Is Upbeat Q1 Guidance Altering The Investment Case For Bank of America’s Earnings Power (BAC)?

Bank of America Corp BAC | 0.00 |

- In recent days, Bank of America reported strong Q1 results, raised its full-year net interest income guidance, and highlighted momentum across trading, investment banking, and wealth management, while continuing to tap bond markets with multiple senior unsecured note offerings.

- These updates, alongside the bank’s large, low-cost consumer deposit base and management’s confident commentary on revenue drivers, have reinforced investor focus on Bank of America’s earnings power and balance sheet funding advantages.

- We’ll now examine how the raised net interest income guidance and stronger trading outlook may influence Bank of America’s investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Bank of America Investment Narrative Recap

To own Bank of America, you have to trust in a wide, low cost deposit base, solid credit discipline, and relatively efficient fee businesses to support earnings across cycles. The raised net interest income guidance and stronger trading outlook sharpen the near term focus on interest rate sensitivity as a key catalyst, while credit quality and funding costs remain the biggest swing factors; the latest updates do not fundamentally change those risks.

Among the recent announcements, Bank of America’s series of senior unsecured note offerings stands out as most relevant. These fixed rate issues, layered across maturities from 2027 to 2046, sit alongside the bank’s large consumer deposit base and highlight how management is shaping its funding mix at different points on the yield curve, a backdrop that matters for how investors think about net interest income as a short term driver.

However, investors should also be aware that increased competition for deposits could pressure Bank of America’s low cost funding advantage and...

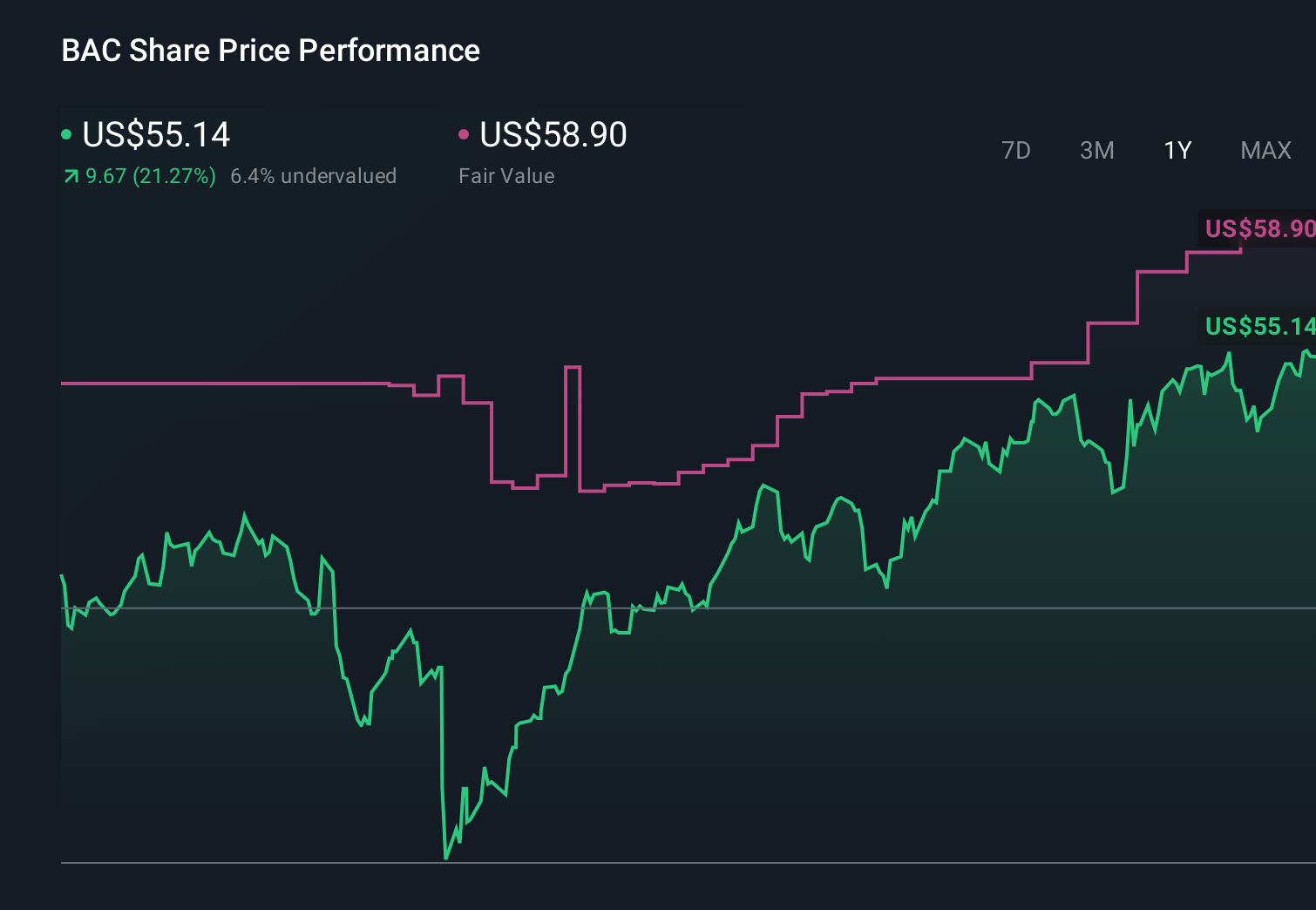

Bank of America's narrative projects $133.8 billion revenue and $36.7 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $6.4 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $63.16 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community sit between US$58.69 and US$68.24, showing how far opinions can spread. When you weigh those views against Bank of America’s focus on digital and AI driven efficiencies as a potential earnings catalyst, it underlines why checking several perspectives on the bank’s performance and risks can be useful before making up your mind.

Explore 5 other fair value estimates on Bank of America - why the stock might be worth just $58.69!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bank of America research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.