Is Stronger AI Demand Reshaping Arteris (AIP) From Niche IP Vendor Into Core Chip Architect?

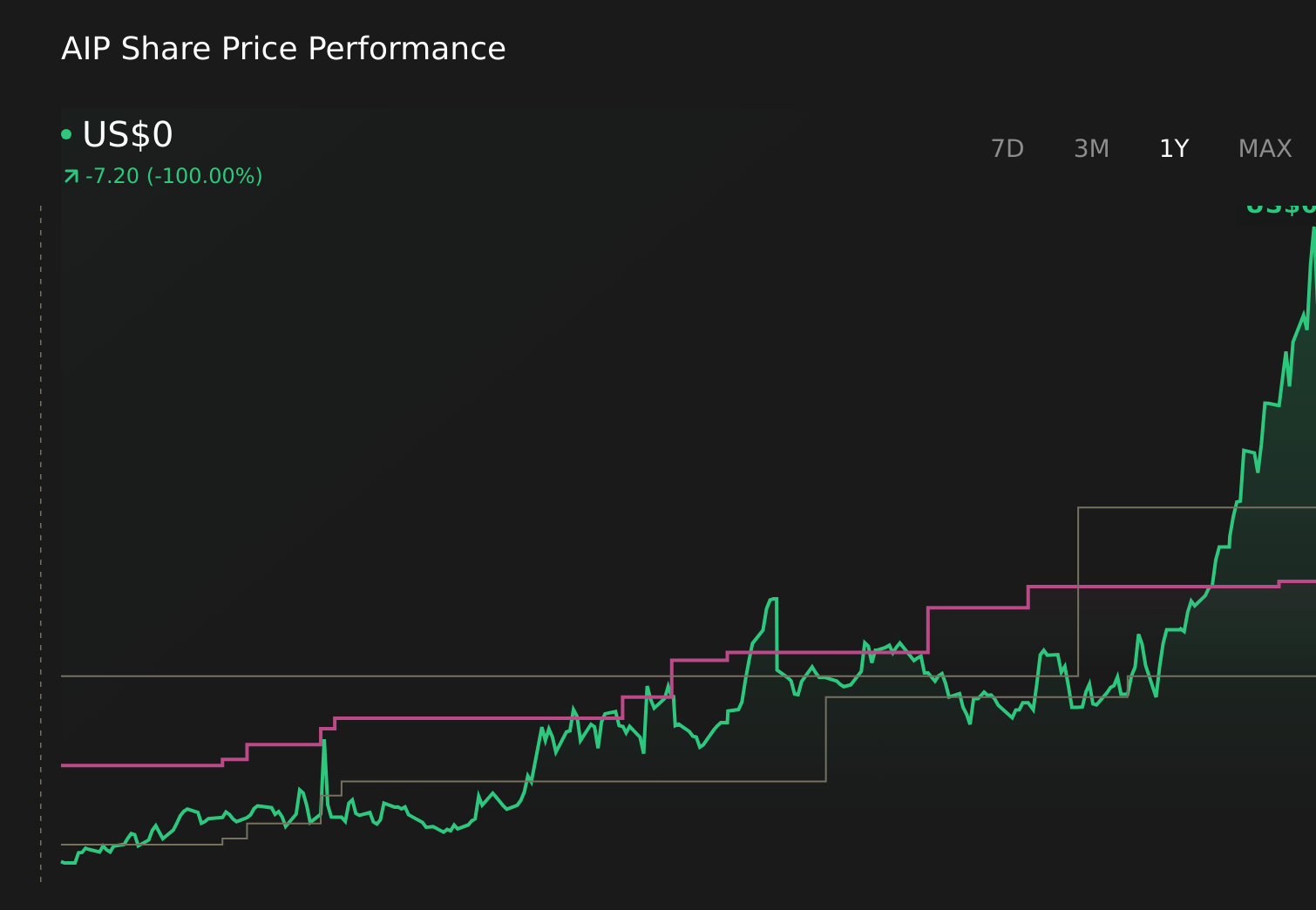

Arteris AIP | 0.00 |

- In early June 2026, Arteris reported increasing demand for its advanced Network-on-Chip IP as artificial intelligence and machine learning adoption gained pace across enterprise computing, automotive, and other complex-chip markets.

- This surge in interest highlights how Arteris’ position in AI-centric chip design is becoming more central to customers seeking to manage rapidly rising system complexity.

- Next, we’ll explore how this stronger AI-driven demand for Arteris’ Network-on-Chip IP affects the company’s existing investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Arteris Investment Narrative Recap

To own Arteris, you need to believe that its Network on Chip IP can remain central to managing rising chip complexity as AI spreads across sectors. The latest news of stronger AI driven demand reinforces that core thesis but does not materially change the near term tension between rapid top line growth and ongoing net losses, or the key risk that a handful of large customers could still drive meaningful revenue volatility if their plans shift.

Among recent announcements, the expanded NXP engagement in February 2026 looks especially relevant. It ties Arteris’ NoC, Ncore and Magillem tools directly to AI enabled MCUs and NPUs, echoing the same AI centric demand visible in the June update. Together, these wins underline the main catalyst investors are watching: broader adoption of Arteris IP across multiple large chipmakers, which could help support operating leverage if revenue continues to scale faster than costs.

Yet beneath this strong AI story, investors should also be aware that customer concentration risk remains a critical issue if any major partner decides to internalize key IP...

Arteris' narrative projects $130.9 million revenue and $15.0 million earnings by 2029.

Uncover how Arteris' forecasts yield a $20.50 fair value, a 39% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected about 24.5 percent annual revenue growth and US$15.5 million in earnings by 2029, so this fresh AI driven momentum could either reinforce those bullish views or force a rethink of how customer concentration risk might cap the upside, reminding you that reasonable people can look at the same stock and reach very different conclusions.

Explore 5 other fair value estimates on Arteris - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Arteris research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Arteris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arteris' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.