Is Shopify (SHOP) Pricing In Too Much Future Growth After Its Recent 20% Surge?

Shopify, Inc. Class A SHOP | 0.00 |

- Wondering if Shopify at around US$124 per share is priced for its future or already fully valued? This article breaks down what the current market is implying.

- The stock has moved sharply, up 20.5% over the past week. However, it is down 2.8% over the last 30 days and down 21.0% year to date, while still showing a 16.5% gain over the past year and a 107.1% return over three years.

- Recent headlines have focused on Shopify's role as a core e commerce platform partner for merchants and how investors are interpreting that role in a changing online retail environment. This context helps explain why the stock can swing between enthusiasm and caution as sentiment shifts.

- Despite this mix of returns, Shopify currently scores 0 out of 6 on Simply Wall St's valuation checks. The next sections will break down what different valuation methods say about the stock and then finish with a more complete way to think about valuation overall.

Shopify scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

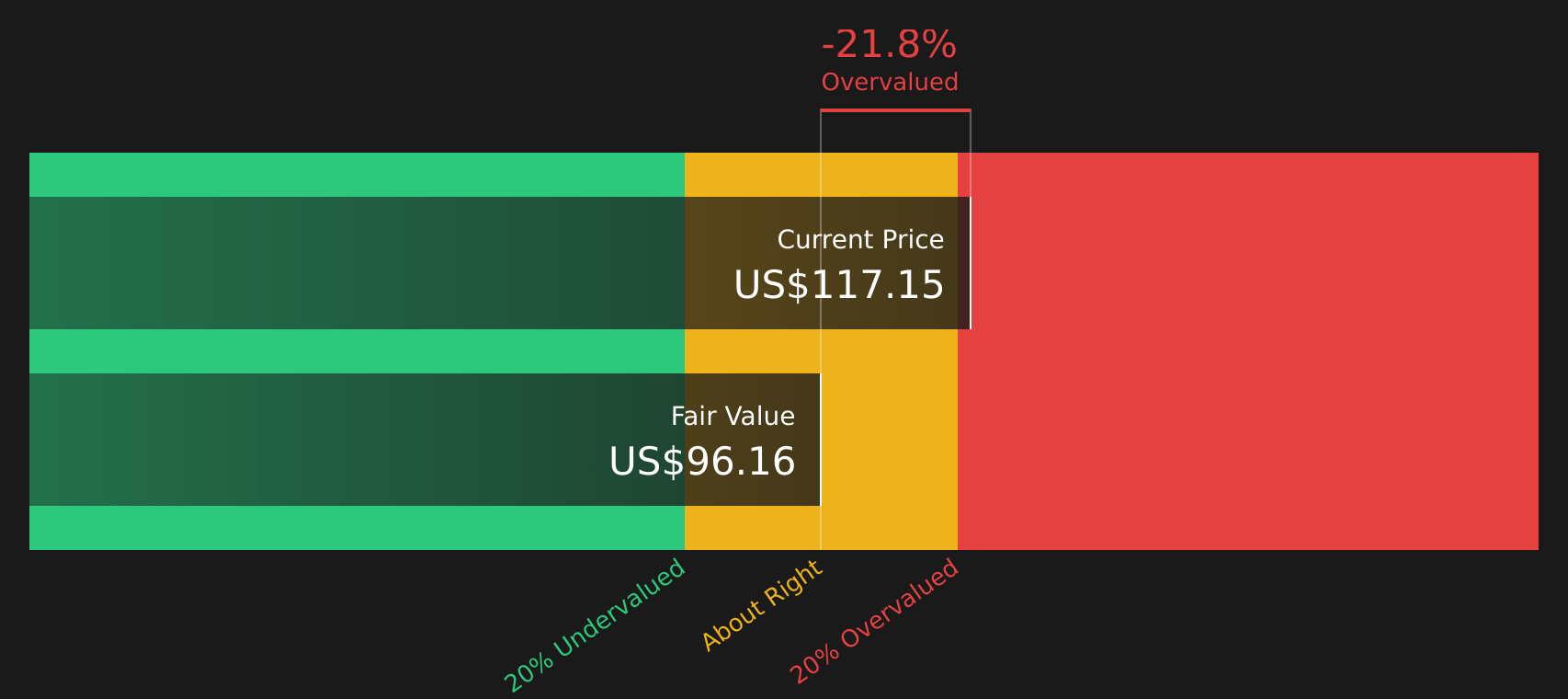

Approach 1: Shopify Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash Shopify is expected to generate in the future and discounts those amounts back to today, using a required rate of return, to estimate what the business might be worth right now.

Shopify’s latest twelve month free cash flow sits at about US$2.1b. Using a 2 Stage Free Cash Flow to Equity model, analysts and extrapolated estimates project free cash flow rising to about US$6.4b in 2030, with a series of annual projections in between. Simply Wall St provides analyst inputs for the first five years, then extends the trend out to year ten using its own growth assumptions.

When those projected cash flows, including the US$6.4b estimate for 2030, are discounted back, the model arrives at an intrinsic value of roughly US$106.72 per share. Versus a current share price around US$124, this implies Shopify is about 16.3% more expensive than the DCF estimate, so the stock screens as overvalued on this model alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Shopify may be overvalued by 16.3%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Shopify Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings, which is often how many investors quickly compare stocks in the same sector.

What counts as a “normal” P/E ratio depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth and perceived stability can justify a higher P/E, while slower growth or higher risk usually points to a lower, more conservative multiple.

Shopify currently trades on a P/E of about 121.2x. That is well above the IT industry average of 20.6x and also above the peer group average of 64.6x. Simply Wall St’s Fair Ratio for Shopify is 53.3x, which represents the P/E level suggested after weighing factors such as earnings growth, profit margins, industry, market cap and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or the broader industry, because it adjusts for Shopify’s own characteristics instead of assuming that all IT stocks deserve similar multiples. With the actual P/E sitting far above the 53.3x Fair Ratio, the stock screens as expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Shopify Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in as your way to connect Shopify’s story with the numbers you care about.

A Narrative is simply your description of what you think is happening at a company, paired with your own assumptions for future revenue, earnings and margins, which then flows through to a Fair Value estimate.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors to do exactly this. You can see how different views on Shopify’s future translate into different forecasts and fair values.

For example, one Shopify Narrative currently assumes a fair value of about US$105 per share while another sits closer to US$252. That wide range clearly shows how different expectations around revenue growth, profit margins and future P/E multiples can support very different views on what the stock is worth.

Once you have a Narrative, comparing its Fair Value to the current share price helps you decide whether Shopify looks attractive or stretched on your assumptions. Because Narratives on Simply Wall St update as new earnings, news and forecasts arrive, your view can stay aligned with the latest information instead of being locked into a static model.

For Shopify however we will make it really easy for you with previews of two leading Shopify Narratives:

Together they frame the current debate around whether today’s share price looks stretched or still reasonable once different assumptions are plugged into the model.

Use them as starting points, then decide which set of expectations feels closer to how you see the business.

Fair value: US$186.64 per share

Implied discount to fair value versus the recent US$124.12 share price: about 33.5% undervalued

Revenue growth used in this Narrative: 12%

- Focuses on social commerce as a large addressable market, with mobile traffic and embedded shopping expected to support Shopify’s role as an e commerce enabler.

- Assumes AI tools like Store Builder and Sidekick, plus integrations with partners such as DHL and Amazon fulfillment, keep lowering friction for merchants.

- Flags tariffs, consumer confidence and competition from large platforms as key risks that could weigh on smaller merchants and on Shopify’s US exposure.

Fair value: US$105.00 per share

Implied premium to fair value versus the recent US$124.12 share price: about 18.2% overvalued

Revenue growth used in this Narrative: 20.98%

- Emphasises saturation signs in global e commerce, regulatory requirements and higher operating costs as potential drags on future growth and margins.

- Points to competition, feature convergence and the cost of supporting a broad ecosystem as possible drivers of pricing pressure and churn risk.

- Assumes a future P/E of about 60x on earnings by 2029, framing the stock as sensitive to any disappointment in revenue, margin or execution against these expectations.

Seen together, these Narratives show how the same company can look either cheap or expensive once you lock in different fair values, revenue paths and margin profiles. The key step is deciding which assumptions you find more reasonable, then checking whether the current US$124.12 share price still fits your own thesis or calls for a rethink.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Shopify on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Shopify? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.