Is There an Opportunity in Adobe After 24.9% Drop in 2025?

Adobe Systems Incorporated ADBE | 241.70 | +0.14% |

- Wondering whether Adobe’s current share price represents a true bargain or just another blip in the market? You’re not alone. Let's dig in and see what’s really happening beneath the surface.

- Adobe’s stock price has slipped 0.6% over the past month and is down 24.9% year-to-date, signaling shifting investor sentiment and raising fresh questions about the company’s potential future returns.

- Some of this volatility has been fueled by major industry headlines and shifts in the competitive landscape, with increased AI adoption and moves by rivals stirring up investor excitement and concern. Tech sector momentum and regulatory chatter have kept Adobe firmly in the spotlight, adding extra context to the recent moves.

- When it comes to value, Adobe scores 5 out of 6 on our valuation checks, suggesting it passes most but not all our undervaluation criteria. Next, we’ll break down the classic valuation methods, and hint at a smarter way to judge value that you’ll want to see at the end.

Approach 1: Adobe Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's true worth by projecting its future cash flows and then discounting them back to today’s dollars. This approach helps investors judge whether a stock is currently under or overvalued, based on its potential to generate cash in the years ahead.

For Adobe, the latest reported Free Cash Flow stands at $9.5 billion. Analysts project continued growth, with free cash flow expected to rise to $13.3 billion by 2029. Notably, projections beyond five years are extrapolated by Simply Wall St, drawing on historic trends and industry expectations to estimate Adobe’s potential over the next decade.

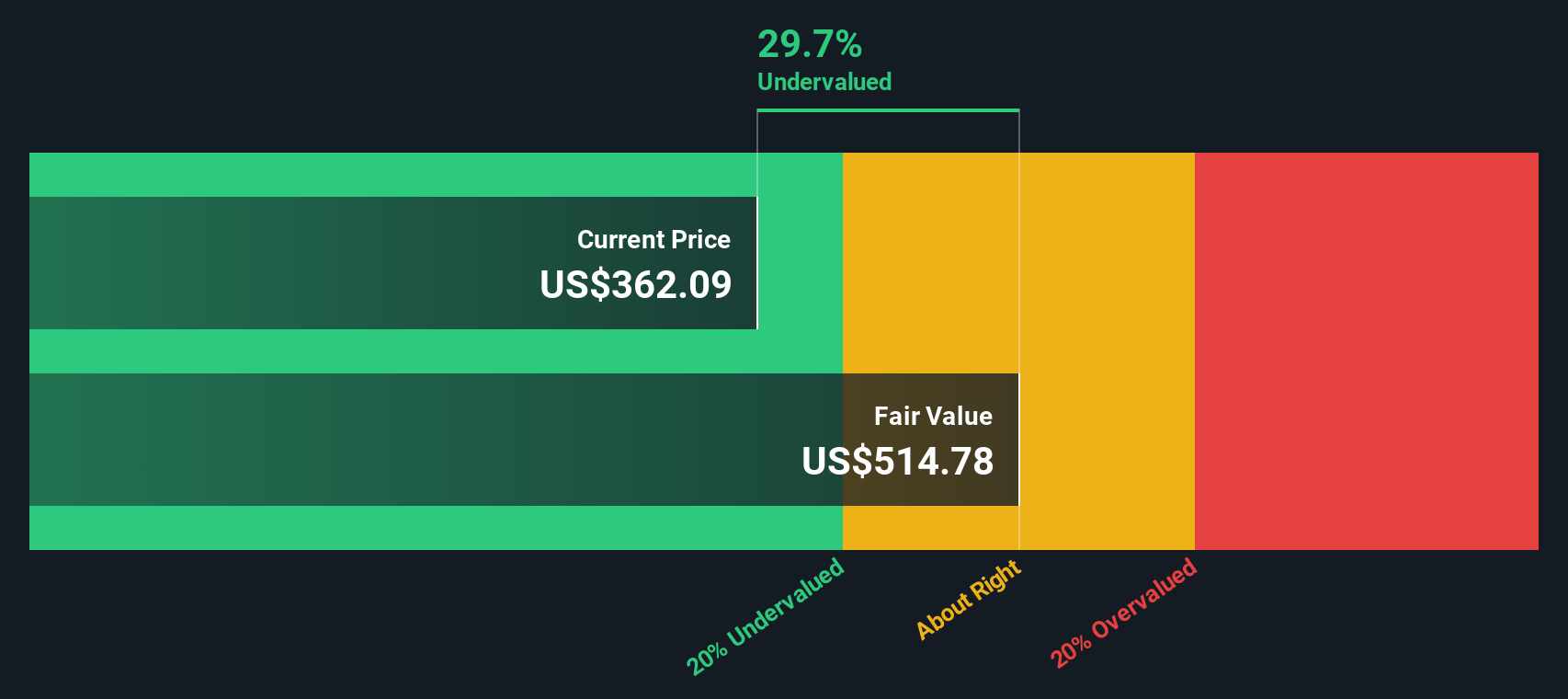

The DCF model arrives at a fair value estimate of $580.34 per share for Adobe. At its current market price, this calculation suggests the stock is trading at a 42.9% discount. This implies it is substantially undervalued compared to what it could be worth if these cash flow projections hold true.

This significant discount points to an opportunity for investors, provided Adobe continues its strong cash generation as forecast and market conditions remain supportive.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Adobe is undervalued by 42.9%. Track this in your watchlist or portfolio, or discover 885 more undervalued stocks based on cash flows.

Approach 2: Adobe Price vs Earnings

The Price-to-Earnings (PE) ratio is widely used to value established, profitable companies like Adobe because it provides a direct way to compare what investors are paying for each dollar of current earnings. It is particularly effective for businesses with a steady earning profile, helping investors quickly benchmark relative value within an industry.

A company’s “normal” or “fair” PE ratio depends on factors such as its growth prospects, risk profile, and how reliably it generates profits. Fast-growing, less risky, or highly profitable companies tend to command higher PE ratios, while slower growth or riskier firms often trade at lower multiples.

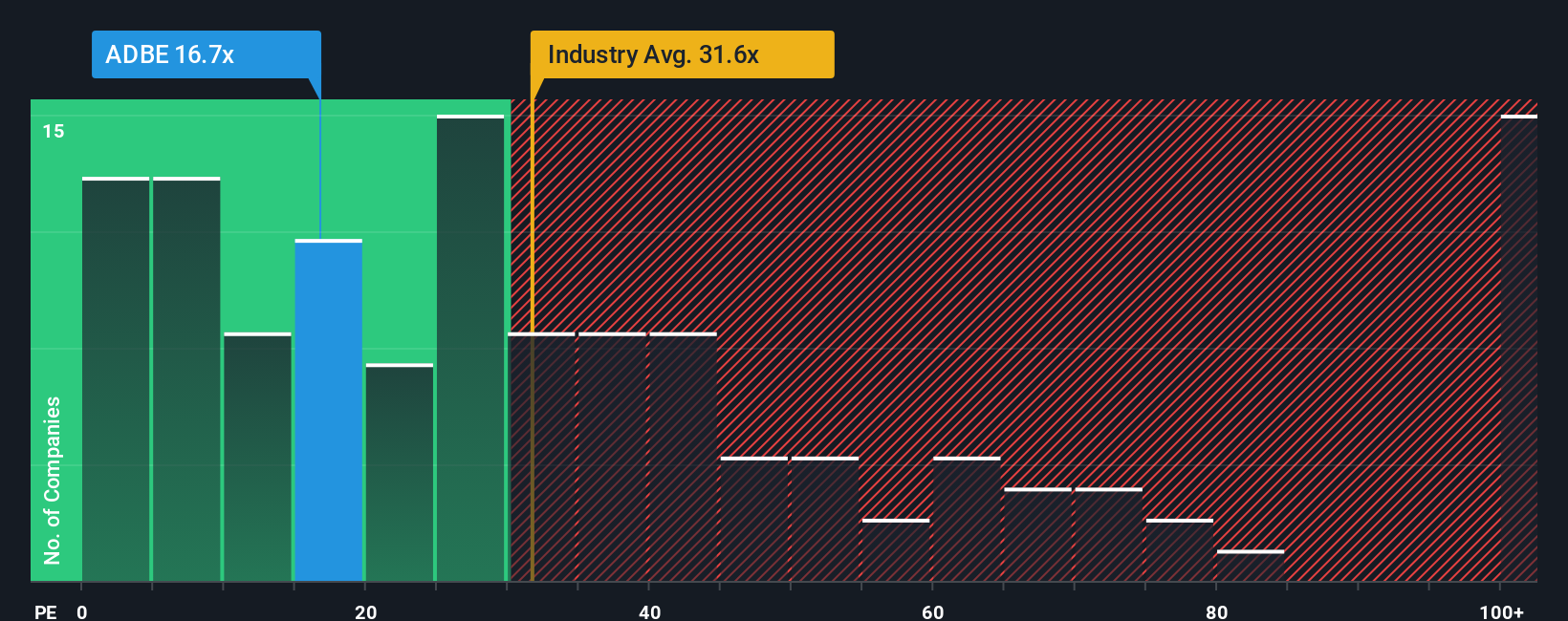

Adobe’s current PE ratio sits at 19.9x. This is notably below the Software industry average of 31.2x and lags well behind the average across its peers at 56.4x. However, relying solely on these averages can miss the nuances that really matter. That is where Simply Wall St’s Fair Ratio comes in, a proprietary benchmark that blends Adobe’s earnings growth, profit margins, industry context, company size, and risk profile to determine what PE multiple is truly justified for its circumstances.

Simply Wall St’s calculated Fair Ratio for Adobe is 38.2x. This individualized approach outperforms simple industry or peer comparisons by incorporating more nuanced, company-specific data. Comparing this Fair Ratio to Adobe’s actual 19.9x, the stock appears meaningfully undervalued based on its expected fair multiple.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Adobe Narrative

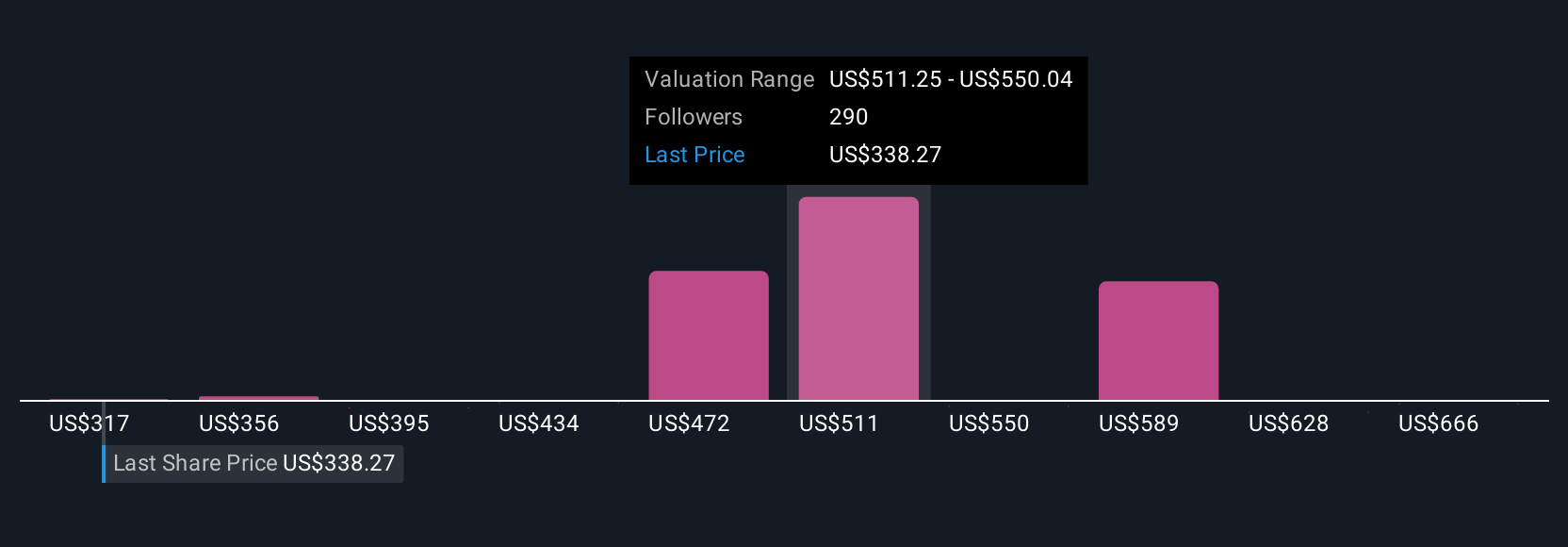

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your perspective or story about a company, backed by your own numbers—your assumptions for future revenue growth, profit margins, and the fair value you believe is justified.

Instead of relying solely on formulas or ratios, Narratives empower you to connect Adobe’s story to a financial forecast and calculate what you think its shares are truly worth. This approach is easy and accessible. On Simply Wall St’s Community page, millions of investors use Narratives to craft, share, and update their investment stories as new news or earnings roll in.

Narratives help guide buy or sell decisions by showing you the fair value based on your forecast and then comparing it to today’s share price, making what is “undervalued” or “overvalued” personal and dynamic rather than static. As the facts change, your Narrative can update automatically, ensuring your analysis stays relevant.

For example, some investors believe Adobe’s fair value could be as high as $605 if they expect rapid AI-driven growth and big profit gains. Others see $380 as appropriate in a tougher, lower-growth scenario. In other words, your Narrative lets you invest according to your view of the future and not just the crowd’s.

Do you think there's more to the story for Adobe? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.