Is Walker & Dunlop’s (WD) Latest Opportunity Zone Refi Shaping Its Role in Specialized CRE Finance?

Walker & Dunlop, Inc. WD | 0.00 |

- Walker & Dunlop, Inc. recently arranged a US$105,000,000 refinancing loan for Maeve, a 297-unit luxury high-rise with over 10,000 square feet of retail, located in a federally designated Economic Opportunity Zone in Raleigh’s Warehouse District.

- This transaction underscores Walker & Dunlop’s role in complex opportunity zone financings that blend high-end urban living, mixed-use amenities, and tax-advantaged community investment.

- Next, we’ll examine how arranging a US$105,000,000 refinancing for an opportunity zone luxury project may influence Walker & Dunlop’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe in its ability to convert advisory reach in commercial real estate into consistent fee income, despite recent earnings pressure and a rich valuation multiple. The Maeve US$105,000,000 refinancing adds to deal momentum in multifamily and mixed-use, but on its own it does not materially change the near term dependency on transaction volumes or the key risk from interest rate driven swings in refinancing activity.

Among recent announcements, the upcoming Q1 2026 earnings release on May 7 stands out as most relevant, because it will show whether transactions like Maeve and other recent financings are starting to support margins after a period of weaker profitability. Investors watching Maeve as a proof point for Walker & Dunlop’s ability to win complex, tax-advantaged mandates may look to that update for clearer evidence that higher activity is translating into healthier earnings rather than just larger, lower fee deals.

Yet even with deals like Maeve, investors should be aware that Walker & Dunlop’s sensitivity to interest rate driven transaction slowdowns and margin pressure could still...

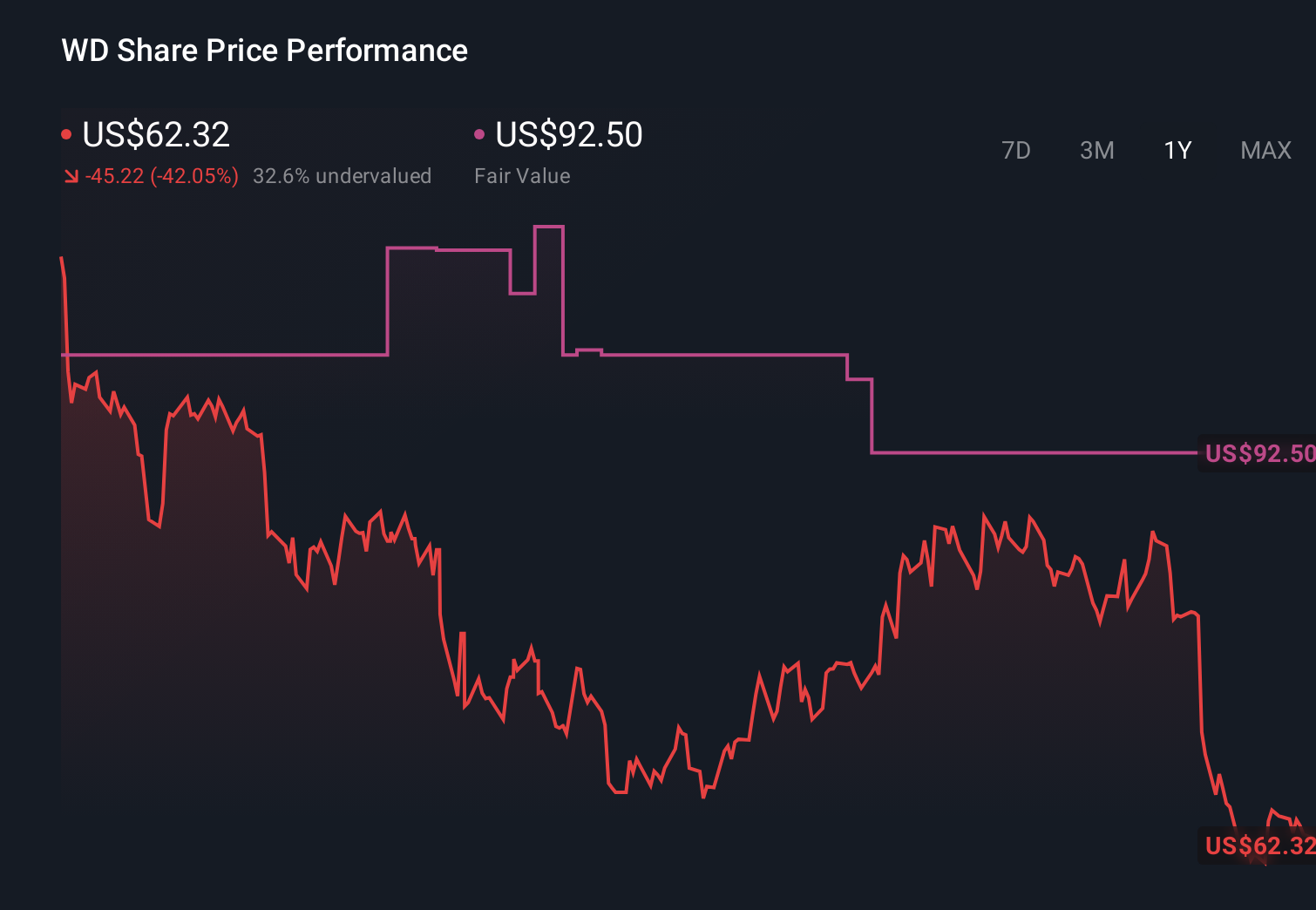

Walker & Dunlop's narrative projects $1.6 billion revenue and $202.2 million earnings by 2029.

Uncover how Walker & Dunlop's forecasts yield a $67.50 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Walker & Dunlop range from US$32.38 to US$67.50, underscoring how far apart individual views can be. When you set those opinions against the company’s exposure to rate driven transaction swings and margin pressure, it becomes even more important to compare several perspectives before deciding how this stock might fit into your portfolio.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth as much as 31% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.