Is There Still Opportunity in Lam Research After Surging 97% in 2024?

Lam Research Corporation LRCX | 222.01 212.55 | +3.91% -4.26% Pre |

If Lam Research is on your radar, you are definitely not alone. With the chip industry constantly in the headlines and stocks in the semiconductor equipment sector drawing plenty of attention, deciding what to do with Lam right now is a hot topic for keen investors. The stock has been making impressive moves, surging 8.4% in just the past week, up a striking 16.8% over the last month, and nearly doubling year-to-date with a 96.5% rally. Zoom out, and the five-year gain stands at a huge 325.2%. Part of this momentum has been driven by renewed optimism in tech hardware as global demand for advanced chips and fabrication equipment climbs, with markets continuing to bet on the increasing importance of innovation in this space.

Of course, such steep climbs often prompt the next big question: is the stock still a deal, or is the price starting to race ahead of itself? To help answer that, we look at Lam’s valuation score, which lands at 2 out of 6 by our checks. This is hardly a screaming bargain, but certainly not the most expensive name out there. Each check highlights how the company stacks up against industry norms in areas like price to earnings, cash flow, and balance sheet strength.

In this next section, we will take a closer look at each of those valuation methods, seeing where Lam shines and where it might have more to prove. And if you are looking for an even smarter way to size up this stock, stick around for our final verdict. It could change how you see valuation entirely.

Lam Research scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Lam Research Discounted Cash Flow (DCF) Analysis

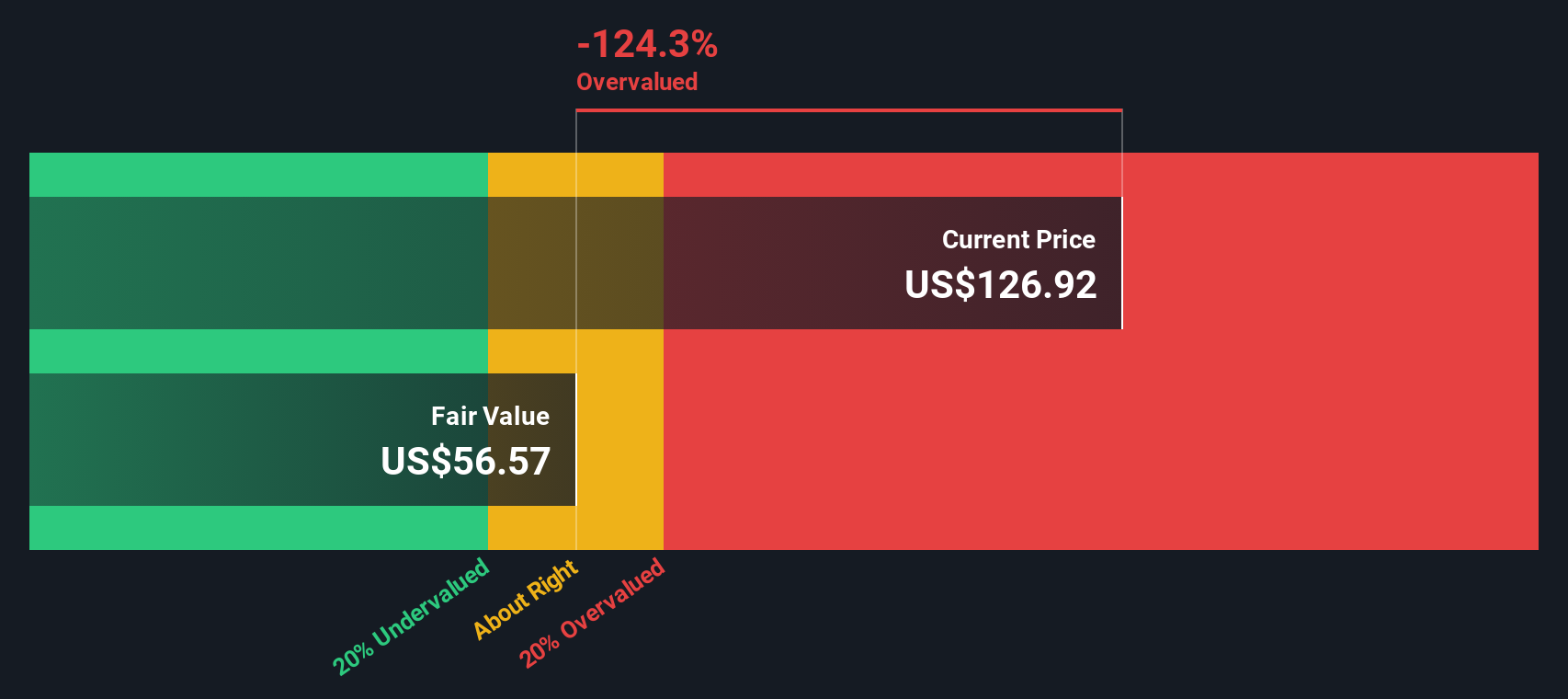

The Discounted Cash Flow (DCF) model estimates the value of a company by projecting its future cash flows and discounting them back to today's value. This approach is widely used to gauge whether a stock’s current price reflects its expected future earning power.

For Lam Research, the company’s most recent reported Free Cash Flow stands at approximately $5.6 Billion. Analyst estimates drive cash flow forecasts through 2030. After this period, Simply Wall St extrapolates the outlook. The projections call for steady growth, with Free Cash Flow estimated to reach around $7 Billion by 2030. These forecasts reflect confidence in Lam’s ongoing innovation and its ability to convert earnings into real cash.

After applying the DCF model, the estimated intrinsic value per share comes in at $58.48. At present, Lam Research’s stock trades at a substantial premium to this estimate. Specifically, the model implies the stock price is 143.4% above its fair value, suggesting the company is significantly overvalued based on forward-looking cash flow expectations.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lam Research may be overvalued by 143.4%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Lam Research Price vs Earnings

When it comes to valuing profitable companies like Lam Research, the Price-to-Earnings (PE) ratio stands out as a widely preferred metric. The PE ratio helps investors gauge how much the market is willing to pay for each dollar of the company's earnings. This is a particularly useful measure for established businesses with steady profit streams.

It's important to understand that what counts as a “fair” PE ratio depends on both growth expectations and perceived risks. Fast-growing companies or those with robust competitive advantages often trade at higher multiples, while more mature or riskier companies usually command lower ones. This "normal" ratio sets the foundation for evaluating whether a stock is attractively priced compared to its profit potential.

Currently, Lam Research trades at a PE of 33.5x. When you compare this to the Semiconductor industry average of 35.6x and a peer group average of 39.0x, Lam’s valuation looks a bit more conservative. However, Simply Wall St’s proprietary Fair Ratio offers an even more precise benchmark. Factoring in elements like Lam’s earnings growth, profit margins, industry conditions, market capitalization, and company-specific risks, the Fair Ratio for Lam comes in at 32.2x. Unlike a simple peer or industry comparison, the Fair Ratio adjusts for the unique opportunities and headwinds facing Lam. This makes it a deeper, more tailored guide for investors sizing up this stock.

With Lam’s PE ratio just slightly above its Fair Ratio, the company’s shares are priced close to fair value based on its underlying fundamentals.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lam Research Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story or perspective about a company’s future, explaining not just what you think it’s worth, but also why. This is anchored by your assumptions about revenue, margins, growth rates, and risk. Narratives link the business story to a financial forecast and then to a fair value, helping you turn a company’s outlook into actionable numbers.

With Simply Wall St’s platform, Narratives are easy to create and use within the Community page where millions of investors share their viewpoints. You can quickly compare your own Narrative-driven fair value to the current share price, making buy or sell decisions that are personal, logical, and transparent. Plus, as news, results, or new forecasts arrive, Narratives update dynamically to keep your analysis relevant in real time.

For example, some investors looking at Lam Research see surging demand and expanding innovation, so they set higher fair value estimates. Others focus on competition or geopolitical risks and arrive at much lower targets. Narratives make these different perspectives visible and comparable, letting you make smarter, conviction-driven investment choices based on what you truly believe will happen next.

Do you think there's more to the story for Lam Research? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.