Is Wayfair’s New Big-Box Store Push and Higher Q2 Outlook Altering The Investment Case For Wayfair (W)?

Wayfair W | 0.00 |

- In recent months, Wayfair has begun opening five new large-format physical stores across the U.S. and raised its Q2 revenue growth guidance to above 5%, marking a move toward a hybrid online-and-offline model.

- This shift suggests Wayfair is looking to use showrooms to improve customer experience, reduce returns, and better compete with omnichannel home-furnishings rivals.

- We’ll now examine how Wayfair’s push into large-format physical stores could reshape its investment narrative and longer-term business profile.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Wayfair Investment Narrative Recap

To own Wayfair, you need to believe its omnichannel pivot, logistics investments, and merchandising efforts can turn persistent losses into a sustainable, asset‑light retail model. The new guidance for Q2 revenue growth above 5% and the accelerated rollout of large stores feed directly into the near term catalyst of improving conversion and unit economics, while also amplifying the key risk that higher fixed costs and advertising might not be offset if home furnishings demand stays uneven.

Among recent announcements, the ongoing buildout of large format stores in markets like New Jersey, New York, and Colorado looks most relevant. These locations tie closely to the earlier halo effect seen around the Chicago area store, and sit at the intersection of several catalysts: tighter integration with the CastleGate logistics network, more effective merchandising via showrooms, and potential uplift in regional sales without abandoning the asset light marketplace model.

Yet, while the store rollout and higher guidance hint at progress, investors should not overlook the risk that structurally thin margins and elevated logistics and advertising costs could still...

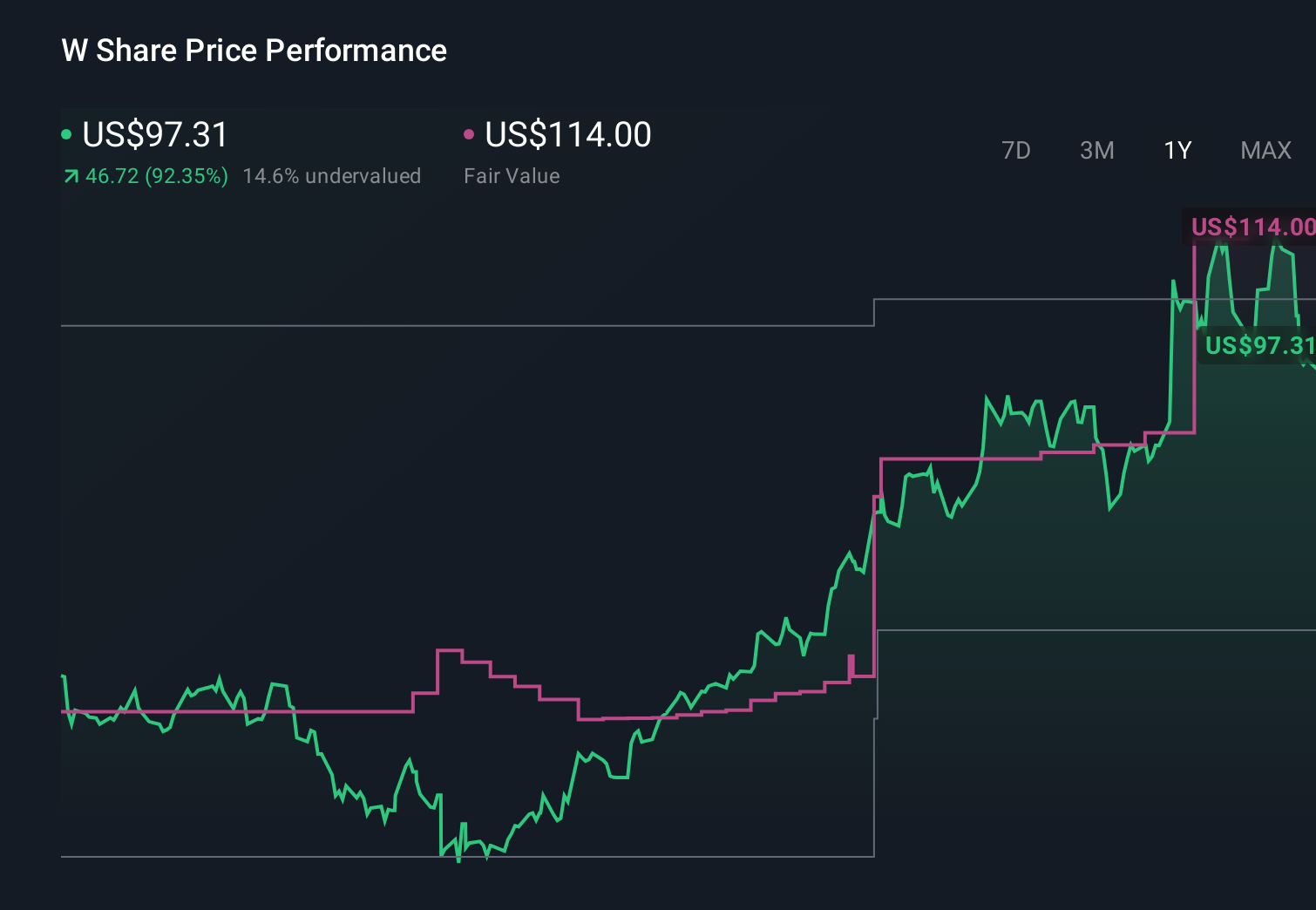

Wayfair's narrative projects $14.9 billion revenue and $382.9 million earnings by 2029.

Uncover how Wayfair's forecasts yield a $91.74 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Wayfair to reach about US$16,000,000,000 in revenue and US$679,000,000 in earnings by 2029, so this latest store news could either reinforce that upbeat view or prompt a rethink, especially if you are weighing it against concerns about thin margins and rising logistics and compliance costs.

Explore 4 other fair value estimates on Wayfair - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.