JetBlue Airways (JBLU) Stock Could Be 15% Overvalued After Mint Expansion In South Florida

JetBlue Airways Corporation JBLU | 0.00 |

JetBlue Airways (JBLU) is reshaping its network around South Florida by expanding Mint business class service from Fort Lauderdale to San Diego, Los Angeles and San Francisco, while closing crew and tech bases in Newark and LaGuardia.

Recent news around JetBlue Airways sharpening its focus on South Florida coincides with strong price momentum, with a 1 day share price return of 10.72%, a 90 day share price return of 35.24% and a 1 year total shareholder return of 41.65%, although the 5 year total shareholder return is down 66.94%.

If JetBlue’s refocus on premium routes has your attention, it can be a good moment to see what else is moving in travel related infrastructure and 34 power grid technology and infrastructure stocks

So with JetBlue Airways stock climbing recently but still carrying a very large modeled intrinsic discount and trading below the average analyst price target, is the market overlooking value here, or already pricing in future growth?

Most Popular Narrative: 15% Overvalued

JetBlue Airways last closed at $5.68, compared with a widely followed fair value narrative of $4.95 that is based on detailed revenue and margin assumptions.

The rebound in leisure travel and resilient demand, especially among Millennials and Gen Z prioritizing experiences, continues to drive close-in bookings and support premium cabin and loyalty revenue growth, which is likely to result in higher ticket revenues and topline expansion.

Read the complete narrative. Read the complete narrative.

The fair value model leans heavily on stronger ticket yields, improving margins and a reset earnings base. It may be useful to explore which revenue and profit assumptions have the most impact here.

Result: Fair Value of $4.95 (OVERVALUED)

However, JetBlue Airways still faces key pressures, including exposure to jet fuel price swings and rising labor costs, either of which could quickly squeeze already thin margins.

Another View: JetBlue Airways Through A Sales Multiple Lens

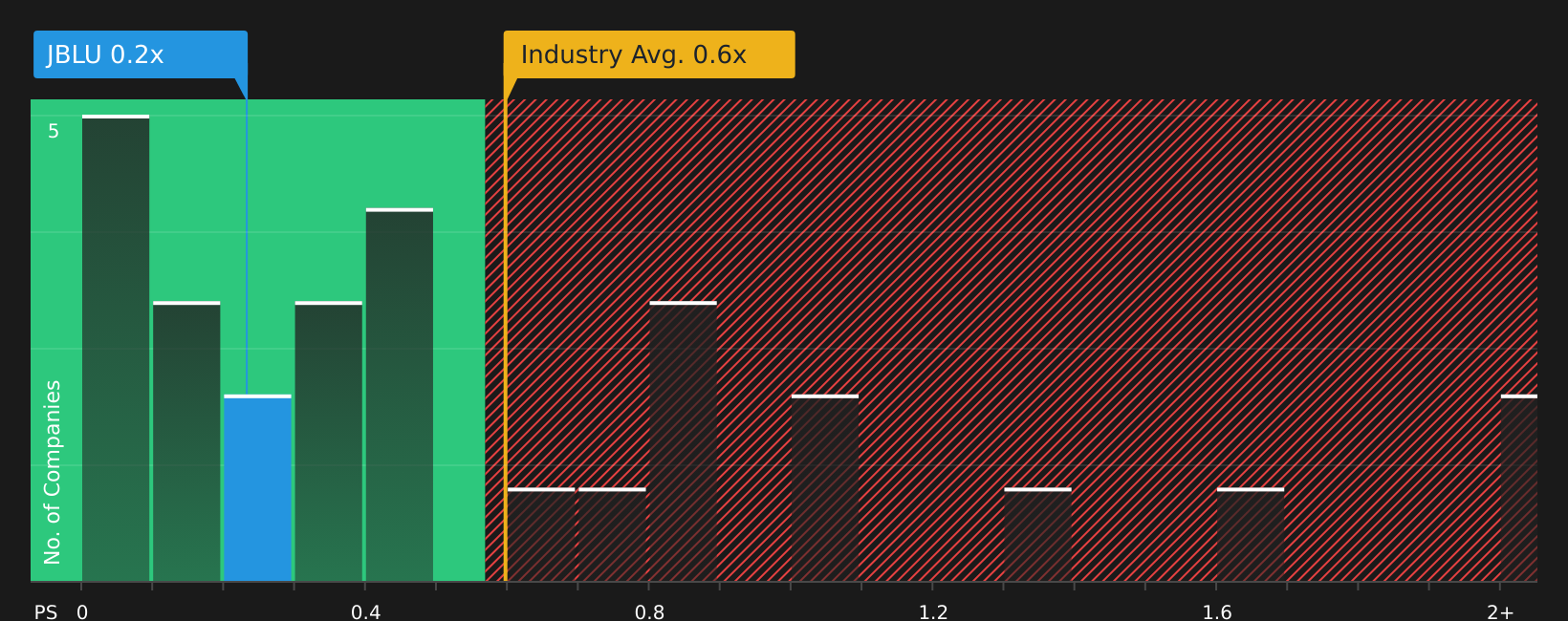

While the popular narrative pegs JetBlue Airways as about 15% overvalued at a fair value of $4.95, the picture shifts when you look at its P/S ratio. At roughly 0.2x sales, compared with about 0.7x for peers and a fair ratio of 0.8x, the stock screens as cheap on revenues alone. If the market ever moves that gap closer to the fair ratio, how much of today’s discount would really remain?

For a closer look at how this sales based view stacks up against earnings expectations and other checks, see what the numbers say in our valuation breakdown: See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With JetBlue Airways drawing mixed reactions from investors, it is worth taking a closer look at the underlying data and sentiment across both risks and rewards, then quickly weighing that against your own expectations by reviewing the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond JetBlue Airways?

If JetBlue Airways has sharpened your interest in airline and travel opportunities, do not stop there. Broaden your watchlist with other focused ideas that could complement your portfolio.

- Target potential mispricings by scanning 45 high quality undervalued stocks that combine solid fundamentals with compressed valuations.

- Strengthen your income stream by reviewing 8 dividend fortresses built around higher yielding companies.

- Prioritize capital preservation by assessing 65 resilient stocks with low risk scores that score well on financial resilience and volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.