Is Weyerhaeuser Set for Recovery After 21% Stock Drop This Year?

Weyerhaeuser Company WY | 24.43 | +0.62% |

If you are wondering what to make of Weyerhaeuser stock right now, you are definitely not alone. The last few years have been something of a roller coaster for the company’s share price, and lately, it has been particularly interesting for investors keeping an eye on the forest and timberland sector. Over the past year, the stock has dropped 21.2%, and while the year-to-date return is down 10.3%, we have seen a bit of a rebound in the last week with a 1.0% increase which might hint that sentiment is shifting or that investors are reassessing risk here. The bigger picture is that over the last five years, Weyerhaeuser shares are still in positive territory, but with only a 3.1% gain, the journey has certainly tested patience.

So, what does this all mean if you are trying to figure out whether now’s the time to buy, hold, or move on? The answer, as always, comes down to value and what you are really getting for your money at today’s price of $25.12 per share. According to our most recent analysis, Weyerhaeuser scores a 3 on the valuation checklist, meaning it is considered undervalued in three out of six of the standard checks we use. That is a solid starting point, but it is only part of the story.

Stick with me as we break down exactly how the company stacks up using these different valuation methods, and I will also share one approach at the end that often cuts through the noise better than the rest.

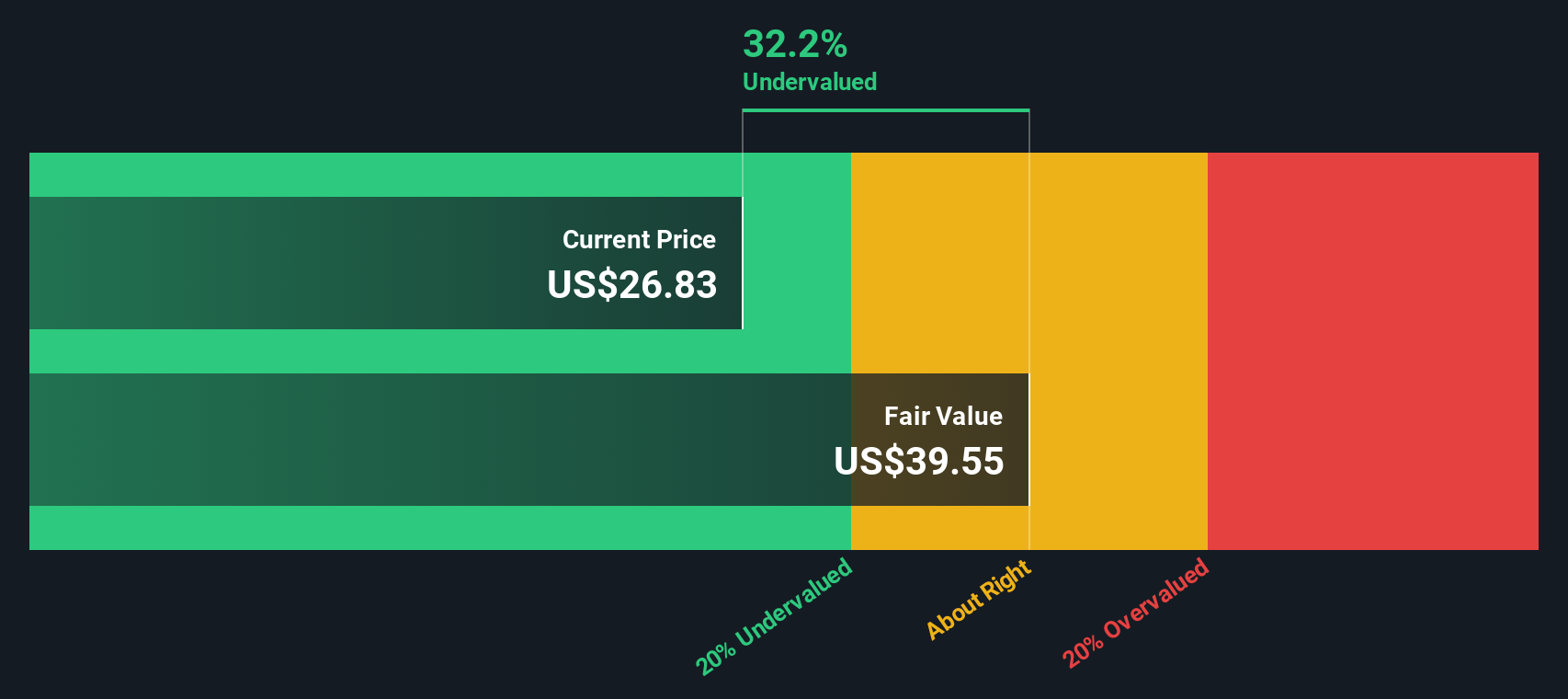

Approach 1: Weyerhaeuser Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a company is worth by projecting its future cash flows. Here, the model uses adjusted funds from operations and discounts them back to today's value. This method aims to answer the question: what are future dollars from Weyerhaeuser’s business actually worth right now?

For Weyerhaeuser, analysts forecast cash flows several years ahead, specifically projecting $1,093 Million in free cash flow for 2029. Beyond analyst estimates, longer-term figures are extrapolated and ultimately suggest steady growth, with projected free cash flows reaching as high as $1.69 Billion by 2035. All dollar figures are in USD.

Plugging these projections into the DCF model produces an intrinsic value for Weyerhaeuser of $39.65 per share. With the recent share price at $25.12, this methodology points to a discount of 36.6%. In simple terms, this suggests the stock is significantly undervalued compared to what the underlying business is forecast to generate in the years ahead.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Weyerhaeuser is undervalued by 36.6%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

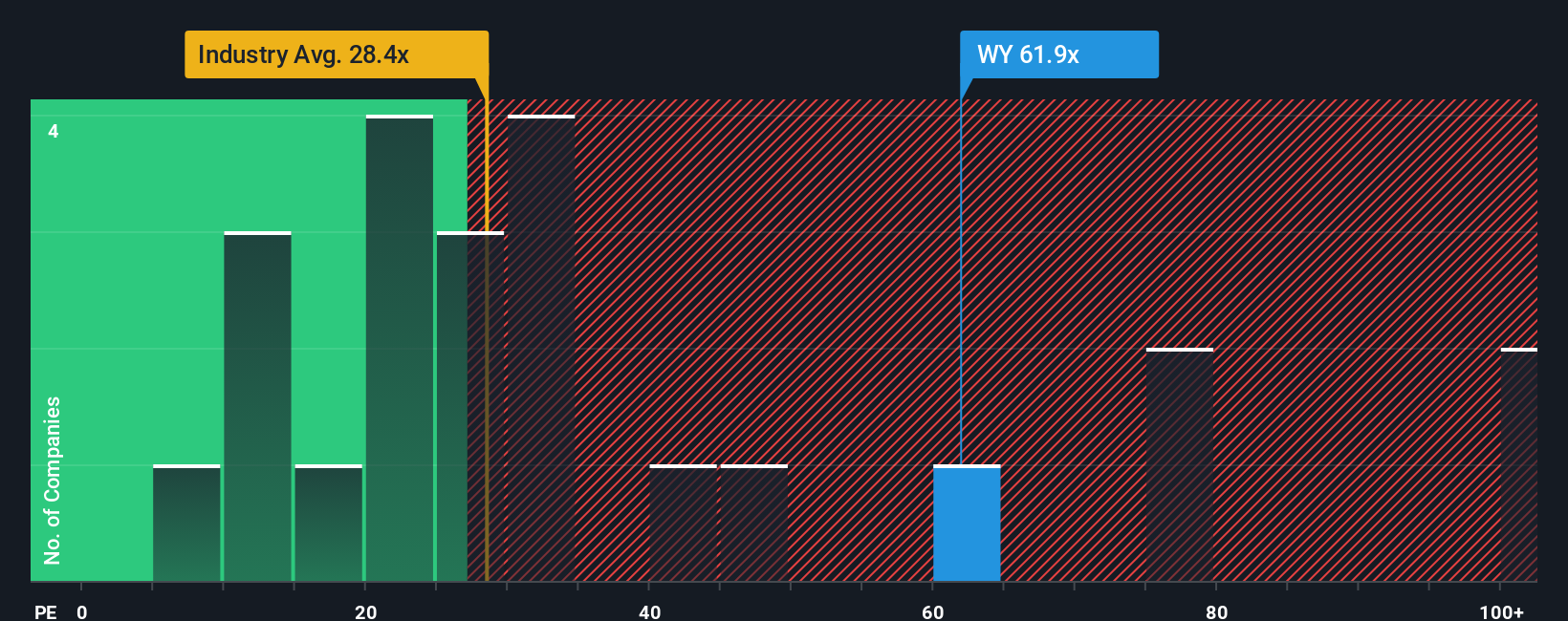

Approach 2: Weyerhaeuser Price vs Earnings

The price-to-earnings (PE) ratio is an especially useful tool for valuing established, profitable companies like Weyerhaeuser. It gives investors a simple way to judge how much they are paying for each dollar of current earnings. A "normal" or "fair" PE ratio is influenced by several factors, including a company’s growth prospects, stability, and the risks in its underlying business. Generally, companies with higher growth or lower risk can justify higher PE ratios, while those with more uncertainty tend to trade at lower multiples.

Weyerhaeuser currently trades at a PE ratio of 65x. That is noticeably higher than the broader Specialized REITs industry average of 17.8x, and also above the peer average of 33x. However, simply comparing to these benchmarks does not always tell the full story, since they do not factor in the unique aspects of Weyerhaeuser’s business.

This is where Simply Wall St’s proprietary “Fair Ratio” comes in. The Fair Ratio, which is 51.99x in this case, is specifically calculated using Weyerhaeuser’s own earnings growth outlook, risk profile, margin, industry landscape, and market cap. It is a more tailored benchmark that aims to cut through the noise of typical peer and industry comparisons.

Comparing Weyerhaeuser’s actual PE of 65x to its Fair Ratio of 52x, the stock appears to be pricing in more optimism than is warranted by its fundamentals. Since the difference between the ratios is greater than 0.10, this suggests Weyerhaeuser is trading above what would be justified by its risk and growth profile.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Weyerhaeuser Narrative

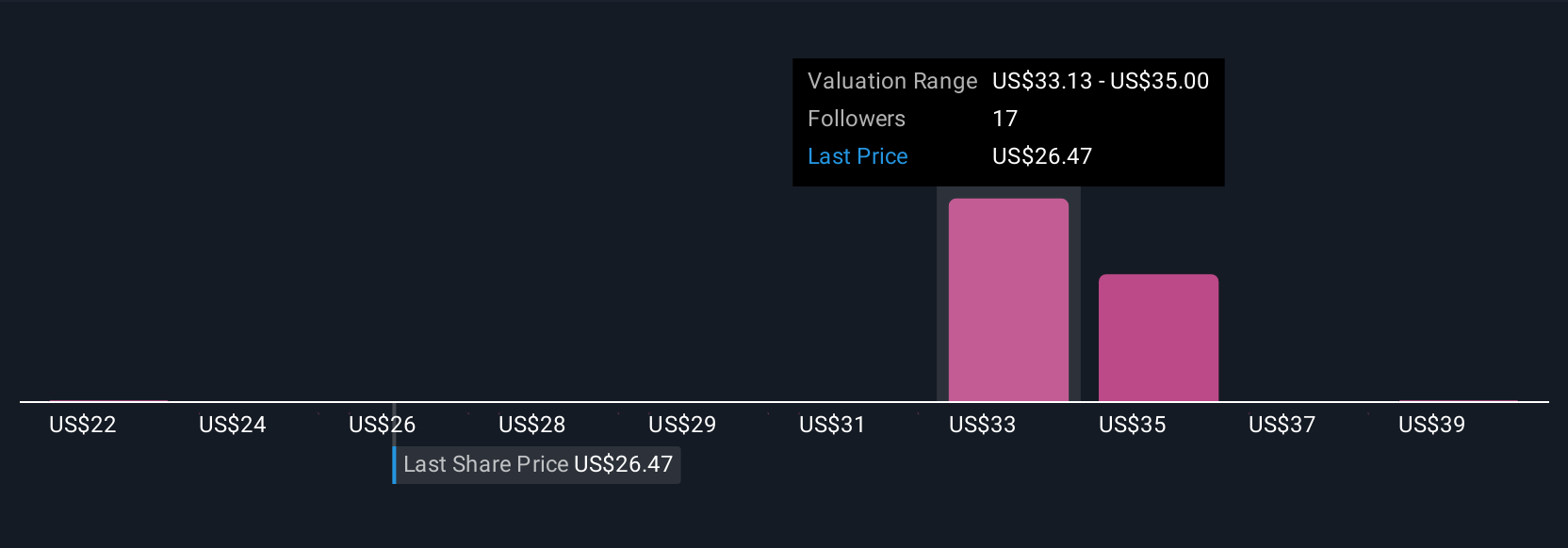

Earlier, we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is simply your story about a company where you connect your perspective, such as assumptions about future revenue, earnings, and margins, with what you believe is a fair value for the stock.

Unlike traditional models that rely strictly on historical numbers, Narratives let you tie your reasoning and expectations directly to the forecasted financials and valuation, giving real meaning to the numbers. This way, you can easily see how your belief about a company’s future shapes its estimated worth today.

Narratives are available right within the Community page on Simply Wall St, making it easy and approachable for any investor to craft and compare their own investment story. Millions of users use Narratives every day to help decide whether to buy, hold, or sell a stock, with the decision coming down to whether the Fair Value you believe in happens to be above or below the current market price.

What makes Narratives powerful is their ability to stay up-to-date. As soon as there is new news or a company posts fresh results, key forecasts and fair values are automatically updated, so no manual number crunching is needed. For example, some investors think Weyerhaeuser could be worth as much as $38.00 per share if margins and exports improve, while others forecast just $29.00 if global trade disruptions persist.

Do you think there's more to the story for Weyerhaeuser? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.