Is SentinelOne (S) Undervalued? A Fresh Look at Current Valuation and Growth Prospects

SentinelOne, Inc. Class A S | 13.31 13.09 | +3.34% -1.65% Pre |

Zooming out, SentinelOne’s share price return is down more than 23% year-to-date and it has fallen roughly 10% over the past month, highlighting persistent investor caution despite strong revenue growth. The one-year total shareholder return of -32% underscores that momentum has faded rather than built up as the cyber sector faces new challenges.

If you’re following shifts in tech and cybersecurity, this could be the perfect moment to discover other innovators in the space. See the full list with our See the full list for free..

With shares well below recent highs but revenue growth still in double digits, the central question emerges: is SentinelOne undervalued considering its fundamentals, or is the market accurately pricing in its future growth prospects?

Most Popular Narrative: 26% Undervalued

SentinelOne's fair value, according to the most popular narrative, stands well above its recent close, suggesting the market may be overlooking upcoming growth drivers. This sets the stage for a deeper look at the factors propelling such a valuation.

SentinelOne's robust innovation in AI-driven, autonomous security, highlighted by substantial enterprise adoption of Purple AI and the AI-native SIEM platform, strongly positions the company to capture growing budgets as cyber threats become more sophisticated. This environment could drive sustained revenue growth and improve gross margins as their differentiated offerings enable premium pricing.

Curious about what powers this lofty valuation? What if the secret is a set of rapid growth projections that could reshape the company’s future, along with a profit profile that isn’t what you’d expect from today’s numbers? Don’t miss the full breakdown of the bold financial forecasts and the rationale that underpins this price target.

Result: Fair Value of $23.5 (UNDERVALUED)

However, SentinelOne’s growth story faces potential hiccups if key partnerships weaken or if regulatory shifts add unexpected complexity to international expansion.

Another View: Multiples Tell a Different Story

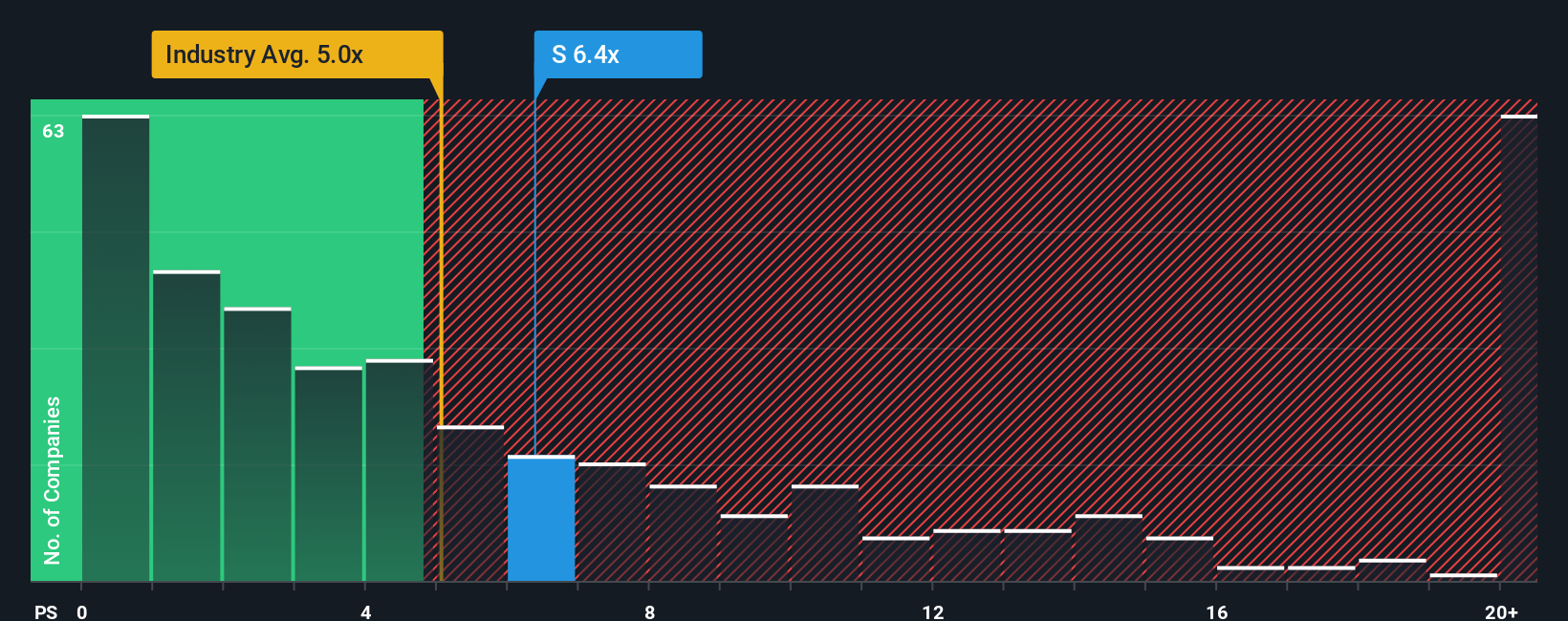

Looking at how SentinelOne is valued based on its price-to-sales ratio, the stock appears expensive, trading at 6.4 times revenue. This is higher than the US Software industry average of 5.2 times but lower than the peer average of 9.3 times. Notably, the current multiple sits below the estimated fair ratio of 7.3. This suggests some relative value, but also hints that investors might be factoring in risk or uncertainty about the company’s path forward.

Build Your Own SentinelOne Narrative

If you’re not fully convinced by this perspective or want to dig deeper into the numbers yourself, building your own narrative takes just a few minutes. Do it your way.

A great starting point for your SentinelOne research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors constantly expand their horizons. Use the Simply Wall Street Screener to find unique stocks and fresh opportunities before they hit everyone’s radar.

- Uncover overlooked growth potential by targeting these 874 undervalued stocks based on cash flows, where robust fundamentals meet attractive valuations you might not see elsewhere.

- Maximize income opportunities by acting now with these 17 dividend stocks with yields > 3% featuring high yields that can strengthen your portfolio returns in any market climate.

- Get ahead of market disruptions as these 26 AI penny stocks push the boundaries of artificial intelligence and set the pace for tomorrow’s leading businesses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.