JetBlue Airways (JBLU) Could Be 14% Overvalued On Mint Expansion News

JetBlue Airways Corporation JBLU | 0.00 |

JetBlue Airways (JBLU) is back in focus after announcing a larger Mint footprint from Fort Lauderdale, including new premium service to San Diego and more Mint frequencies to Los Angeles and San Francisco starting this winter.

These Mint upgrades arrive as JetBlue Airways trades at US$5.63, with the stock showing a 27.38% 90 day share price return and a 33.10% 1 year total shareholder return. However, the 3 year and 5 year total shareholder returns remain significantly negative, suggesting more recent momentum contrasts with a weaker longer term record.

If this premium travel push has you rethinking where growth might emerge next, it could be worth scanning other opportunities through our screener of 20 top founder-led companies

So with JetBlue Airways stock at US$5.63, a recent 1 year total shareholder return of 33.10% but a weaker 3 and 5 year record, are you looking at an undervalued recovery story or a price that already reflects future growth?

Most Popular Narrative: 13.8% Overvalued

On the most followed narrative, JetBlue Airways screens as overvalued, with a fair value of $4.95 against the latest close at $5.63, which frames the Mint expansion against a richer valuation backdrop.

The rebound in leisure travel and resilient demand, especially among Millennials and Gen Z prioritizing experiences, continues to drive close-in bookings and support premium cabin and loyalty revenue growth, which is likely to result in higher ticket revenues and topline expansion.

This fair value hinges on a specific playbook: revenue climbing at a steady clip, margins moving from losses toward typical airline levels, and a future earnings multiple that sits well below many peers.

Result: Fair Value of $4.95 (OVERVALUED)

However, this JetBlue Airways story can shift quickly if fuel costs climb further or if competitive pressure keeps load factors and unit revenues under strain.

Another View on JetBlue Airways Valuation

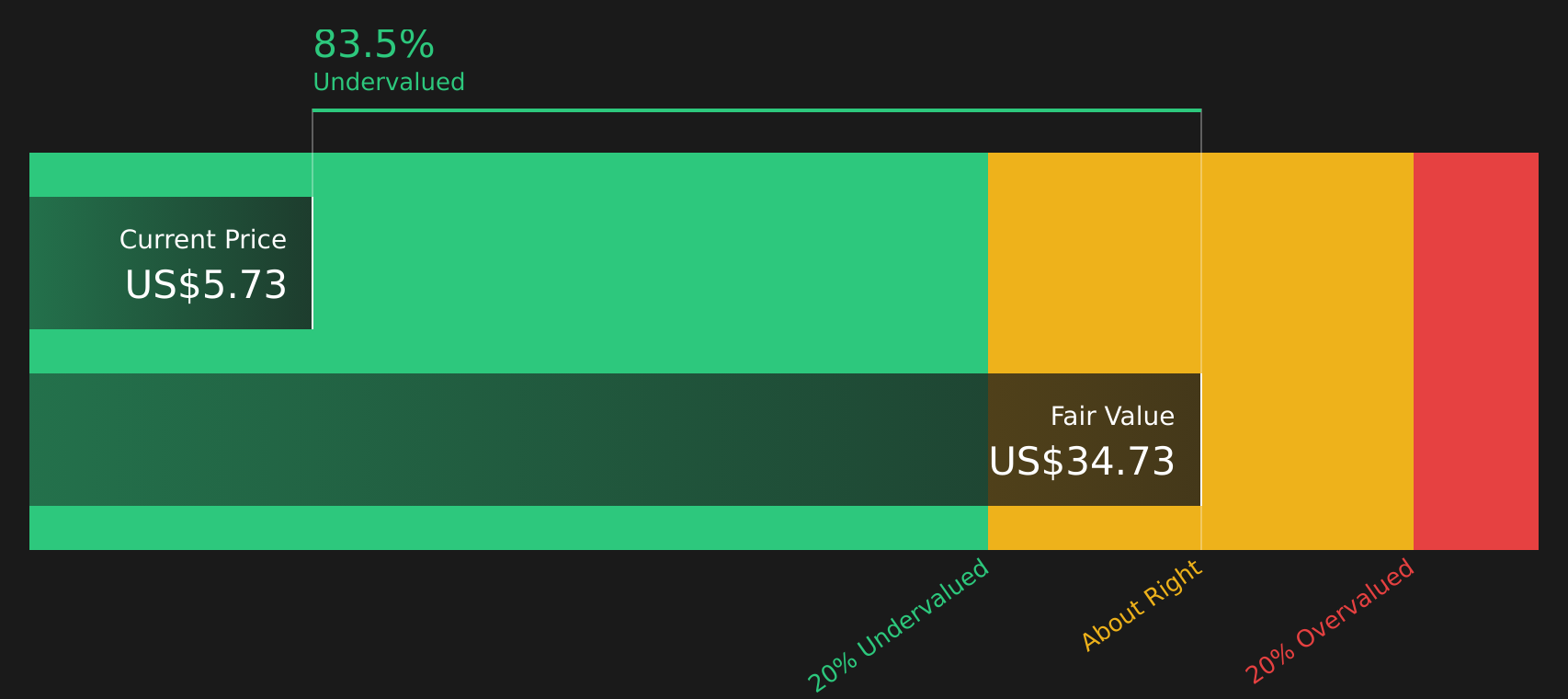

That 13.8% overvaluation signal from the consensus fair value of $4.95 sits awkwardly next to another data point: our SWS DCF model, which suggests JetBlue Airways might be trading about 83.8% below its own future cash flow value at $34.73. Is the crowd underestimating the long term cash story?

Next Steps

Mixed signals on JetBlue Airways so far? Take a closer look at the numbers, weigh both the concerns and the upside, and then review the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond JetBlue Airways?

If JetBlue Airways has you thinking differently about where your next opportunity might come from, do not stop here. Broaden your watchlist before the market moves on.

- Spot potential mispricing early by scanning companies that currently screen as 42 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses highlighted in our 72 resilient stocks with low risk scores.

- Hunt for tomorrow's potential standouts with the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.