Is Stronger Earnings and CFO Transition Altering The Investment Case For Plexus (PLXS)?

Plexus Corp. PLXS | 0.00 |

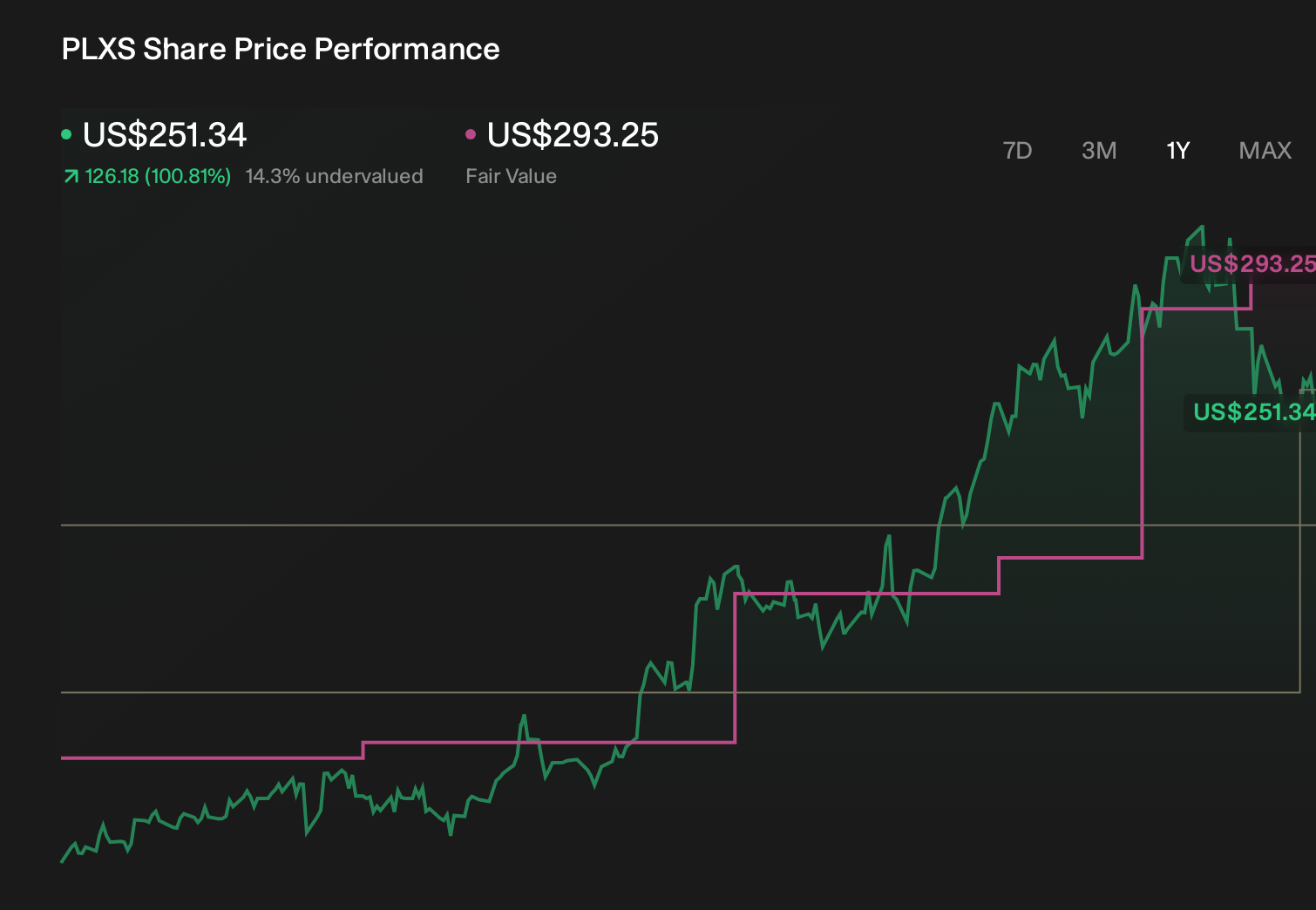

- Plexus Corp. recently reported past second-quarter and six-month results to April 4, 2026, with higher sales, net income and earnings per share versus a year earlier, and issued new third-quarter revenue and GAAP diluted EPS guidance.

- The company also confirmed the upcoming retirement of long-serving CFO Patrick Jermain, outlined a planned handover to incoming CFO David Abuhl, and disclosed continued share repurchases and insider stock sales by the CEO.

- Next, we’ll examine how Plexus’ stronger quarterly earnings and raised outlook could influence its existing investment narrative and risk-reward profile.

Rare earth metals are the new gold rush. Find out which 34 stocks are leading the charge.

Plexus Investment Narrative Recap

To own Plexus, you need to believe its focus on complex, higher value electronics manufacturing can keep attracting long term programs across healthcare, aerospace and industrial markets. The latest quarter’s stronger earnings and raised Q3 outlook support that thesis, but the key near term catalyst and risk both remain demand stability in core end markets, where order pushouts or program delays could still introduce meaningful revenue and margin volatility despite recent momentum.

Among the recent announcements, Plexus’s new third quarter guidance for revenue of US$1.20 billion to US$1.25 billion and GAAP diluted EPS of US$1.25 to US$1.41 is most relevant. It sits directly against concerns about cyclicality and customer concentration, because it gives investors a near term benchmark for how well current program ramps are converting into sales and profits, and whether the company can offset any softness in semicap, aerospace or other key verticals.

Yet against this stronger quarter, investors should still be aware that a sharp slowdown in semicap or aerospace and defense program ramps could...

Plexus' narrative projects $5.4 billion revenue and $223.8 million earnings by 2029. This requires 9.4% yearly revenue growth and a $47.0 million earnings increase from $176.8 million today.

Uncover how Plexus' forecasts yield a $210.80 fair value, a 21% downside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming only about 9.9% annual revenue growth and US$281.3 million of earnings by 2029, so if you worry about slower program conversion and margin pressure, this more cautious view might feel closer to home than the consensus.

Explore 2 other fair value estimates on Plexus - why the stock might be worth as much as $210.80!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Plexus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Plexus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Plexus' overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.