Is Tango Therapeutics (TNGX) Fully Valued On Russell Index Rebalancing?

Tango Therapeutics, Inc. TNGX | 0.00 |

Tango Therapeutics (TNGX) is at the center of index rebalancing after being added to several Russell growth benchmarks and removed from various value and microcap indexes, a mix that can reshape short term trading flows.

Tango Therapeutics has seen a sharp shift in momentum, with the share price up 48.07% over the past month and a 235.27% year to date share price return, alongside a very large 1 year total shareholder return of 451.38%. This highlights how strongly expectations have changed around the company, despite a recent 7 day share price pullback of 8.05%.

If index moves around Tango Therapeutics have caught your attention, it could be a good moment to see what else is moving in healthcare AI and precision medicine via 40 healthcare AI stocks.

Tango Therapeutics now sits near the center of growth indices after a very sharp run in the share price. The key question is whether the current valuation still leaves enough potential upside to justify the risks buyers are taking on from here.

Preferred Price-to-Book Multiple of 11.1x: Is It Justified?

Tango Therapeutics is currently being assessed on a rich P/B multiple, with investors clearly paying a premium relative to both peers and the wider US biotech sector.

The preferred multiple here is the price-to-book ratio, which compares the company’s market value to the accounting value of its net assets. For Tango Therapeutics, that figure stands at 11.1x, a level that often reflects strong expectations about future potential rather than current profitability, especially for a precision oncology company that is still reporting losses.

For context, the US Biotechs industry average P/B is 2.8x, while the peer average sits at 4.5x. Tango Therapeutics is therefore trading at a multiple several times higher than both groups. That suggests the market is pricing in significantly stronger prospects than those implied by a more typical sector or peer valuation band, even though the company is currently unprofitable.

Result: Price-to-book of 11.1x (OVERVALUED)

However, Tango Therapeutics still carries meaningful risk if its current drug candidates run into clinical setbacks, or if sentiment cools and the rich P/B multiple compresses.

Another View on Tango Therapeutics: DCF vs Market Multiple

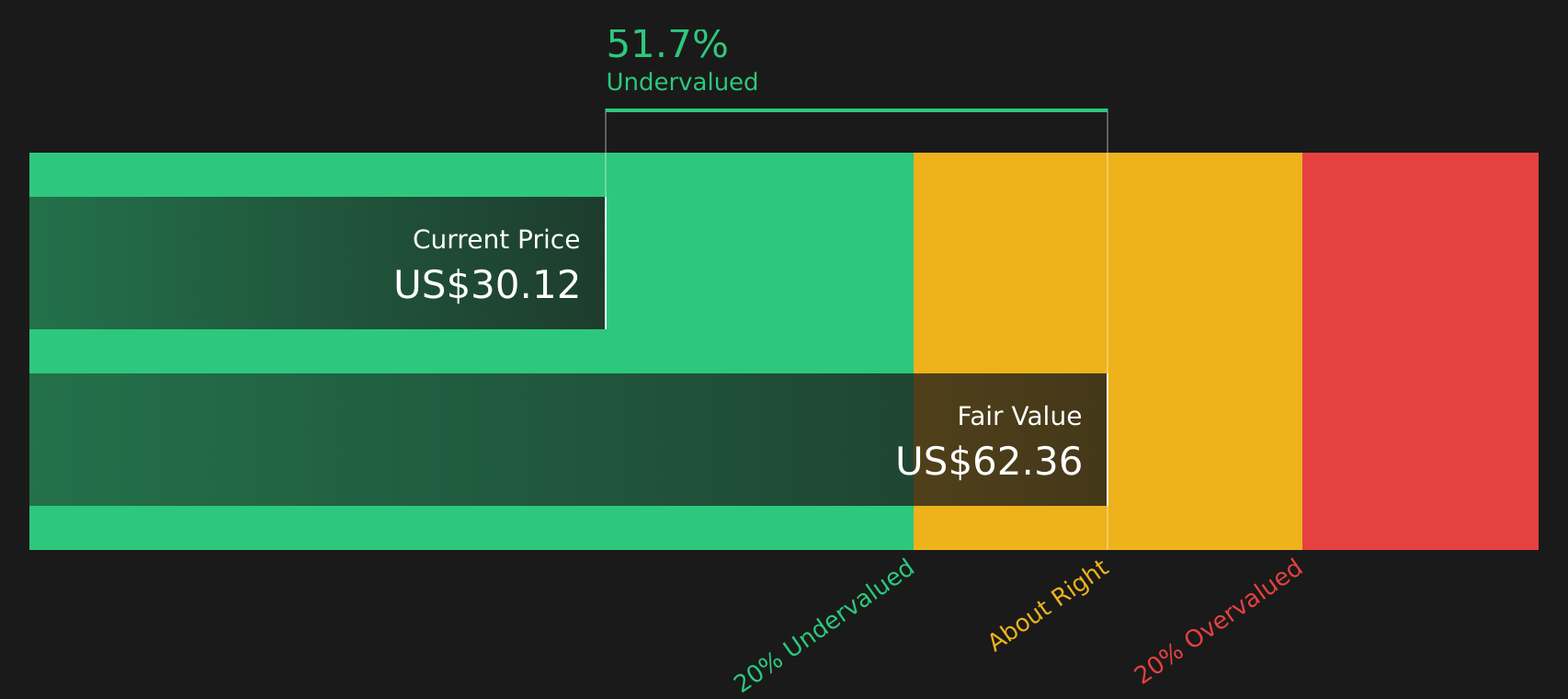

The market is treating Tango Therapeutics like a premium stock on a P/B of 11.1x, yet the SWS DCF model suggests a different picture, with an estimated future cash flow value of $62.47 per share versus the current $29.94 price, or about 52.1% below that estimate.

When one method flags Tango Therapeutics as expensive and another suggests it is trading well below a cash flow based value, it raises the question of which signal should carry more weight for you as an investor.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tango Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals around Tango Therapeutics, do you want to let the market decide the story for you, or test the numbers yourself by weighing up the company’s potential rewards against its real risks through 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Tango Therapeutics?

If the Tango Therapeutics story has sharpened your focus, now is the time to widen your watchlist and pressure test fresh ideas before the next big move.

- Spot underappreciated opportunities by checking companies that currently screen as 41 high quality undervalued stocks.

- Strengthen your income core by reviewing stocks highlighted as 8 dividend fortresses.

- Stay one step ahead by scanning the screener containing 18 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.