Is Warner Bros. Discovery Still a Bargain After Shares Jumped 143% in 2025?

Warner Bros. Discovery, Inc. Series A WBD | 27.32 | -0.62% |

- Curious if Warner Bros. Discovery is still a value play, or if the market is already onto its next blockbuster? Let's dig into where the stock might stand now.

- Shares have soared recently, climbing 26.6% over the last month and an eye-popping 143.2% in the past year. This signals renewed confidence and big expectations.

- Media headlines have spotlighted Warner Bros. Discovery's major streaming deals and content partnerships, painting a picture of a company making big moves in both digital and studio segments. These developments have energized investors and sparked speculation around future growth and industry positioning.

- Despite all the buzz, Warner Bros. Discovery scores just 0 out of 6 on our value checklist. This suggests the market may be pricing in lots of optimism already. Next, we'll break down those valuation approaches. Stick around, as we'll also share a smarter way to think about true value before you make your own call.

Warner Bros. Discovery scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

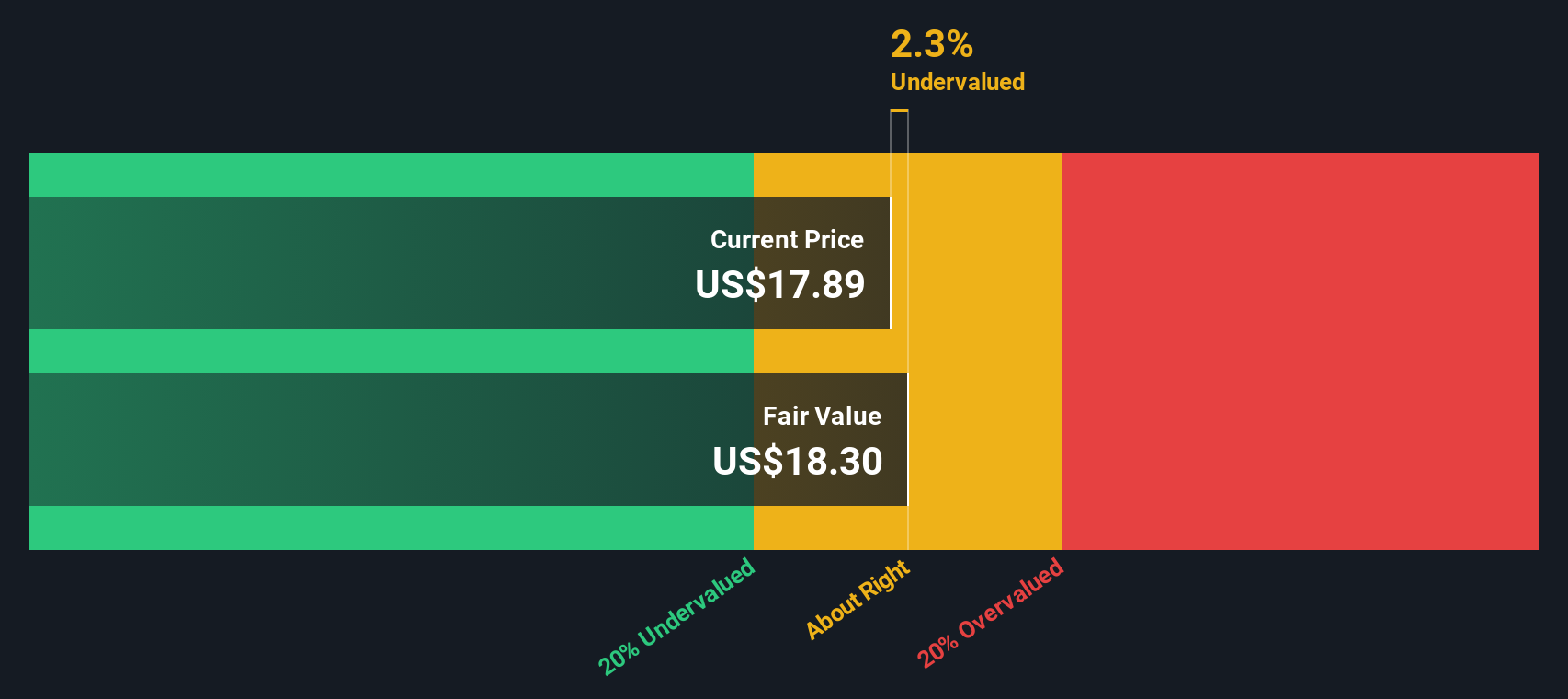

Approach 1: Warner Bros. Discovery Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model takes Warner Bros. Discovery’s estimated future cash flows and calculates what they are worth in today’s dollars. It projects how much cash the business will generate over time and discounts those cash flows back using a required rate of return, offering an estimate of what the company should be worth right now.

Currently, Warner Bros. Discovery generates $4.1 Billion in Free Cash Flow. Analyst estimates provide forecasts for the next five years, after which Simply Wall St extrapolates growth. By 2029, projected Free Cash Flow reaches $4.4 Billion, and by year ten, the model estimates $4.7 Billion. All cash flows are presented in US dollars to match reporting requirements.

Based on these projections, the DCF model calculates an intrinsic value of $19.60 per share. This is about 17.5% below the current market price, indicating the stock is overvalued according to this approach.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Warner Bros. Discovery may be overvalued by 17.5%. Discover 897 undervalued stocks or create your own screener to find better value opportunities.

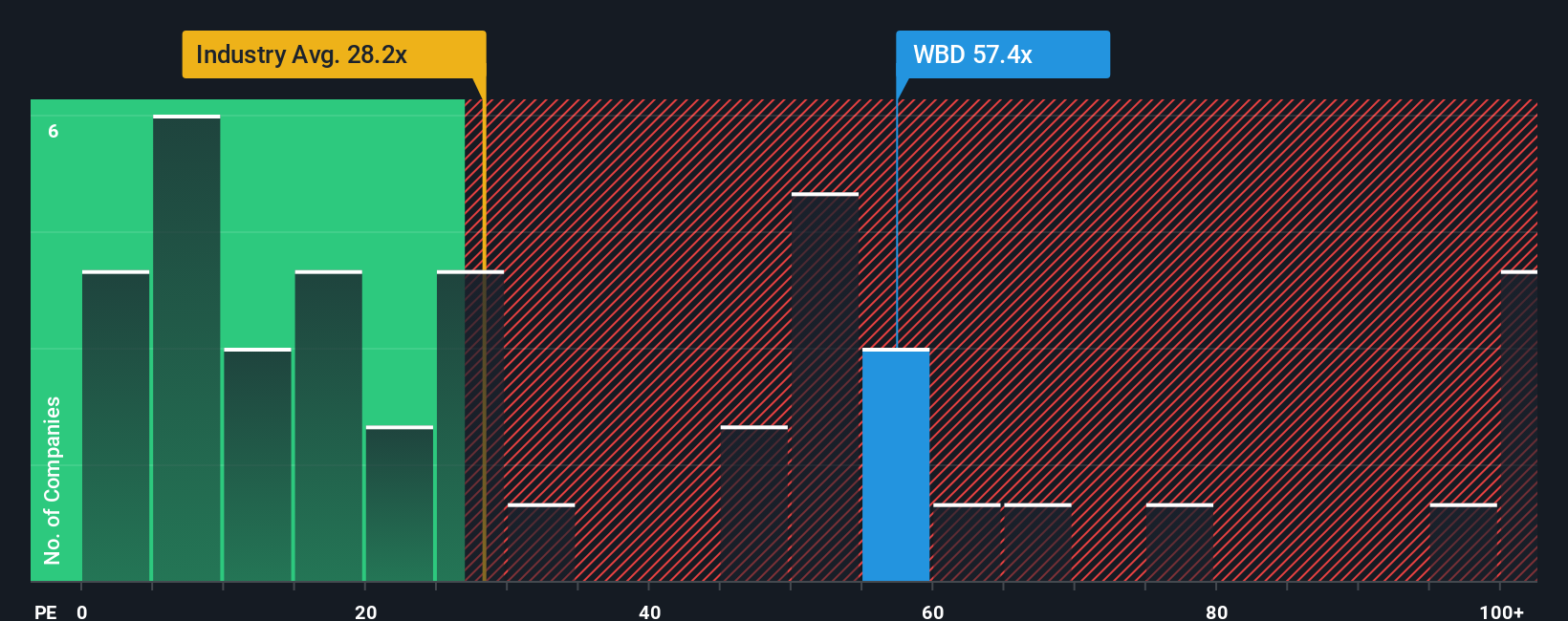

Approach 2: Warner Bros. Discovery Price vs Earnings

For profitable companies like Warner Bros. Discovery, the Price-to-Earnings (PE) ratio is a widely accepted valuation tool because it illustrates how much investors are paying for each dollar of earnings. PE ratios help investors quickly gauge if a stock appears cheap or expensive compared to earnings power.

Growth prospects and risk levels are key drivers for what a "normal" or "fair" PE ratio should be. Companies expected to grow earnings rapidly or with more stability often command higher PE multiples, while those facing slower growth or higher risks tend to have lower ones.

Currently, Warner Bros. Discovery is trading at a PE ratio of 116.7x, which stands out against the Entertainment industry average PE of 20x and its peer average of 77.3x. These benchmarks give some context, but by themselves, they do not tell the whole story about what a reasonable multiple should be for this specific company.

This is where Simply Wall St’s proprietary “Fair Ratio” comes in. This metric estimates what the PE ratio should be after considering Warner Bros. Discovery’s profit margins, growth outlook, industry, market cap, and risk factors. It offers a more tailored benchmark than simply comparing the company to its peers or industry average.

The Fair Ratio for Warner Bros. Discovery is 7.0x. Comparing this to the current PE of 116.7x suggests the stock is trading at a significant premium relative to what would be expected by the underlying fundamentals.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1413 companies where insiders are betting big on explosive growth.

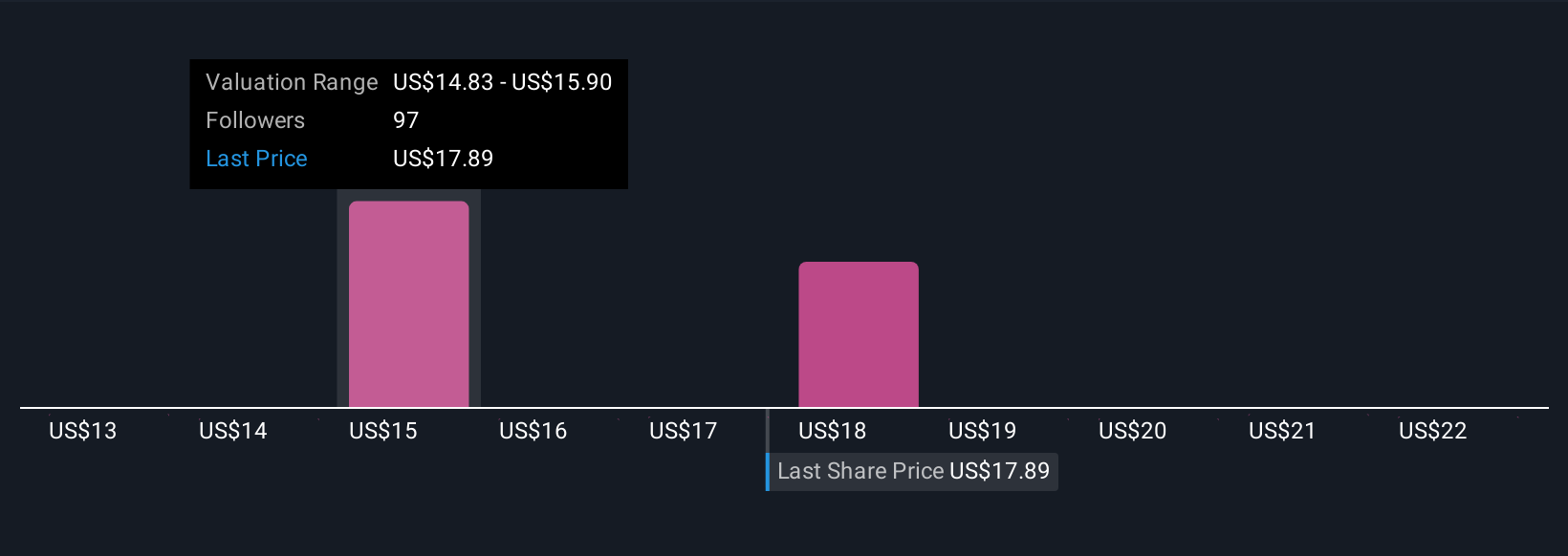

Upgrade Your Decision Making: Choose your Warner Bros. Discovery Narrative

Earlier, we mentioned there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, interactive way to combine your view of a company’s story, its future prospects, challenges, and big bets, with your own expectations for its revenue, margins, and growth. By connecting this story to financial forecasts and a fair value calculation, Narratives help you make smarter, more personal investment decisions.

Available right on the Community page at Simply Wall St, Narratives make it easy for millions of investors to map out why they believe Warner Bros. Discovery is worth more or less than today's market price. Each investor’s Narrative links their perspective to a fair value and allows them to see at a glance whether it's time to buy, hold, or sell, depending on how their fair value compares to the current share price.

Narratives are kept current, automatically updating as new earnings reports or news breaks, so your viewpoint and your estimate of fair value can keep pace with fast-moving market events. For Warner Bros. Discovery, some investors believe in the bullish story that recent merger interest and global expansion could justify a price above $24, while others, focused on ongoing streaming risks, forecast a fair value closer to $10. Narratives empower you to sense-check these perspectives against your own view, creating a smarter approach to investing than relying on ratios alone.

Do you think there's more to the story for Warner Bros. Discovery? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.