January 2026 Penny Stocks To Watch For Potential Growth

VTEX Class A VTEX | 0.00 |

As of late January 2026, the U.S. stock market remains relatively stable with major indices showing little change following the Federal Reserve's decision to maintain current interest rates. This steady environment provides an interesting backdrop for investors considering penny stocks, a term that may seem outdated but still represents a viable investment area in smaller or newer companies. By focusing on those with strong financial health and clear growth potential, investors can uncover opportunities for significant returns within this niche market segment.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Rewards & Risks |

| Dingdong (Cayman) (DDL) | $2.82 | $612.91M | ✅ 3 ⚠️ 1 View Analysis > |

| Waterdrop (WDH) | $1.71 | $603.98M | ✅ 4 ⚠️ 0 View Analysis > |

| WM Technology (MAPS) | $0.8103 | $137.38M | ✅ 4 ⚠️ 1 View Analysis > |

| LexinFintech Holdings (LX) | $2.90 | $496.38M | ✅ 4 ⚠️ 1 View Analysis > |

| Tuya (TUYA) | $2.15 | $1.31B | ✅ 4 ⚠️ 1 View Analysis > |

| Perfect (PERF) | $1.66 | $170.09M | ✅ 5 ⚠️ 0 View Analysis > |

| Golden Growers Cooperative (GGRO.U) | $5.00 | $77.45M | ✅ 2 ⚠️ 5 View Analysis > |

| Cricut (CRCT) | $4.44 | $931.68M | ✅ 2 ⚠️ 2 View Analysis > |

| BAB (BABB) | $0.93 | $6.76M | ✅ 2 ⚠️ 3 View Analysis > |

| Lifetime Brands (LCUT) | $3.61 | $84.96M | ✅ 3 ⚠️ 2 View Analysis > |

Let's take a closer look at a couple of our picks from the screened companies.

Cricut (CRCT)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Cricut, Inc. designs, markets, and distributes a creativity platform for crafting handmade goods across various regions worldwide with a market cap of approximately $931.68 million.

Operations: The company's revenue is derived from its platform segment, which generated $322.83 million.

Market Cap: $931.68M

Cricut, Inc. demonstrates financial stability with no debt and strong short-term asset coverage of both long-term and short-term liabilities. Recent earnings growth of 30% surpasses its five-year average decline, indicating a positive shift in profitability, further supported by improved net profit margins from 8.5% to 11.3%. Despite this progress, the company's dividend sustainability is questionable due to inadequate free cash flow coverage. Cricut's experienced management and board teams contribute to its operational resilience, while recent share buybacks and a declared dividend reflect shareholder-focused initiatives amidst stable market volatility.

EVgo (EVGO)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: EVgo, Inc. owns and operates a direct current fast charging network for electric vehicles in the United States with a market cap of approximately $939.35 million.

Operations: The company's revenue segment includes Retail - Gasoline & Auto Dealers, generating $333.13 million.

Market Cap: $939.35M

EVgo, Inc. is focusing on expanding its fast charging network with plans to install over 500 NACS connectors by year-end 2026 and collaborate with Kroger to build at least 150 stalls annually through 2035. Despite having a market cap of approximately US$939.35 million, the company remains unprofitable, with losses growing at a significant rate over the past five years. While EVgo's short-term assets exceed its short-term liabilities, they fall short of covering long-term obligations. The recent appointment of a seasoned CFO aims to support strategic financial growth amidst these challenges and opportunities in the EV sector.

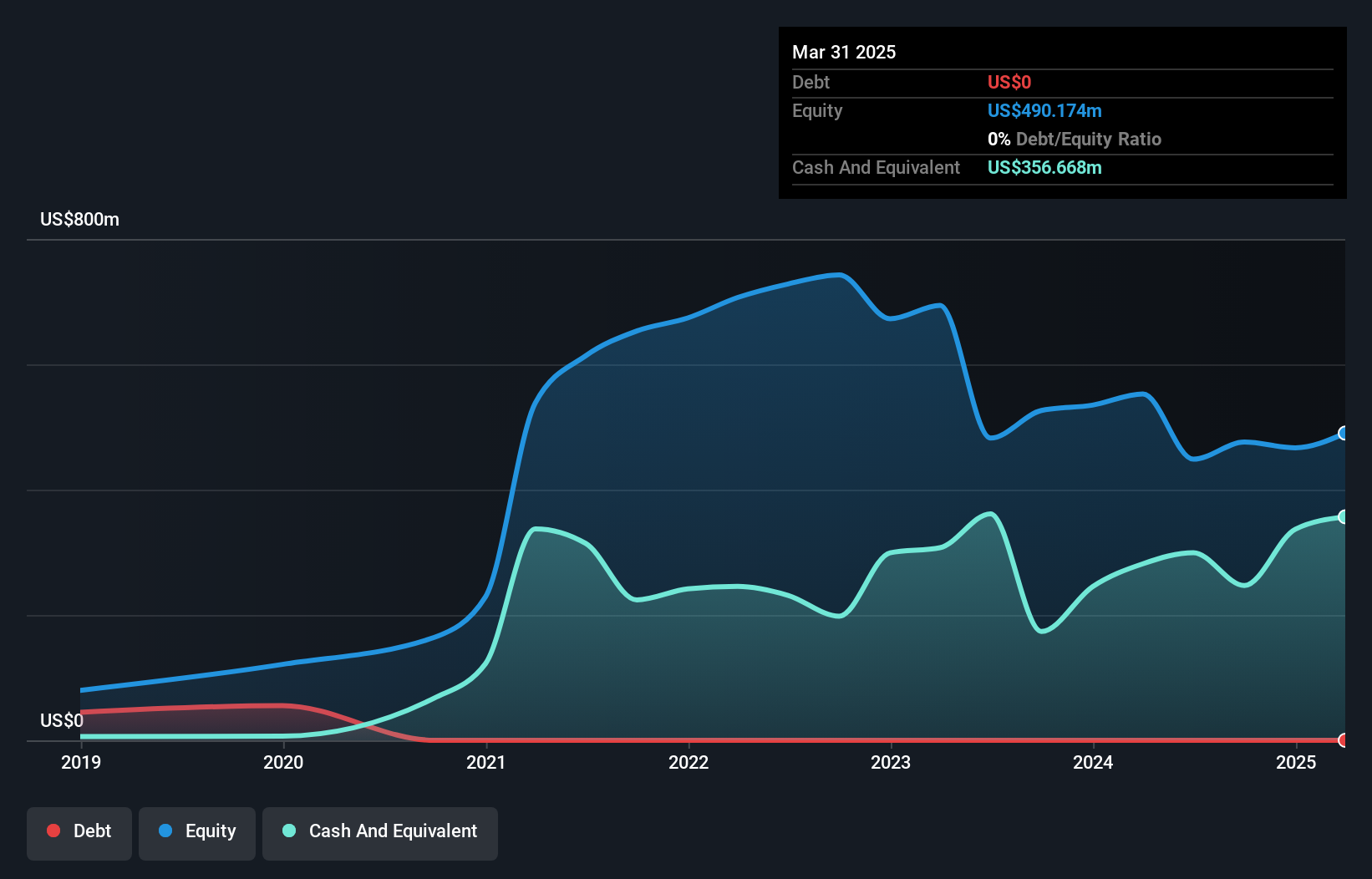

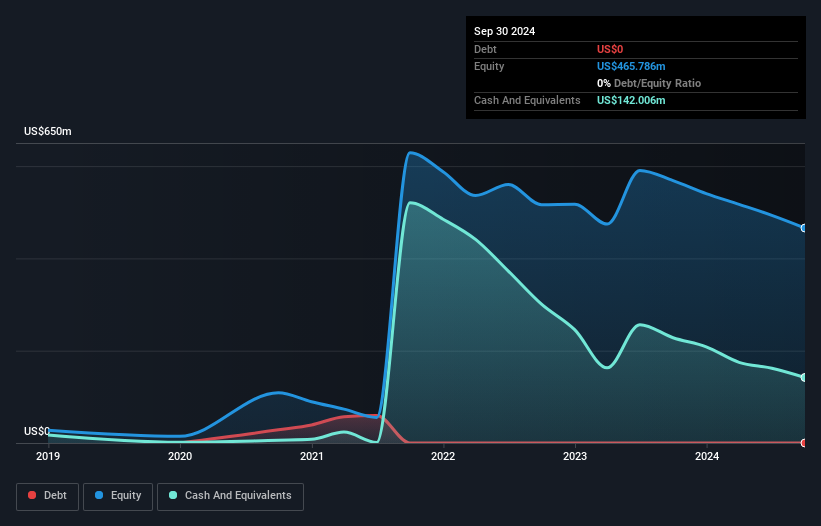

VTEX (VTEX)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: VTEX, along with its subsidiaries, offers a software-as-a-service digital commerce platform for enterprise brands and retailers, with a market cap of $600.58 million.

Operations: The company generates revenue of $234.12 million from its Internet Software & Services segment.

Market Cap: $600.58M

VTEX, with a market cap of US$600.58 million, has shown consistent revenue growth, reporting US$59.61 million for Q3 2025 and US$172.56 million for the first nine months of 2025. The company is debt-free and its short-term assets exceed both short- and long-term liabilities, indicating strong financial health. Although recent earnings growth slowed to 6.6%, VTEX remains profitable with improved net profit margins from last year. The company completed a share buyback program worth US$27.59 million, reflecting confidence in its valuation while providing guidance for continued subscription revenue growth into Q4 2025 and beyond.

Seize The Opportunity

- Reveal the 330 hidden gems among our US Penny Stocks screener with a single click here.

- Want To Explore Some Alternatives? Uncover 14 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.