Is Strong Q2 Results And Portfolio Shift Altering The Investment Case For Phibro Animal Health (PAHC)?

Phibro Animal Health Corporation Class A PAHC | 0.00 |

- Phibro Animal Health recently reported strong fiscal Q2 2026 results, with earnings per share and revenue topping expectations and highlighting improved profitability and operational progress across its animal health portfolio.

- At the same time, the company’s integration of Zoetis’ medicated feed additive business and expanding vaccines franchise point to a business mix that is shifting toward higher-value products and broader international reach.

- With this backdrop of better-than-expected quarterly performance, we’ll explore how Phibro’s accelerating earnings and margin trends may reshape its investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Phibro Animal Health Investment Narrative Recap

To own Phibro Animal Health, you have to believe its shift toward vaccines, nutritional specialties, and the Zoetis medicated feed additives can support healthier margins while managing regulatory and geopolitical risks. The latest earnings beat reinforces that earnings momentum is a key short term catalyst, while the biggest near term risk remains execution on integrating higher value products without overreliance on medicated feed additives. The recent news supports this narrative rather than materially changing it.

The most relevant development here is Phibro’s strong fiscal Q2 2026 results, with earnings and revenue ahead of expectations and better profitability across its animal health portfolio. That print, combined with positive guidance for fiscal 2026, underpins the view that Phibro Forward and the Zoetis MFA integration are gaining traction, which matters directly for the margin and earnings assumptions behind both the consensus outlook and the more optimistic scenarios.

Yet while the story looks attractive on the surface, investors should also be aware that...

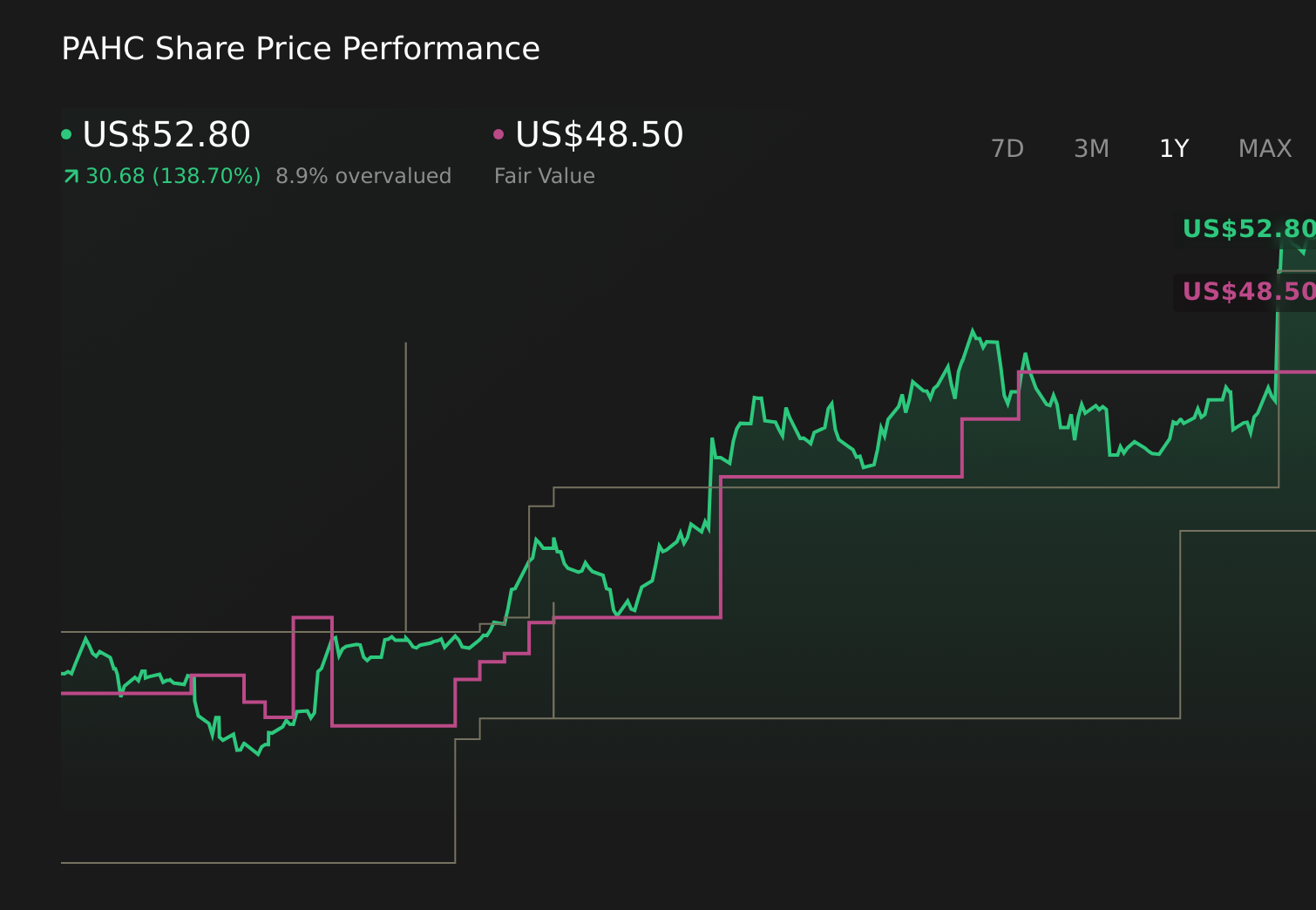

Phibro Animal Health's narrative projects $1.5 billion revenue and $119.1 million earnings by 2028. This requires 6.1% yearly revenue growth and a $70.8 million earnings increase from $48.3 million today.

Uncover how Phibro Animal Health's forecasts yield a $48.50 fair value, a 13% downside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already assuming revenues near US$1.6 billion and earnings of about US$154.7 million by 2029, so this upside surprise could either reinforce those expectations or prompt a rethink, especially if reliance on medicated feed additives remains a concern.

Explore 2 other fair value estimates on Phibro Animal Health - why the stock might be worth 13% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Phibro Animal Health research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Phibro Animal Health research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Phibro Animal Health's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.