Is Uranium Energy (UEC) Pricing Look Stretched After 1 Year Return Of 138%

Uranium Energy Corp. UEC | 13.57 | +1.04% |

- If you are wondering whether Uranium Energy's share price really lines up with its underlying value, this article will walk through what the current numbers actually suggest.

- The stock last closed at US$18.82, with returns of 9.5% over 7 days, 50.8% over 30 days, 43.6% year to date and 138.2% over 1 year, while the 3 year return is 376.5% and the 5 year figure is very large.

- These moves sit against an ongoing stream of sector and company specific news that keeps uranium names in focus, including recurring attention on uranium supply, demand and policy themes that often frame investor sentiment. For Uranium Energy, this backdrop gives useful context for thinking about whether the current price is stretching expectations or not.

- On Simply Wall St's valuation checks, Uranium Energy currently has a valuation score of 0 out of 6, so next we will look at how different valuation approaches interpret that result and then finish with an even more practical way to think about the company's value.

Uranium Energy scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

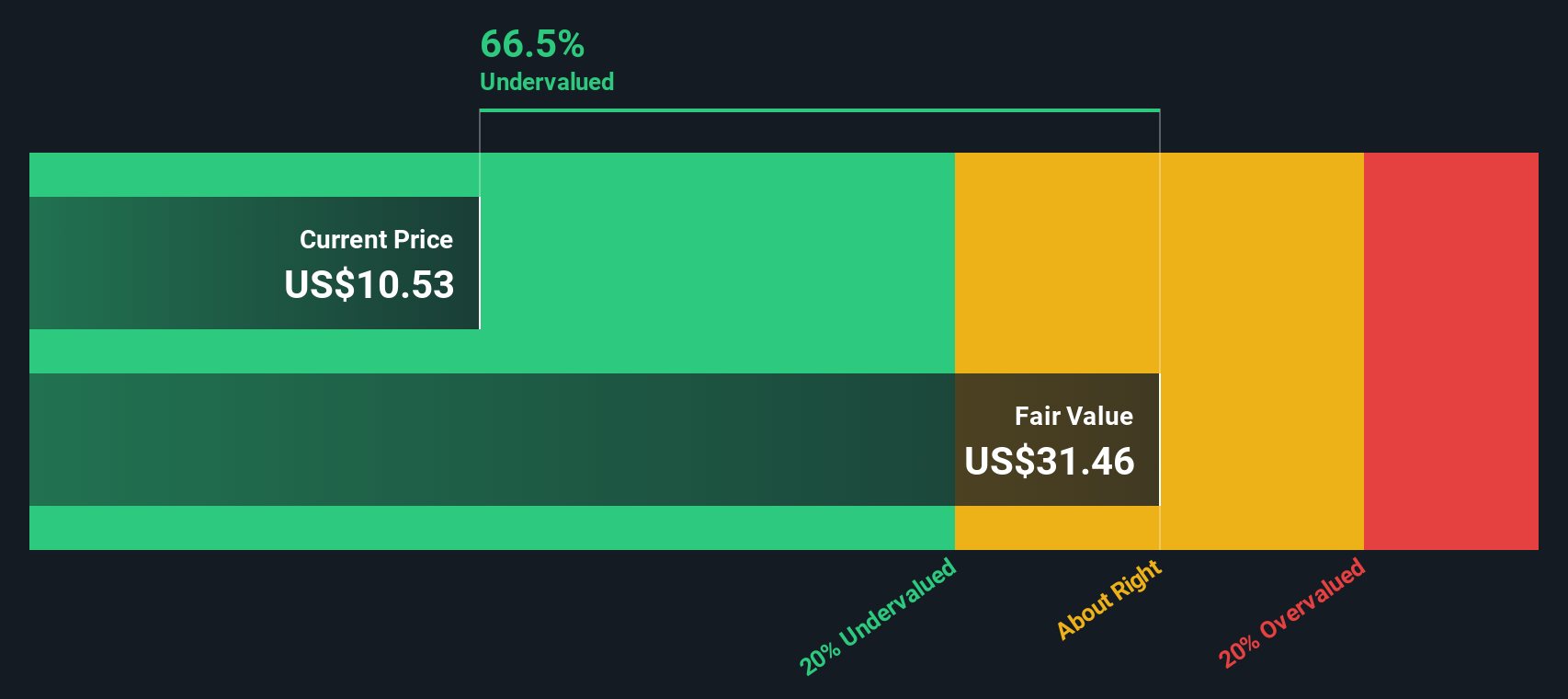

Approach 1: Uranium Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today to arrive at an estimated intrinsic value per share.

For Uranium Energy, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow was a loss of $90.39 million, so the model leans heavily on future projections. Analyst inputs and extrapolations point to free cash flow of $95.50 million by 2028, with Simply Wall St extending that path out a full 10 years using its own growth assumptions.

Pulling all of those projected cash flows into today’s dollars, the DCF model arrives at an estimated intrinsic value of about $12.49 per share. With the recent share price at US$18.82, the DCF output implies Uranium Energy is around 50.7% overvalued on this metric.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Uranium Energy may be overvalued by 50.7%. Discover 876 undervalued stocks or create your own screener to find better value opportunities.

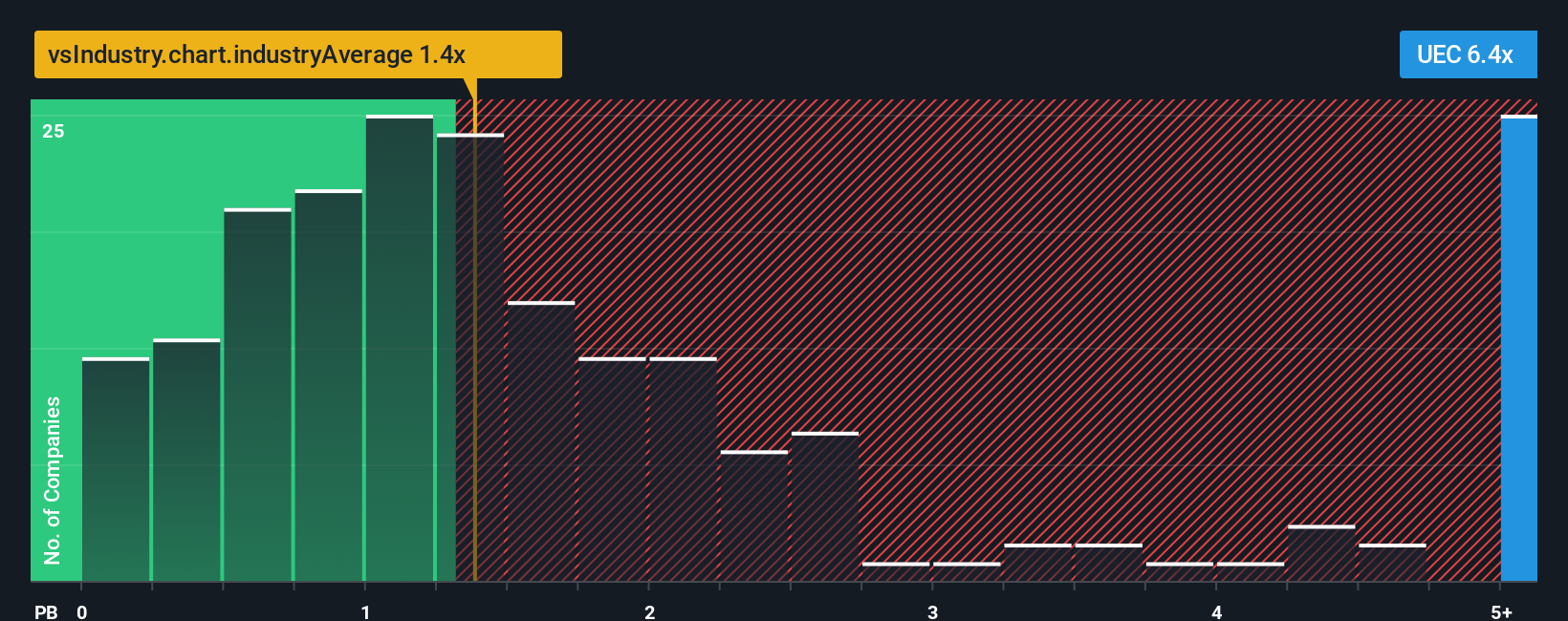

Approach 2: Uranium Energy Price vs Book

For companies where profits are limited or volatile, price based on book value can be a useful cross check, because it anchors the valuation to the net assets on the balance sheet rather than earnings or revenue swings.

In simple terms, the higher the perceived growth potential and the lower the perceived risk, the more investors may be willing to pay above book value. As a result, a “normal” or “fair” P/B tends to be higher for businesses seen as stronger or more resilient. The opposite can also be true if risks are higher or assets are harder to value.

Uranium Energy currently trades on a P/B of 6.93x. That sits above the Oil and Gas industry average P/B of 1.43x and above the peer group average of 4.93x that is provided here. Simply Wall St also uses a proprietary “Fair Ratio” to estimate what a more tailored P/B might look like for Uranium Energy, based on factors such as earnings growth, margins, industry, market value and risk profile. Because it is customised to the company, that Fair Ratio can be more informative than a broad comparison with peers or the sector. With no Fair Ratio value supplied here, the P/B comparison alone cannot show whether the shares are overvalued or undervalued.

Result: ABOUT RIGHT

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Uranium Energy Narrative

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St that means using Narratives, which let you spell out your own story for Uranium Energy by linking your assumptions for future revenue, earnings and margins to a financial forecast, a fair value, and then a clear comparison between fair value and the current price to help you decide what action, if any, makes sense.

Instead of only relying on models like DCF or P/B, a Narrative lets you say why you think the business will perform a certain way and then see those beliefs turned into numbers inside the Community page. There, millions of investors share and update their views as new information such as news or earnings arrives, so the Narrative you follow can adjust in real time.

Narratives can differ a lot. For example, one Uranium Energy Narrative might assume a relatively high fair value based on optimistic uranium demand scenarios, while another might sit at the low end with more cautious expectations for pricing and project timing. You can weigh both against the current share price to decide which story you find more convincing.

Do you think there's more to the story for Uranium Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.