Is Royal Caribbean (RCL) Using Alaska Port Upgrades to Quietly Redefine Its Competitive Moat?

Royal Caribbean Group RCL | 0.00 |

- Earlier this week, Royal Caribbean Group and partners marked the opening of the Dale R. and Carol Ann Lindsey Alaska Railroad Terminal in Seward, now the largest cruise terminal in Alaska with modernized facilities, shore power, and direct rail connectivity to Anchorage and Fairbanks.

- By combining enhanced passenger flows, cleaner-energy pier infrastructure, and year-round community use, the new Seward terminal underscores how port investments can support both operational efficiency and broader regional development.

- We’ll now explore how this new Alaska terminal, with its shore power and capacity upgrades, may influence Royal Caribbean’s investment narrative.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean today, you need to believe in durable cruise demand, disciplined capacity growth, and the company’s ability to convert high occupancy into healthy margins despite a macro backdrop that still leans on consumer discretionary spending. The new Seward terminal appears directionally positive for operational efficiency and brand positioning, but it is unlikely to shift near term catalysts like booking trends or key risks such as sensitivity to fuel costs and broader economic conditions in a material way.

The Seward terminal opening also sits alongside Royal Caribbean’s continued investment in new hardware, including the recent delivery of Legend of the Seas as the third Icon Class ship. Together, these moves point to a focus on enhancing guest experience and port infrastructure, which ties directly into catalysts around onboard spending, yield management, and moderating capacity growth, while still leaving the company exposed to swings in demand and input costs that investors should monitor closely.

Yet even as these projects advance, investors should be aware of how rising regulations and potential carbon costs could eventually reshape Royal Caribbean’s cost base and...

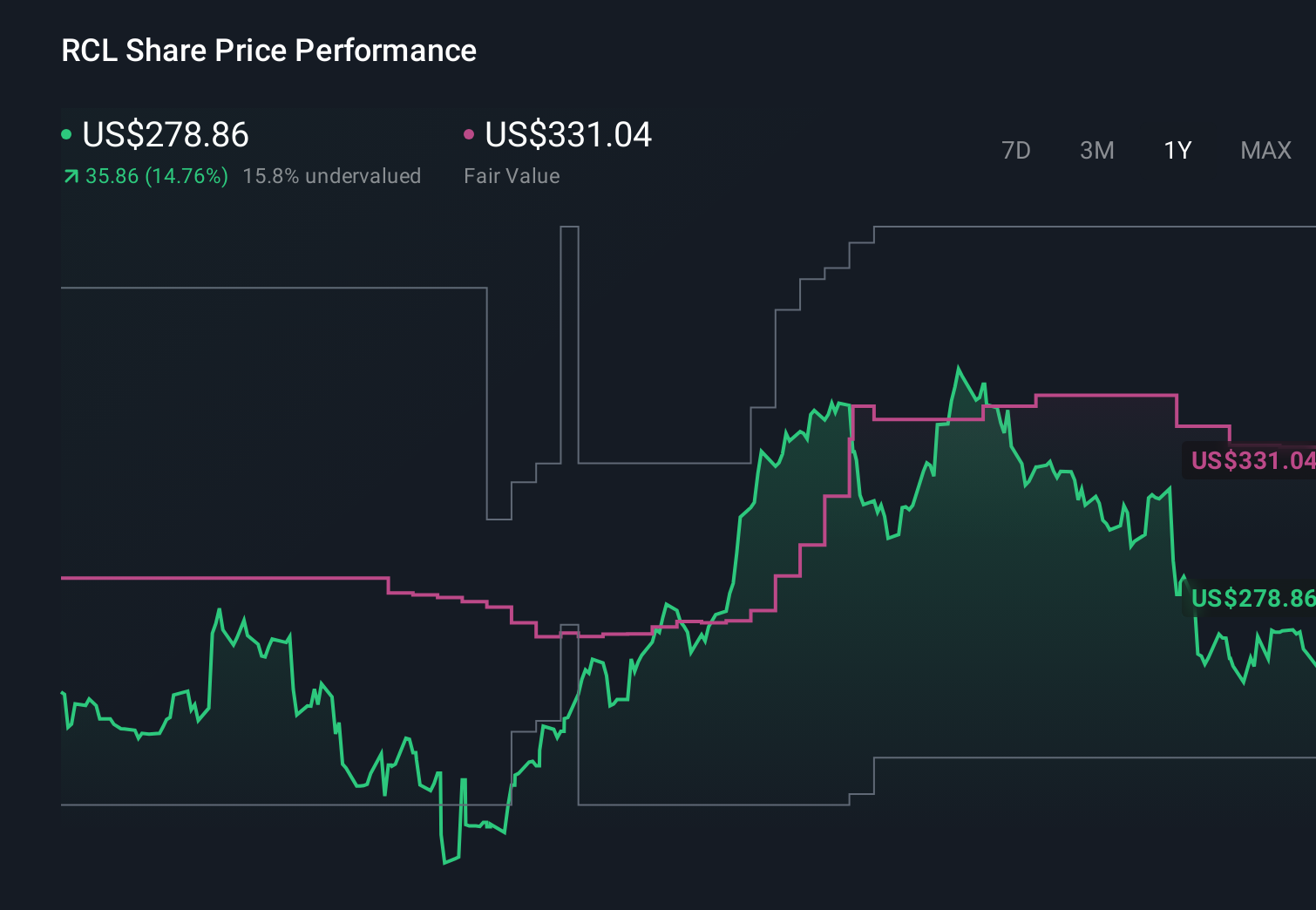

Royal Caribbean Cruises' narrative projects $23.5 billion revenue and $6.1 billion earnings by 2029. This requires 8.6% yearly revenue growth and an earnings increase of about $1.6 billion from $4.5 billion today.

Uncover how Royal Caribbean Cruises' forecasts yield a $338.33 fair value, a 15% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady yield gains, the most optimistic analysts see revenue reaching about US$24.2 billion and earnings near US$6.9 billion, a far more bullish view that could be challenged if rising regulatory and fuel cost pressures start to bite, so it is worth comparing these contrasting narratives before deciding where you stand.

Explore 6 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth 9% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.