Jabil (JBL) Valuation Check As EHT Semi Partnership Expands Advanced Semiconductor Ambitions

Jabil Inc. JBL | 268.55 | -1.25% |

Why Jabil’s EHT Semi deal matters for the stock

Jabil (JBL) has drawn fresh attention after announcing a minority investment and manufacturing partnership with Eagle Harbor Technologies, tying its large scale production capabilities to EHT Semi's power delivery systems for advanced semiconductor fabrication.

For you as a shareholder or potential investor, this move sits alongside Jabil's existing semiconductor focused work and is part of a broader story about how the company positions itself in a sector many see as increasingly important to computing, data centers and electronics supply chains.

Jabil's EHT Semi announcement lands during a brief pause in the share price, with a 1 day share price return of a 3.34% decline and a 7 day share price return of a 3.35% decline, even though the 90 day share price return of 15.19% and a 1 year total shareholder return of 43.14% point to momentum that has been strong over a longer stretch. Recent board changes, a fresh quarterly dividend declaration and new bond issuance sit in the background as the shares trade at US$244.70.

If you are tracking how semiconductor related names are moving, it can be useful context to scan high growth tech and AI stocks as a way of spotting other potential ideas in the same broad theme.

With Jabil delivering a 1 year total shareholder return of 43.14% and trading at US$244.70 with an estimated 31% intrinsic discount, investors may wonder whether there is still potential upside or if the market is already pricing in future growth.

Most Popular Narrative: 5.6% Undervalued

Against Jabil's last close of $244.70, the most followed narrative points to a fair value of $259.25, suggesting modest undervaluation on a discounted cash flow view.

The anticipated $1.2 billion in free cash flow generation suggests sound financial health, providing flexibility for share buybacks or strategic investments that could support earnings per share growth.

Curious what kind of revenue path, margin shift, and earnings multiple are baked into that valuation story? The narrative leans on detailed projections that go well beyond simple P/E snapshots.

Result: Fair Value of $259.25 (UNDERVALUED)

However, there are still pressure points to watch, including revenue declines in Regulated Industries and Connected Living, as well as tariff uncertainty that could challenge those upbeat assumptions.

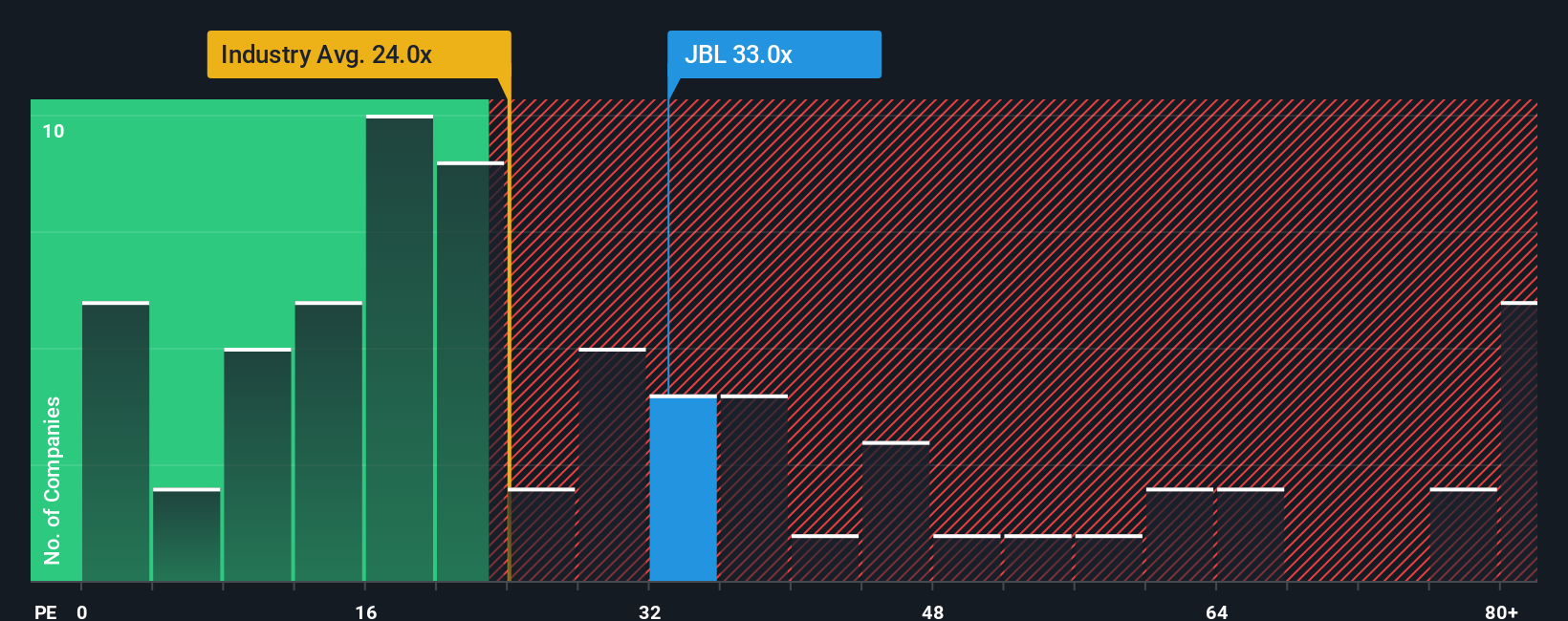

Another View: Pricing Signals From P/E Ratios

While our narrative points to Jabil as undervalued on cash flow assumptions, the market’s current P/E of 36.8x tells a different story. That is higher than the US Electronic industry at 28.1x and also above a fair ratio estimate of 32.2x, which suggests valuation risk if expectations cool.

Compared with immediate peers, Jabil’s P/E sits just under the 37x peer average. The shares are not an obvious outlier, but they are far from cheap. For you, the question is whether earnings can grow into this multiple or if the market is paying up too much for the story right now.

Build Your Own Jabil Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own view against the data, you can build a custom narrative in just a few minutes using Do it your way.

A great starting point for your Jabil research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If you stop at a single stock, you could miss other opportunities sitting in plain sight, so put the Simply Wall Street Screener to work for you today.

- Target dependable income by scanning these 12 dividend stocks with yields > 3% that offer higher yields while still passing key fundamental checks.

- Spot potential growth stories early by checking these 3522 penny stocks with strong financials that already show stronger balance sheets and financial quality.

- Zero in on value focused opportunities using these 880 undervalued stocks based on cash flows that trade below what their cash flows suggest they might be worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.