Is Starbucks (SBUX) Share Price Justified After Recent Turnaround Focus?

Starbucks Corporation SBUX | 90.37 | -0.07% |

- If you are wondering whether Starbucks at around US$93.79 is priced for a comeback or still has work to do, you are not alone. This article will help you frame that question around value.

- The stock is up 0.9% over the last 30 days and 11.7% year to date, but over 1 year it has returned 14.4% and over 5 years 1.8%. This leaves many investors asking how today’s price stacks up against the company’s fundamentals.

- Recent attention on Starbucks has focused on how the brand is executing on its long term store growth plans and managing consumer demand in key markets. At the same time it is dealing with cost pressures and competitive pressures in premium coffee. These themes are often front of mind for investors trying to connect the share price moves over the past week, including the 5.7% return over 7 days and 5.7% return over 3 years, with the underlying business story.

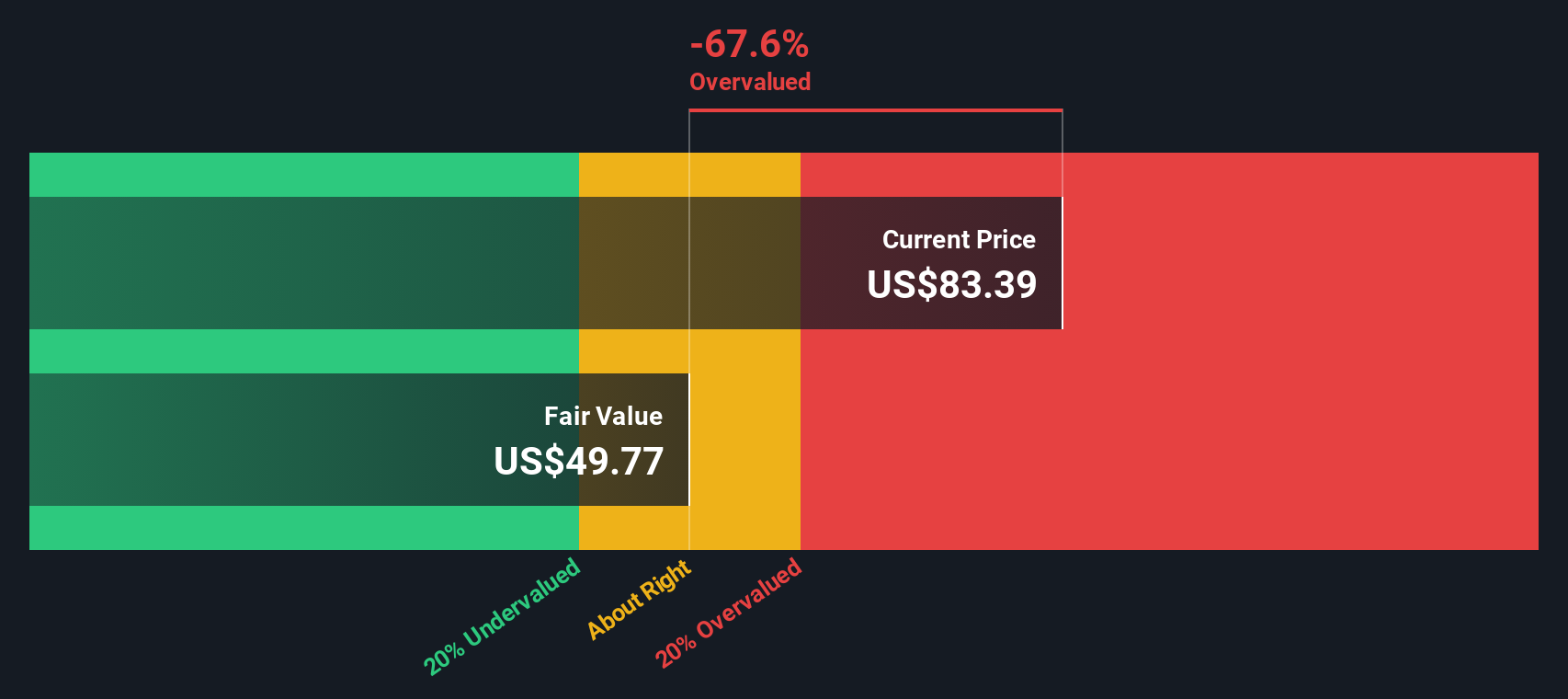

- Right now, our valuation model gives Starbucks a value score of 0 out of 6, which suggests it does not screen as undervalued on any of our standard checks. The key question is how different methods like DCF, multiples and comparables line up and whether there is an even better way to think about value that we will come back to at the end of this article.

Starbucks scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Starbucks Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model takes Starbucks projected future cash flows and discounts them back to today, aiming to estimate what the entire stream of cash is worth in present terms.

Starbucks last twelve month free cash flow is about US$1.8b. Using a 2 Stage Free Cash Flow to Equity model, analysts provide explicit forecasts for several years, then Simply Wall St extrapolates further out. For example, projected free cash flow for 2029 is US$4.5b, with intermediate years such as 2026 to 2035 ranging from roughly US$2.8b to US$6.5b before discounting.

Bringing all those projected cash flows back to today results in an estimated intrinsic value of US$73.67 per share. Compared with the current share price of about US$93.79, the DCF output suggests Starbucks trades at a 27.3% premium to this cash flow based estimate, so on this model it screens as overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Starbucks may be overvalued by 27.3%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

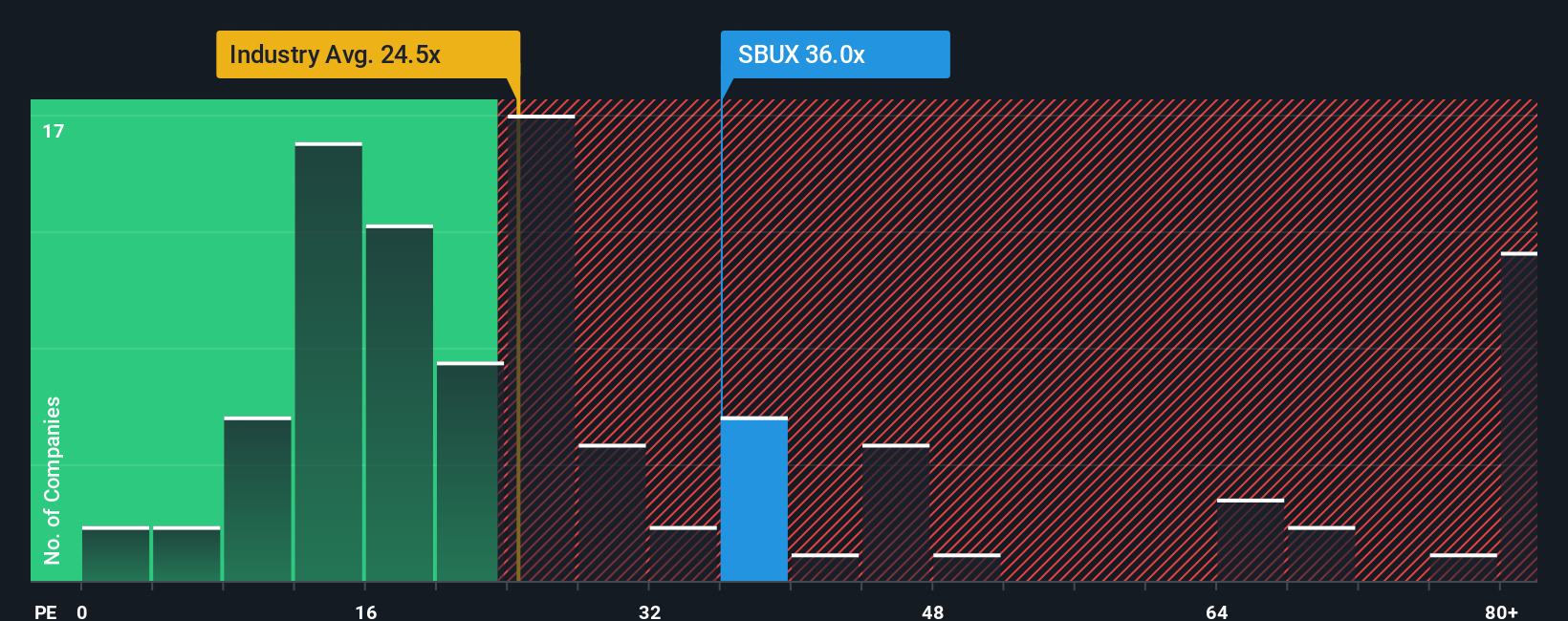

Approach 2: Starbucks Price vs Earnings

For a profitable company like Starbucks, the P/E ratio is a common way investors look at value because it links what you pay for each share to the earnings that share is currently generating.

What counts as a normal or fair P/E typically reflects how the market sees a company’s growth prospects and risk profile. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth expectations or higher risk usually point to a lower P/E.

Starbucks currently trades on a P/E of 78.06x. That is well above the Hospitality industry average of 21.36x and also higher than the peer group average of 41.66x. Simply Wall St’s Fair Ratio framework estimates a P/E of 48.90x for Starbucks, based on factors like its earnings growth profile, profit margins, industry, market cap and risk characteristics.

This Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it adjusts for Starbucks specific qualities, rather than assuming it should trade in line with an average. Comparing the Fair Ratio of 48.90x with the current P/E of 78.06x suggests the shares are pricing in more than this framework implies.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Starbucks Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way for you to spell out your story about Starbucks, connect it to specific forecasts for revenue, earnings and margins, and arrive at your own fair value that you can compare with the current price.

On Simply Wall St’s Community page, Narratives let you link a clear thesis to numbers. The platform then keeps that fair value updated when new data such as earnings or news is added, so you can quickly see whether your view still makes sense or if the gap between fair value and market price is closing or widening.

For Starbucks, one investor might lean toward the higher fair value case at about US$120 per share, with assumptions such as stronger margins and a future P/E above 36x. Another investor might align with the low end, around US$67 to US$72 per share, with slower revenue growth and profit margins closer to 8% to 10%. Narratives let you see exactly which story you agree with and how your assumptions compare.

For Starbucks however we will make it really easy for you with previews of two leading Starbucks Narratives:

Here is what the current bull and bear cases look like side by side, using concrete assumptions rather than vague labels.

Fair value in this bull narrative: US$97.59 per share

Current price vs this fair value: about 3.9% below the narrative fair value

Revenue growth used in the narrative: 8.3%

- Assumes the new CEO’s turnaround plan simplifies stores and menus, improves efficiency and lifts margins despite higher coffee and labor costs.

- Sees global expansion continuing, while also flagging that China and other overseas markets bring competition and execution risk.

- Builds to an equity value of about US$110.3b, or US$97.59 per share, using mid single digit revenue growth, margins around 10.5% and a P/E closer to long term averages.

Fair value in this bear narrative: US$86.27 per share

Current price vs this fair value: about 8.7% above the narrative fair value

Revenue growth used in the narrative: 5.0%

- Assumes Starbucks grows stores to 56,000 by 2030, but that international stores earn much less per location so returns on capital trend lower.

- Expects profit margins to sit around 13% while wage pressure, union activity and new competitors in premium coffee and alternative caffeine keep growth in check.

- Uses a lower future P/E of 22x and around 5% annual revenue growth, which leads to a fair value estimate of US$86.27 per share, below today’s price.

Taken together, these two Narratives frame a reasonable range of views for Starbucks, with one arguing that the current price sits a little below its long term potential and the other suggesting it is ahead of what more cautious assumptions support.

If you want to see how other investors are joining the dots between Starbucks fundamentals, risks and valuation, Curious how numbers become stories that shape markets? Explore Community Narratives is a useful next step.

Do you think there's more to the story for Starbucks? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.