Is Southwest (LUV) Turning Domestic Scale Into Global Pricing Power With Its Singapore Airlines Tie-Up?

Southwest Airlines Co. LUV | 0.00 |

- In June 2026, Singapore Airlines announced a partnership with Southwest Airlines to offer single-ticket journeys linking Singapore’s global network with Southwest’s nearly 120 U.S. destinations via Los Angeles, Seattle/Tacoma, and San Francisco, alongside Southwest’s new 2026 services to St. Thomas, Sint Maarten, Santa Rosa/Sonoma County, Knoxville, and Anchorage.

- This agreement expands Southwest’s international connectivity through eight overseas carrier partnerships across Asia, Europe, the Middle East, and Africa, potentially increasing the appeal of its largely domestic network to long-haul travelers.

- We’ll now examine how this expanded international connectivity through Singapore Airlines could reshape Southwest’s existing investment narrative around distribution, pricing, and partnerships.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Southwest Airlines Investment Narrative Recap

To own Southwest, you need to believe its low cost model, product changes, and expanding partnerships can translate into durable earnings, despite demand and cost uncertainty. The Singapore Airlines deal reinforces the near term catalyst around distribution and partnerships by feeding more long haul travelers into Southwest’s domestic network, but it does not remove key risks tied to macro softness, fuel costs, and potential disruption from aircraft delivery issues or new fee structures.

The Singapore Airlines tie up fits neatly with Southwest’s recent push into new channels, especially the Expedia distribution launch, which targets customers who previously did not book directly with the airline. Both moves expand the potential pool of travelers exposed to Southwest’s new fare types and loyalty ecosystem, supporting the catalyst around higher yields and better aircraft utilization, while the company continues working on cost control and operational efficiency to sustain margin improvement.

Yet, against these positives, investors should be aware that heavy reliance on the U.S. domestic market still leaves Southwest exposed if...

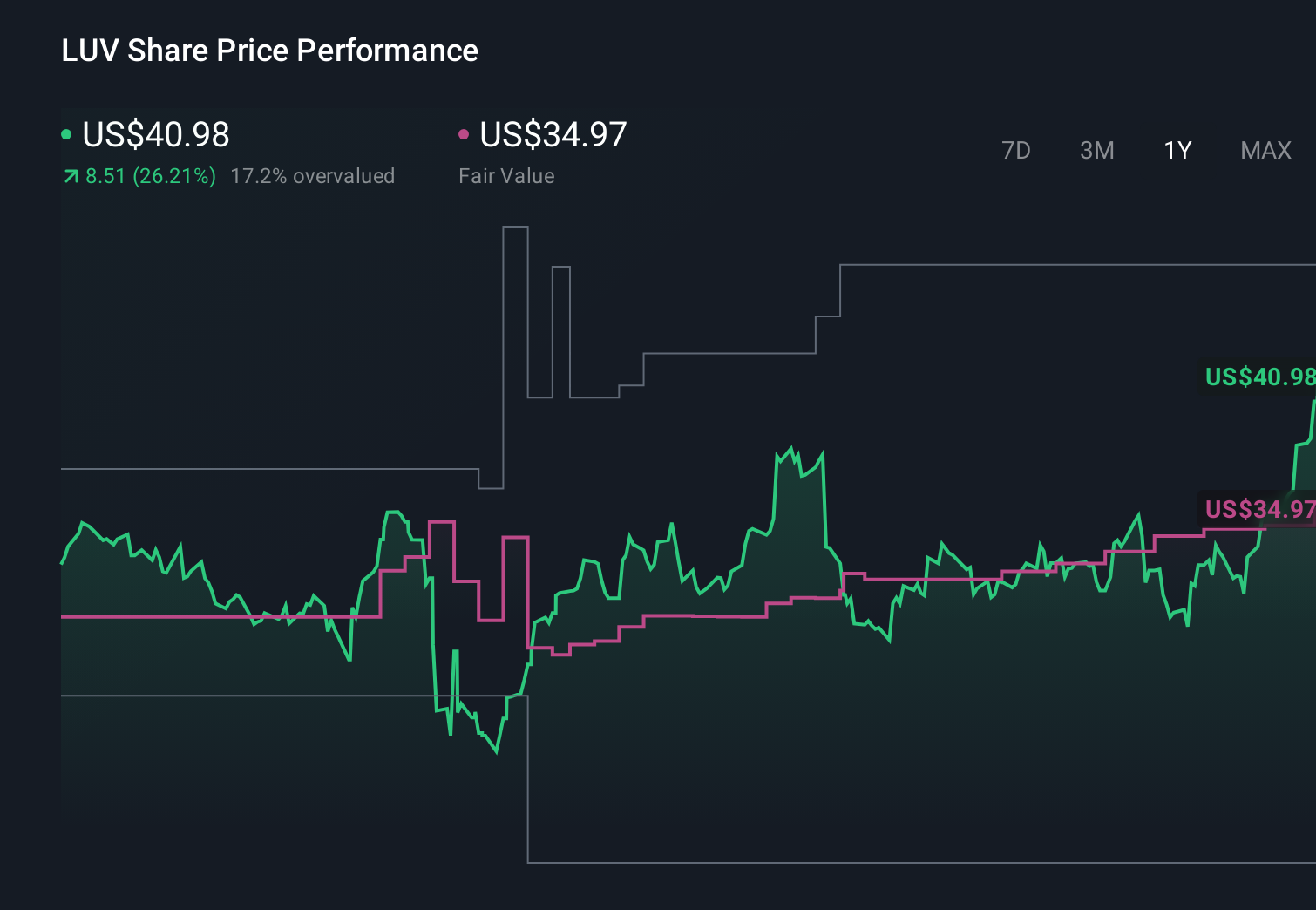

Southwest Airlines’ narrative projects $34.6 billion revenue and $2.2 billion earnings by 2029.

Uncover how Southwest Airlines' forecasts yield a $45.64 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue reaching about US$36.6 billion and earnings of roughly US$2.7 billion by 2029, and now this Singapore Airlines partnership could further test whether their bullish view on Southwest’s international connectivity and domestic concentration risk really holds up or needs rethinking.

Explore 4 other fair value estimates on Southwest Airlines - why the stock might be worth just $45.64!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.