Is Waters (WAT) Recent Rally Justified By Conflicting Valuation Signals

Waters WAT | 0.00 |

- Wondering if Waters at around US$371.93 is offering fair value or if the stock is getting ahead of itself? This article walks through what the current price really implies.

- The stock has recently been strong, with returns of 9.8% over the past week and 21.1% over the past month, while the year to date return is a decline of 2.6% and the 1 year return sits at 6.5%.

- That mix of shorter term strength and more modest longer term returns has put the focus back on whether the recent move is backed by fundamentals or mainly by shifting sentiment. This article uses that backdrop as a neutral starting point to reassess what you might reasonably infer from the current share price.

- Simply Wall St's valuation model currently gives Waters a value score of 2 out of 6. Next, you will see how different valuation approaches address that score, and then finish with a broader way to think about valuation beyond any single model.

Waters scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

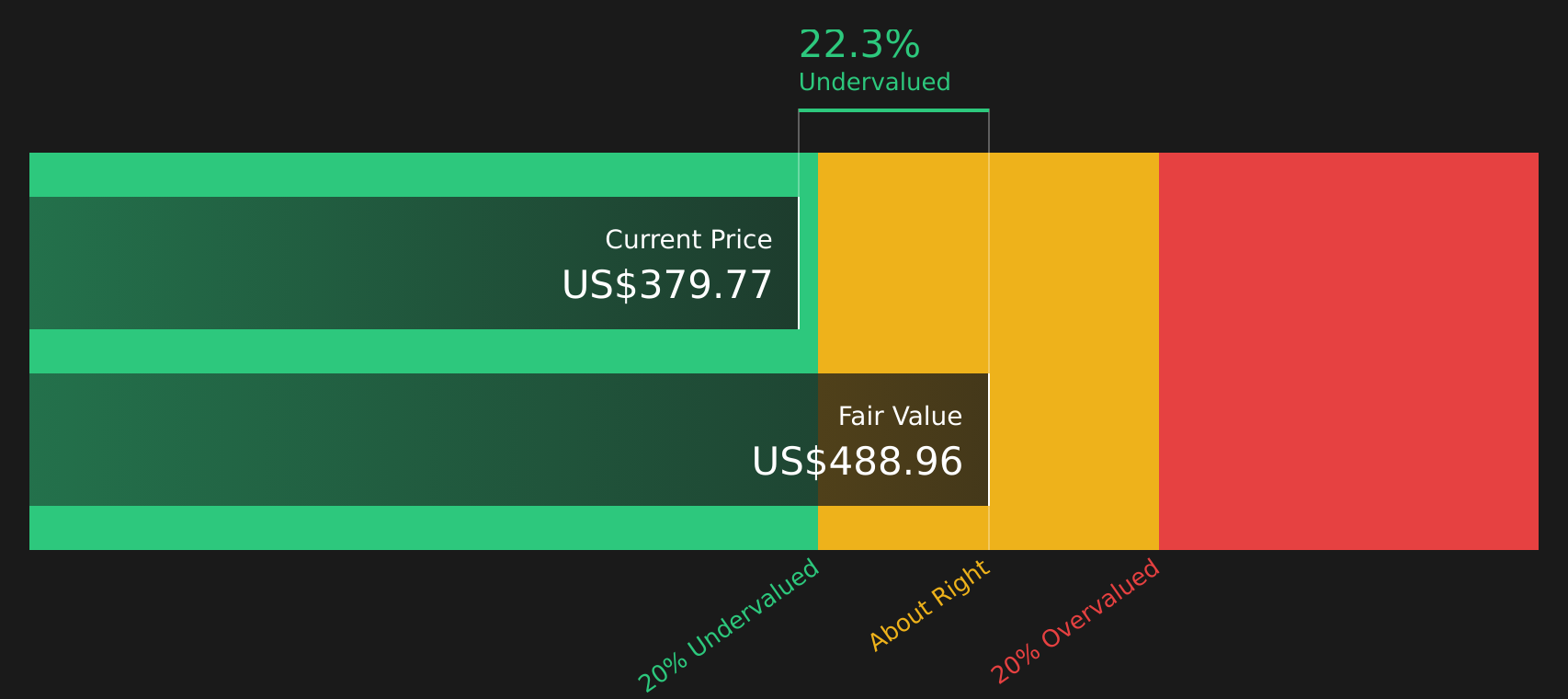

Approach 1: Waters Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows, then discounts them back to today using a required return, to estimate what the entire business might be worth right now.

For Waters, the latest twelve month Free Cash Flow is around $226.1 million. Simply Wall St uses a 2 Stage Free Cash Flow to Equity model that starts with analyst estimates and then extends the projections. For example, projected Free Cash Flow for 2029 is $1.9 billion, with interim years such as 2026 and 2027 estimated at $892.1 million and $1.4 billion respectively, all in $ terms.

When those projected cash flows are discounted and added up, the model arrives at an intrinsic value of about $489.21 per share. Compared with the recent share price of about $371.93, this suggests Waters is trading at roughly a 24.0% discount to that DCF estimate, so the stock appears undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Waters is undervalued by 24.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Waters Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings. This makes it a practical cross check against the DCF result you saw earlier.

What counts as a "normal" P/E depends on what the market expects for future earnings growth and how risky those earnings are perceived to be. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually point to a lower one.

Waters currently trades on a P/E of 81.22x. That sits above the Life Sciences industry average of 35.18x and the peer average of 29.10x, which on simple comparisons suggests the stock carries a richer earnings multiple than many similar companies.

Simply Wall St also calculates a proprietary "Fair Ratio" for the P/E, which for Waters is 30.47x. This metric aims to reflect what P/E might make sense given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it blends these inputs, it can be a more tailored reference point than just lining the stock up against broad industry or peer averages.

Comparing the current P/E of 81.22x with the Fair Ratio of 30.47x indicates the stock is trading above that model based reference point.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Waters Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story about Waters to the numbers you have seen on fair value, future revenue, earnings and margins.

A Narrative is your shorthand story about what you think is happening at the company, which then links directly into a financial forecast and, from there, to an explicit fair value that you can compare with today’s share price.

On Simply Wall St, Narratives sit inside the Community page and are designed so that any investor can select or build a view on Waters without complex modelling, then immediately see how that view translates into projected financials and a value estimate.

For Waters, one Narrative might align with a higher fair value around US$478.22 per share, while another might align with a lower fair value around US$330.00, and you can use that range to judge whether the current price around US$371.93 looks closer to your preferred story or to an alternative view.

Because these Narratives are updated when new earnings, guidance or news arrive, they give you a living framework to revisit whether the gap between your chosen fair value and the market price still supports buying more, holding or reducing exposure.

For Waters however we'll make it really easy for you with previews of two leading Waters Narratives:

Fair value in this bullish narrative: about US$478.22 per share.

Current price vs this fair value implies the stock is trading at roughly a 22.2% discount using ((478.22 - 371.93) / 478.22).

Revenue growth assumption in this view: about 30.1% a year.

- Analysts in this camp see Waters' newer systems and workflow solutions, plus the completed buyback, supporting higher earnings over time.

- They link the updated fair value of about US$478.22 to expectations for rising margins, a future P/E of 52.3x and revenue reaching about US$8.3b by 2029.

- The key watchpoints are technology shifts, pricing pressure, slower software investment and supply chain or regulatory risks that could hold back those expectations.

Fair value in this cautious narrative: about US$330.00 per share.

On this view, the recent price around US$371.93 sits about 12.7% above the narrative fair value using ((371.93 - 330.00) / 330.00).

Revenue growth assumption in this view: about 34.1% a year.

- Analysts here focus on reliance on mature product lines, customer budget pressure and execution risks around acquisitions and reorganization.

- The fair value of about US$330.00 reflects expectations for a future P/E of 35.5x, profit margins around 18.4% and earnings of about US$1.4b by 2029.

- This camp highlights risks from slower recovery in key end markets, integration of BD assets, margin pressure and the possibility that current drivers of recurring revenue may fade.

If you want to go beyond these snapshots and see the full range of community views, including detailed forecasts tied to each storyline, See what the community is saying about Waters.

Do you think there's more to the story for Waters? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.