Is Twilio’s (TWLO) RCS Rollout and S&P Inclusion Reshaping Its Investment Case?

Twilio TWLO | 0.00 |

- Earlier this past week, Twilio announced the global launch of its Rich Communication Services (RCS) messaging, now available to over 349,000 active customer accounts, and revealed its addition to the S&P MidCap 400 index, replacing Amedisys Inc.

- An interesting development is that analyst sentiment has also turned more positive, with upward revisions to earnings forecasts and growing confidence in Twilio’s capacity for long-term product and fundamental growth.

- We’ll explore how Twilio’s global RCS rollout and market index inclusion shape its investment narrative amid rising AI-driven communications demand.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Twilio Investment Narrative Recap

To own Twilio, an investor needs conviction in the accelerating shift toward AI-powered and omnichannel communications, and belief that Twilio can convert digital demand into both revenue growth and margin improvement. While the recent global RCS launch and S&P MidCap 400 index inclusion enhance the story, these developments do not materially affect the immediate catalyst, which remains Twilio's ability to grow higher-margin software and data products, or the principal risk: structural margin pressure from low-margin messaging and rising carrier costs.

The most relevant announcement is Twilio’s global RCS rollout, which provides richer messaging capabilities to over 349,000 customer accounts and supports its pursuit of higher engagement and value-added services. Although RCS may open new monetization streams and highlights product innovation, the effect on addressing margin compression from messaging mix will take time, and therefore has limited near-term impact on Twilio’s key risk or catalyst.

Yet, before assuming these strengths are sustainable, investors should be aware that growing revenues alone may not offset ongoing pressure on gross margins if...

Twilio's narrative projects $5.9 billion revenue and $449.9 million earnings by 2028. This requires 7.9% yearly revenue growth and a $429.7 million earnings increase from $20.2 million today.

Uncover how Twilio's forecasts yield a $130.88 fair value, a 22% upside to its current price.

Exploring Other Perspectives

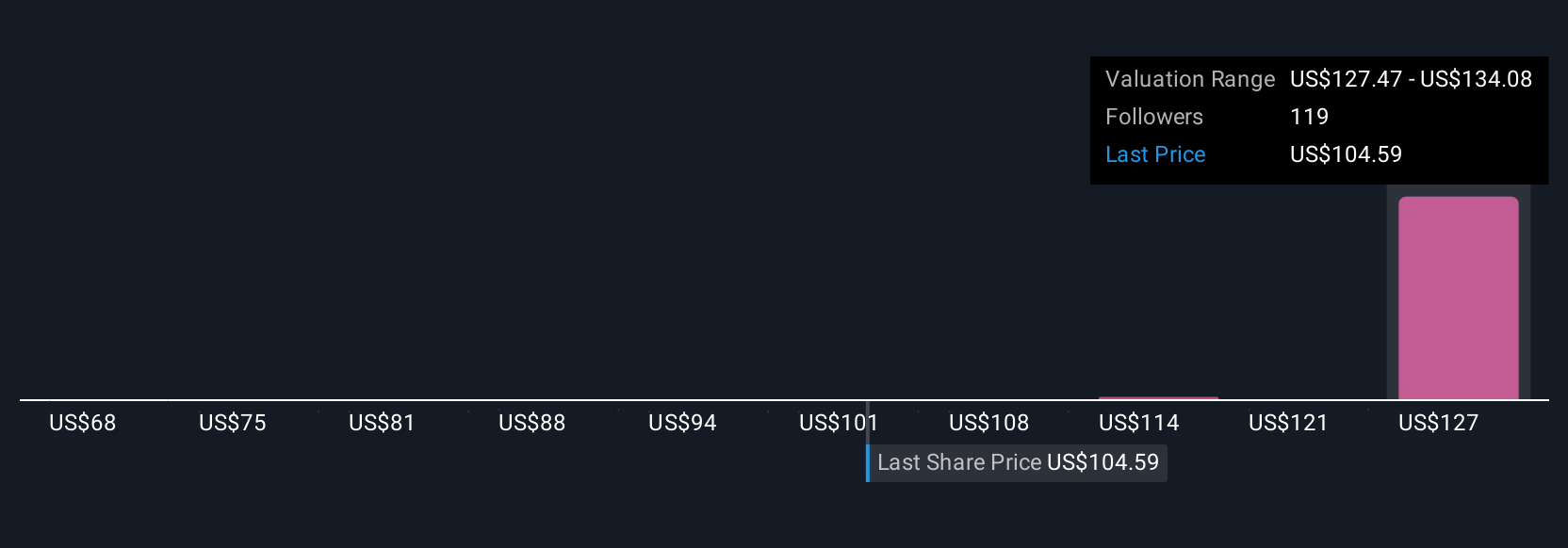

Simply Wall St Community members provided 7 fair value estimates ranging from US$68 to US$133.06, underlining wide differences in opinion. While many see Twilio’s software innovation as a growth lever, sustaining margins remains key to long-term performance, consider how this could affect future outcomes as you look through other viewpoints.

Explore 7 other fair value estimates on Twilio - why the stock might be worth 37% less than the current price!

Build Your Own Twilio Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Twilio research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Twilio research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Twilio's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.