Is the G-III Licensing Fight Reshaping the Earnings Quality Narrative for PVH (PVH)?

PVH Corp. PVH | 0.00 |

- PVH Corp. previously declared a quarterly dividend of US$0.0375 per share, payable on June 24, 2026, with both ex-dividend and record dates on June 3, 2026, while confronting higher oil-driven supply chain costs and pressure on margins across the apparel sector.

- At the same time, PVH’s intensifying legal dispute with G-III over Calvin Klein and Tommy Hilfiger licenses, alongside concerns about debt and foreign-exchange-driven growth, raises fresh questions about the resilience and quality of its earnings profile.

- We’ll now examine how the escalating G-III licensing dispute and its operational risks reshape PVH’s existing investment narrative and risk balance.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

PVH Investment Narrative Recap

To own PVH today, you need to believe its Calvin Klein and Tommy Hilfiger focus, cost actions, and brand investment can translate a volatile earnings profile into steadier cash generation. In the near term, the most important catalyst is whether management can protect margins as oil-driven freight costs and tariffs bite, while the biggest risk is that the G III legal fight distracts leadership and weakens key U.S. wholesale relationships. The latest dividend affirmation does not materially change that balance.

The most relevant recent development here is the escalating G III licensing dispute, with PVH alleging contractual breaches that hurt the Calvin Klein and Tommy Hilfiger brands and prompting security measures around alleged threats. For a business still heavily reliant on these two labels and on wholesale channel health, how this legal battle evolves could influence both near term earnings volatility and the longer term payoff from PVH’s brand elevation and direct to consumer push.

Yet behind this, investors should also be aware of how FX reliant growth and PVH’s debt load could interact with any prolonged legal or margin pressure...

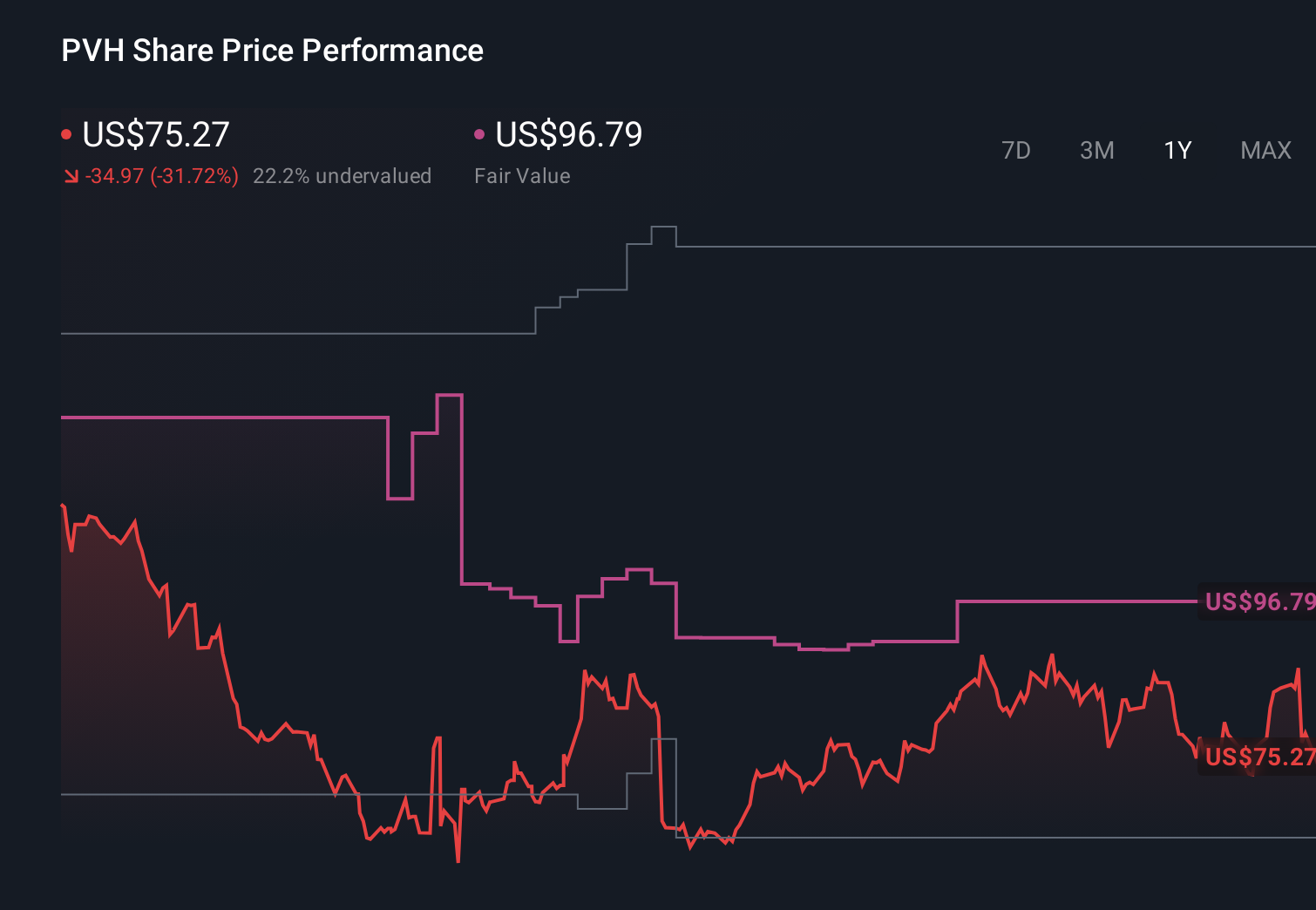

PVH's narrative projects $9.4 billion revenue and $707.7 million earnings by 2028. This requires 2.3% yearly revenue growth and about a $239 million earnings increase from $468.5 million today.

Uncover how PVH's forecasts yield a $96.79 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some higher conviction analysts were assuming PVH could lift margins and reach about US$680.5 million in earnings by 2028, which is far more optimistic than consensus and could be tested by the recent legal and cost headlines.

Explore 4 other fair value estimates on PVH - why the stock might be worth just $96.79!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PVH research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.