Is Talos Energy a Bargain After Gulf Coast Expansion and Recent Share Price Drop?

Talos Energy, Inc. TALO | 15.65 | +4.82% |

- Wondering if Talos Energy is undervalued, overhyped, or sitting at the perfect entry point? You’re not alone, and there’s plenty to dig into.

- The stock has seen minor ups and downs lately, gaining 0.6% over the last week but still down 2.8% across the past month and a steeper 12.4% over the year.

- Recent headlines have focused on Talos Energy’s strategic offshore acquisitions and expanding Gulf Coast operations. These moves have fueled discussions around the company’s long-term growth and risk factors and are helping shape investor sentiment, especially as the energy sector sees renewed attention.

- On our 6-point valuation checklist, Talos Energy scores a 5. This is impressive for a stock with this much volatility. Let’s break down how each method stacks up and, more importantly, reveal an even smarter approach to sizing up its fair value at the end.

Approach 1: Talos Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s dollars. The goal is to figure out what those future cash streams are really worth right now, based on time and risk.

For Talos Energy, analysts estimate its Free Cash Flow at $610.8 Million over the last twelve months. Looking ahead, projections show Free Cash Flow rising to $217 Million by 2028. Since analyst estimates only reach out five years, Simply Wall St’s model extends beyond that period by extrapolating a gradual shift in cash flow growth over the next decade.

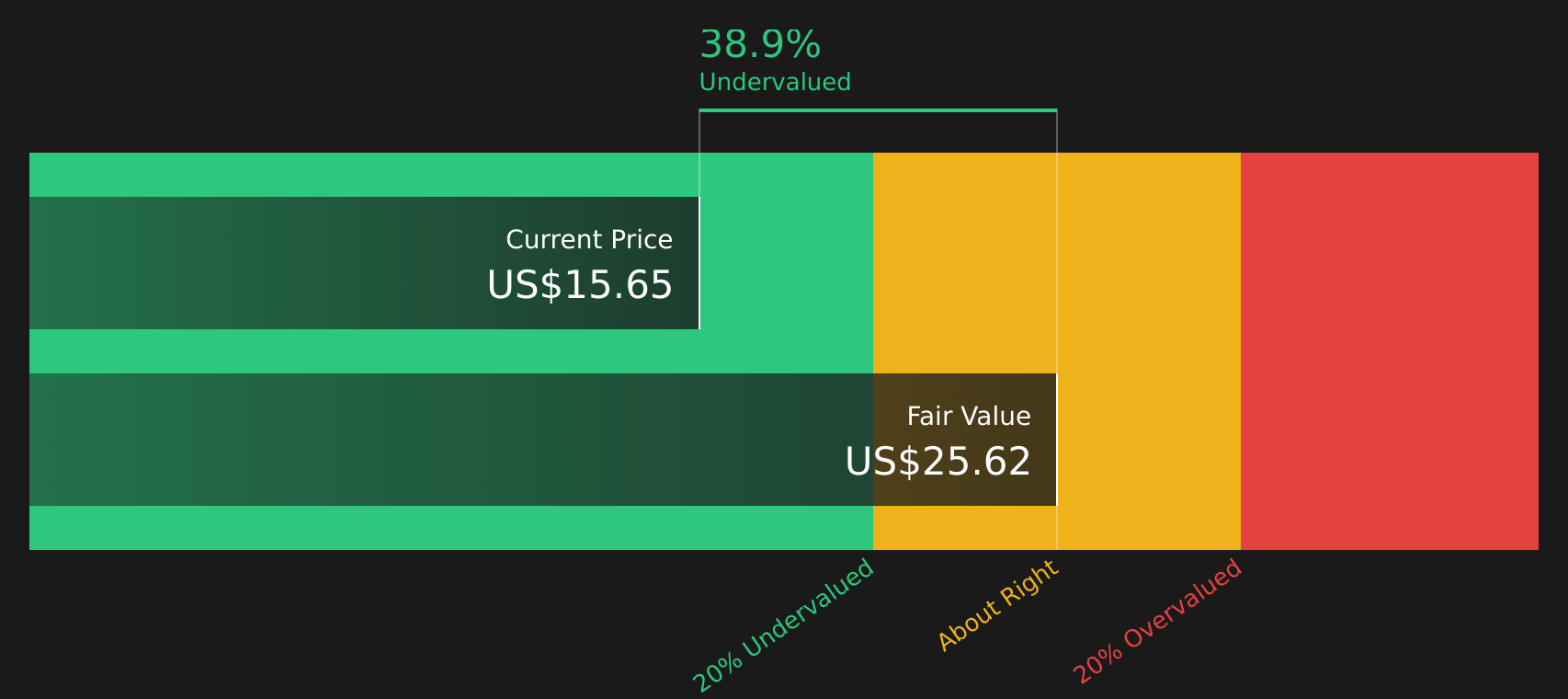

Using these projections, the resulting DCF model calculates an intrinsic value per share of $22.62. With the current market price at a 57.7% discount to this estimate, this suggests that Talos Energy is trading significantly below what its future cash flows imply it is worth.

By this measure, the stock appears to have meaningful upside potential for investors who are willing to look past short-term volatility.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Talos Energy is undervalued by 57.7%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

Approach 2: Talos Energy Price vs Sales

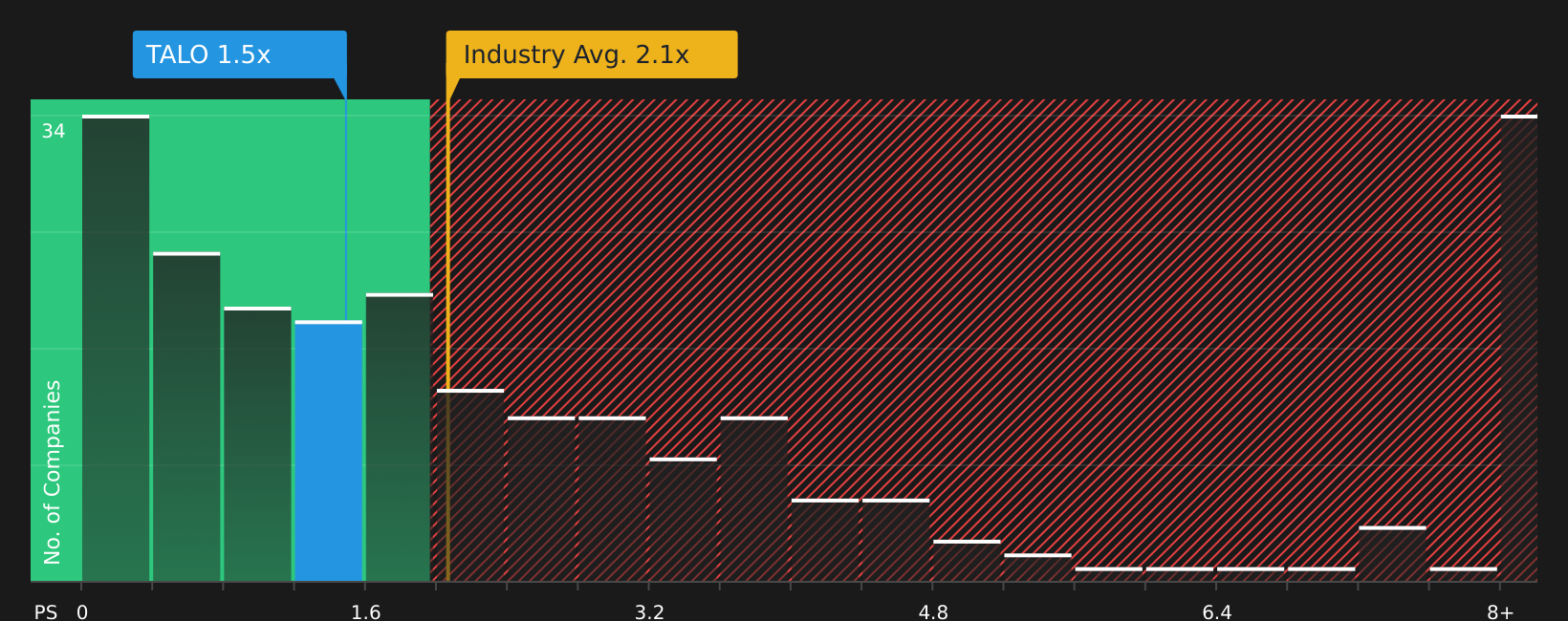

The Price-to-Sales (P/S) ratio is often a preferred valuation metric for companies like Talos Energy, especially when profitability can be lumpy from quarter to quarter. This ratio measures a company’s market value relative to its revenue, making it useful for evaluating firms that may not have consistent earnings due to industry cycles but still generate meaningful sales.

The "right" P/S multiple for any company is shaped by expectations for future growth and perceptions of risk. Higher growth prospects can justify a steeper multiple, while greater risks or shrinking revenues generally demand a discount. Comparing the P/S ratio to industry benchmarks and peers helps give context to whether a stock is pricey or a bargain.

Currently, Talos Energy trades at a P/S ratio of 0.86x. This is notably lower than the peer group average of 1.74x and the Oil and Gas industry average of 1.46x. However, just looking at these figures does not capture the entire story.

This is where the Simply Wall St "Fair Ratio" comes in. The Fair Ratio takes into account not just industry standards but also Talos Energy’s unique growth outlook, profitability, and risk profile. It aims to reflect what a reasonable investor should pay, using a more holistic approach than simple peer comparisons. For Talos, the Fair Ratio is 1.66x.

Since Talos Energy’s actual P/S is significantly below its Fair Ratio, the stock appears undervalued on this metric.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Talos Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is your personal story about a company, an easy, structured way to express not just what you think Talos Energy is worth, but why you believe it, through your assumptions about future revenue, earnings, and margins.

Narratives help you connect the facts and forecasts to the underlying company story, making your investment thesis both transparent and actionable. On Simply Wall St’s Community page, millions of investors use Narratives to blend financial forecasts with their unique perspectives, building a bridge between raw numbers and real-world events.

These Narratives update automatically as new data arrives, whether that is major news or quarterly earnings, so your investment thinking stays dynamic and relevant. By comparing your Narrative Fair Value to Talos Energy’s current market price, you can easily decide for yourself if now is the right time to buy or sell, based on logic, not just hype or headlines.

For example, some investors believe Talos is worth $20.0, seeing strong growth from disciplined cost controls, while others assign only $9.0, citing industry risks and volatile revenues. Your Narrative helps you cut through the noise and invest with conviction.

Do you think there's more to the story for Talos Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.