Is Semtech (SMTC) A Bargain On Its New Credit Agreement?

Semtech Corporation SMTC | 0.00 |

Semtech (SMTC) recently entered a new Credit Agreement that includes a $360 million undrawn revolving credit facility and an uncommitted incremental term loan option, replacing its prior bank arrangement with extended maturities.

Despite the new Credit Agreement and recent index changes that saw Semtech move into several Russell large and midcap indices, short term momentum has cooled, with the 7 day share price return down 21.90% and the 1 month share price return down 16.30%. However, the 1 year total shareholder return of 180.27% and 3 year total shareholder return of 362.66% point to strong longer term performance.

If you are weighing Semtech against other semiconductor related opportunities, this could be a good moment to see what else is moving via the 52 AI infrastructure stocks

Semtech’s share price has retreated sharply even as analyst targets sit far higher, with the stock trading around $126.40 against a consensus of $205.25. The key question is where a reasonable view of fair value actually falls within that gap.

Most Popular Narrative: 38.3% Undervalued

On the most widely followed narrative, Semtech’s fair value of $204.83 sits well above the recent $126.40 share price, setting up a wide valuation gap that turns on aggressive growth expectations and profitability improvements.

Accelerating demand from hyperscale data centers and AI infrastructure is driving robust, multi-year growth across Semtech's high-margin data center business, supported by design wins in advanced optical (FiberEdge), low-power (LPO), and active copper interconnects (CopperEdge/ACC); as data rates move from 400G to 800G and 1.6T, Semtech stands to capture significant revenue and margin expansion from new content per deployment.

Curious what growth runway and margin profile are baked into that fair value, and how far earnings would need to scale to support it? The narrative leans on steep revenue compounding, a sharp swing into profitability and a rich future earnings multiple usually reserved for sector leaders, all tied to Semtech’s data center and IoT ambitions.

Result: Fair Value of $204.83 (UNDERVALUED)

However, Semtech’s story could change quickly if data center and AI spending slows, or if lower margin IoT and consumer products have a greater impact on profitability.

Another View on Semtech’s Valuation

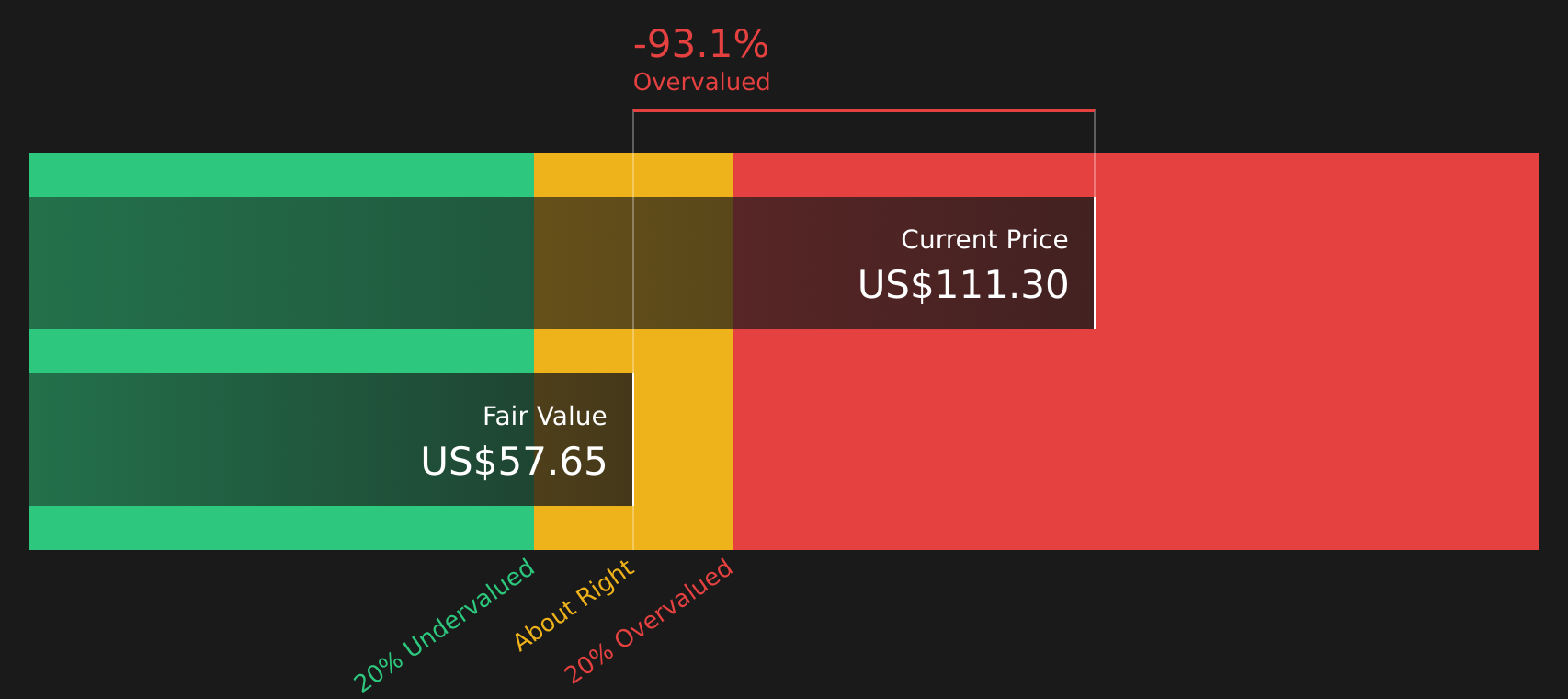

The popular Semtech narrative leans on a fair value of $204.83, but the SWS DCF model tells a very different story, with an estimated future cash flow value of $57.50 against a $126.40 share price, pointing to an overvalued stock instead of a 38.3% undervaluation. Which story feels closer to your own assumptions?

Before leaning on any single framework, it can help to see how that cash flow driven view is built up over time, what discount rate is used, and how sensitive the result is to the growth and margin paths you find realistic for Semtech. Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment on Semtech clearly split between upside potential and downside risk, consider reviewing the underlying data yourself and start with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Semtech?

If Semtech has you thinking about what else could fit your portfolio, this is a smart moment to line up a few fresh ideas using the Simply Wall Street screener.

- Target stronger upside potential by filtering for companies trading below estimated value with the 45 high quality undervalued stocks.

- Prioritize resilience and support more stable returns by focusing on businesses flagged in the 74 resilient stocks with low risk scores.

- Hunt for overlooked opportunities by scanning the screener containing 18 high quality undiscovered gems before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.