Is Wayfair's (W) Expanded Affirm Partnership Reframing Its Global Big-Ticket Home Purchase Strategy?

Wayfair, Inc. Class A W | 68.88 | -4.27% |

- On 5 February 2026, Affirm announced it had expanded its partnership with Wayfair to offer transparent, split-payment options to shoppers in the UK and Canada, following an earlier rollout across US online and in-store checkouts.

- This move extends Wayfair’s flexible checkout experience into new international markets, potentially supporting higher conversion on big-ticket home purchases where upfront costs can be a hurdle.

- We’ll now examine how extending Affirm-powered split payments into the UK and Canada could influence Wayfair’s investment narrative and long-term positioning.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Wayfair Investment Narrative Recap

To own Wayfair, you need to believe its investments in logistics, merchandising, and checkout can convert more big-ticket home traffic into profitable orders despite a tough housing backdrop and ongoing losses. The Affirm expansion into the UK and Canada may modestly support near term conversion, but does not change that the key catalyst is improved profitability and cash generation, while the biggest risk remains weak demand for large home purchases and the cost of trying to grow through that softness.

The Affirm rollout lines up with Wayfair’s broader push to improve the buying experience, alongside initiatives like Muse, its visual discovery tool introduced in early 2025. While Muse targets inspiration and personalization on the front end, Affirm’s split-pay options work at checkout, together aiming to lift conversion and order values at a time when management is also focused on cost efficiency and a path toward profitability.

Yet, while this expansion could help, the risk that elevated advertising spend fails to translate into sustained, profitable demand is something investors should be aware of...

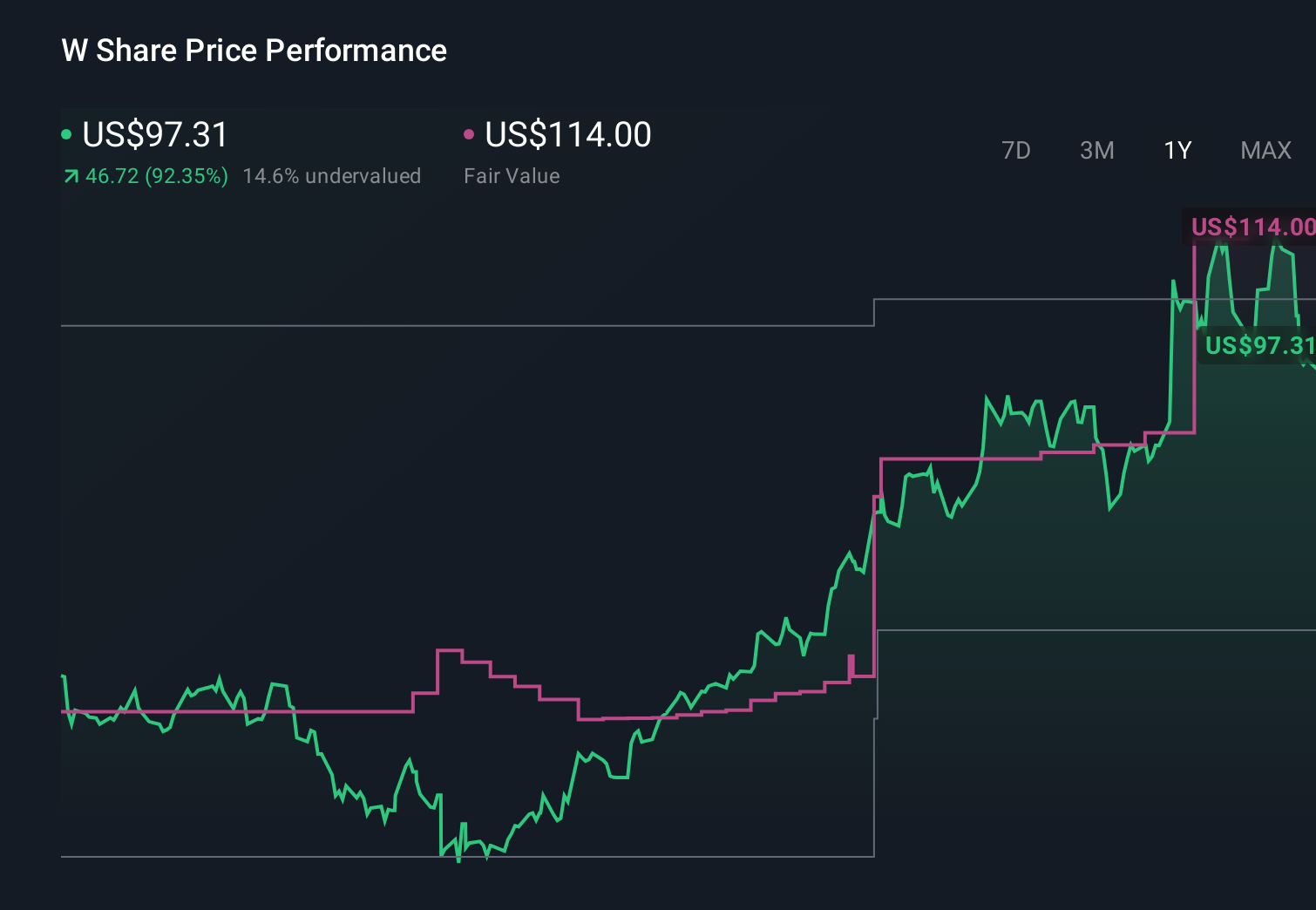

Wayfair's narrative projects $13.9 billion revenue and $124.7 million earnings by 2028. This implies earnings would need to increase by about $124.7 million from roughly breakeven levels today.

Uncover how Wayfair's forecasts yield a $113.64 fair value, a 33% upside to its current price.

Exploring Other Perspectives

While this Affirm news may support conversion, the most pessimistic analysts were assuming only about 3.4% annual revenue growth and no profitability by 2028, so it is worth exploring how views on supply chain costs and long term margin pressure could still diverge from this more optimistic take.

Explore 6 other fair value estimates on Wayfair - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Wayfair research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.