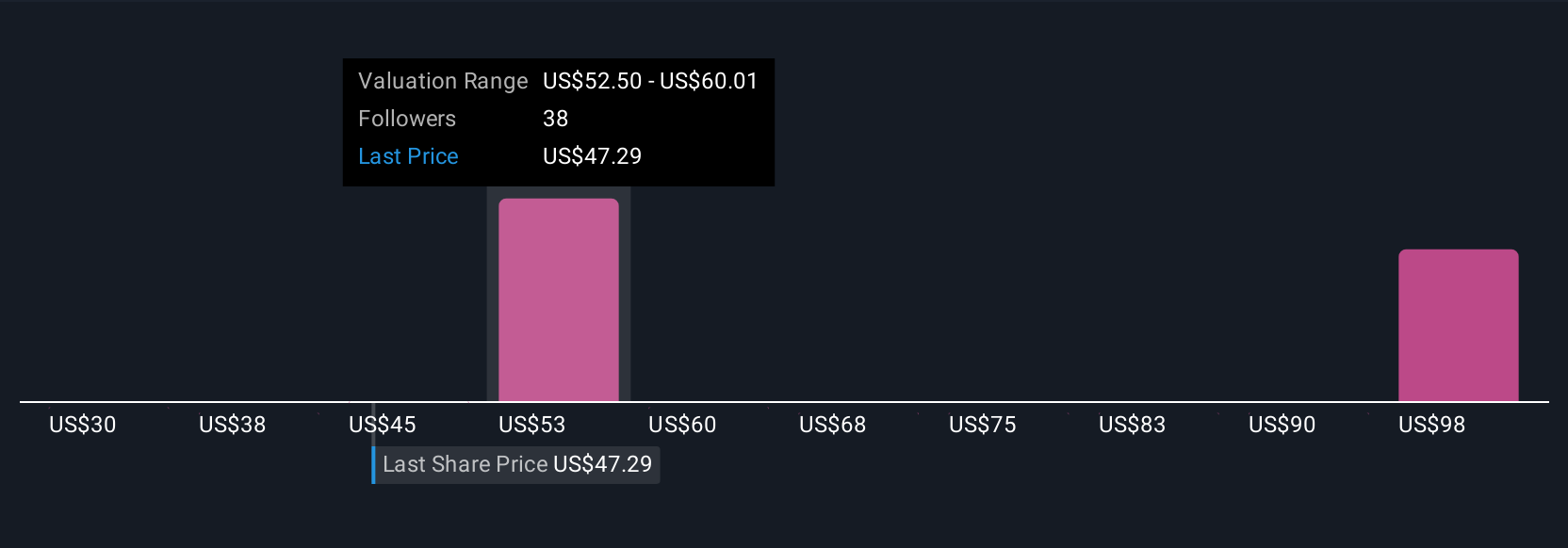

Simply Wall St Community members have provided five fair value estimates for International Seaways, ranging from US$30 to US$64 per share. While forecasts for extended shipping routes support utilization, opinions differ widely, inviting you to explore alternative viewpoints.

Explore 5 other fair value estimates on International Seaways - why the stock might be worth as much as 39% more than the current price!

Build Your Own International Seaways Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your International Seaways research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free International Seaways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Seaways' overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.