Is Travelers Companies (TRV) Fairly Valued As Analysts Split On Growth And Margins?

Travelers Companies, Inc. TRV | 0.00 |

Travelers Companies (TRV) is in focus after Barclays downgraded the stock on concerns about slowing growth and margin pressures in property and casualty insurance, while other firms took a more supportive stance.

Even with the recent downgrade, Travelers Companies has seen strong momentum, with a 1-month share price return of 9.15% and a 1-year total shareholder return of 26.31%. The 5-year total shareholder return of 138.56% reflects a sustained long-term gain.

If analyst debate around Travelers has you reviewing the broader insurance space, it can be useful to compare with other financials and insurers and discover 20 top founder-led companies

With Travelers Companies trading at $327.37, above the average analyst price target of $312.91 yet flagged by some as undervalued on intrinsic metrics, investors face a key question: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 4.6% Overvalued

With Travelers Companies last closing at $327.37 compared with a narrative fair value of $312.91, the current setup hinges on how future underwriting, earnings and capital returns are expected to evolve under this view.

Analysts are assuming Travelers Companies's revenue will decrease by 1.5% annually over the next 3 years. Analysts assume that profit margins will shrink from 15.4% today to 11.5% in 3 years time.

Read the complete narrative. Read the complete narrative.

Want to understand why a company with shrinking margins and lower projected earnings still lands near this fair value band? The narrative focuses on how future profit levels, valuation multiples and share count changes interact over time. The tension between softer top line assumptions and a higher future earnings multiple is central here, with buybacks and discount rates doing quiet but important work in the background.

Result: Fair Value of $312.91 (OVERVALUED)

However, the narrative on Travelers Companies could be tested if catastrophe losses climb faster than pricing adjustments, or if auto retention and personal lines margins stay under pressure.

Another View: Travelers Companies Through A Cash Flow Lens

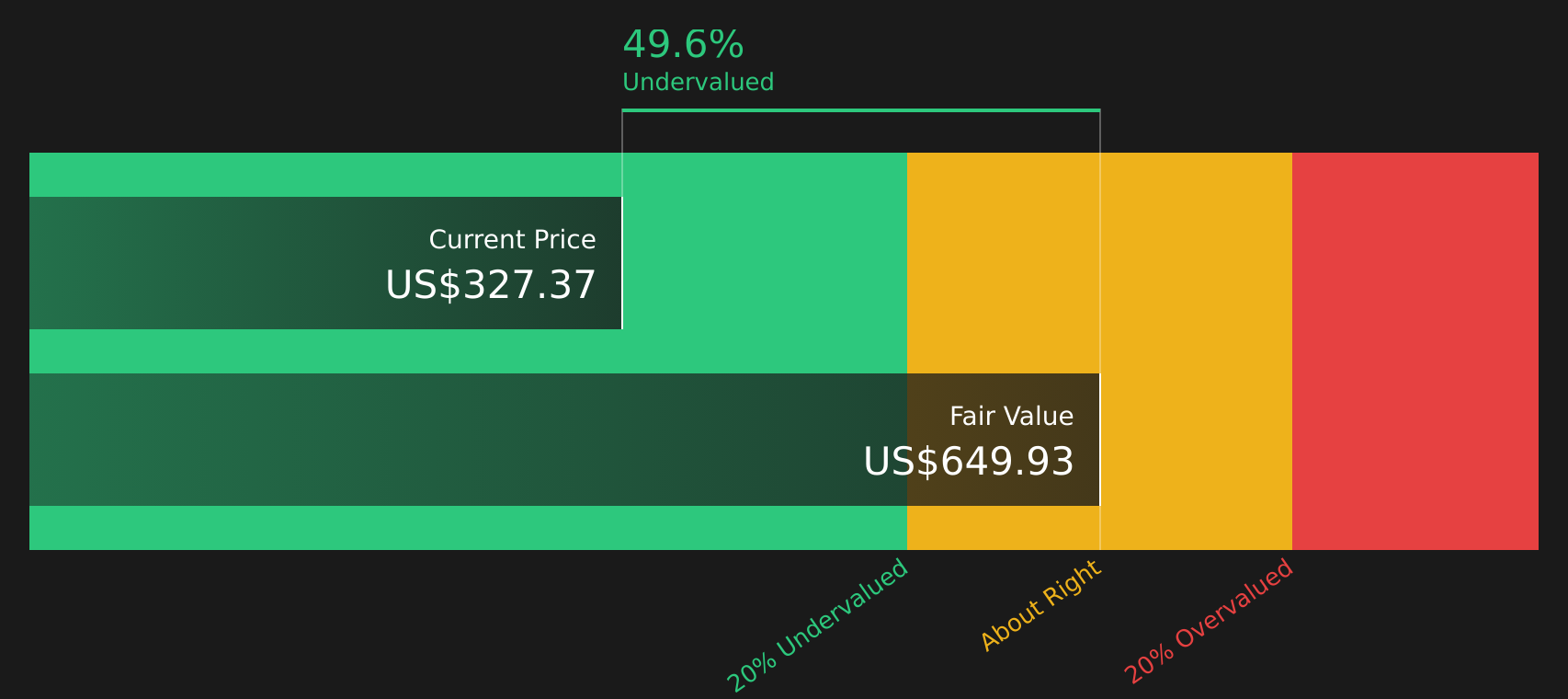

While the analyst narrative pegs Travelers Companies as about 4.6% overvalued at $327.37 versus a fair value of $312.91, the Simply Wall St DCF model points in the opposite direction. On that cash flow view, TRV trades at roughly a 49.6% discount to an estimated fair value of $649.93. This raises a simple question for you: which story about future cash generation feels more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Travelers Companies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment around Travelers Companies divided between risk and reward, this is the moment to check the assumptions yourself and move quickly using the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Travelers Companies?

Once you have formed a view on Travelers Companies, do not stop there. Use targeted stock lists to spot other opportunities that could sharpen your portfolio.

- Hunt for potential mispriced opportunities by reviewing companies highlighted in the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on stocks featured in the 8 dividend fortresses.

- Limit downside risks by concentrating on companies selected in the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.