JetBlue (JBLU) Stock Valuation Check After Recent Rebound And Mixed Long Term Returns

JetBlue Airways Corporation JBLU | 0.00 |

JetBlue Airways stock: recent performance snapshot

JetBlue Airways (JBLU) has recently drawn investor attention after a period of mixed financial metrics and stock returns, with the shares moving over the past month and past 3 months on shifting expectations.

Over the past month, the stock shows a 9.39% gain, with a 17.61% rise over the past 3 months and a 12.08% total return over the past year. These moves sit alongside a weaker 3 year and 5 year record, where total returns declined 37.84% and 71.06% respectively.

Recent trading has been firm, with a 90 day share price return of 17.61% and a 1 year total shareholder return of 12.08%. However, longer term total returns remain sharply negative. This suggests confidence is rebuilding after a tougher few years as investors reassess both growth potential and risk.

If JetBlue has you looking at opportunities across transportation and infrastructure, it can be useful to see what is moving in related areas like automation and logistics. Take the next step and scan 33 robotics and automation stocks

With JetBlue stock trading near analyst targets, yet sitting on a large modeled intrinsic discount and a history of weak multi-year returns, is the market missing a recovery story or already pricing in all the future growth?

Most Popular Narrative: 1% Overvalued

JetBlue's most followed valuation narrative pegs fair value at about $4.95 per share, slightly below the recent $5.01 close. This puts the current price just above that modeled estimate while still reflecting a large intrinsic discount from the SWS DCF work.

The Blue Sky partnership with United, expanded distribution/loyalty integration, and growth of the capital-light, high-margin Paisly travel products business will open new revenue streams, improve customer retention, and contribute at least $50M in incremental EBIT by 2027, accelerating EBITDA and earnings growth.

Want to see what this narrative is really banking on? It leans heavily on steady revenue expansion, a margin rebuild, and a future earnings multiple that sits well below the sector. The tension lies in how those pieces fit together over time.

Result: Fair Value of $4.95 (OVERVALUED)

However, this depends on close-in bookings remaining strong and on fuel costs not rising further, as either factor could quickly pressure margins and earnings visibility.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

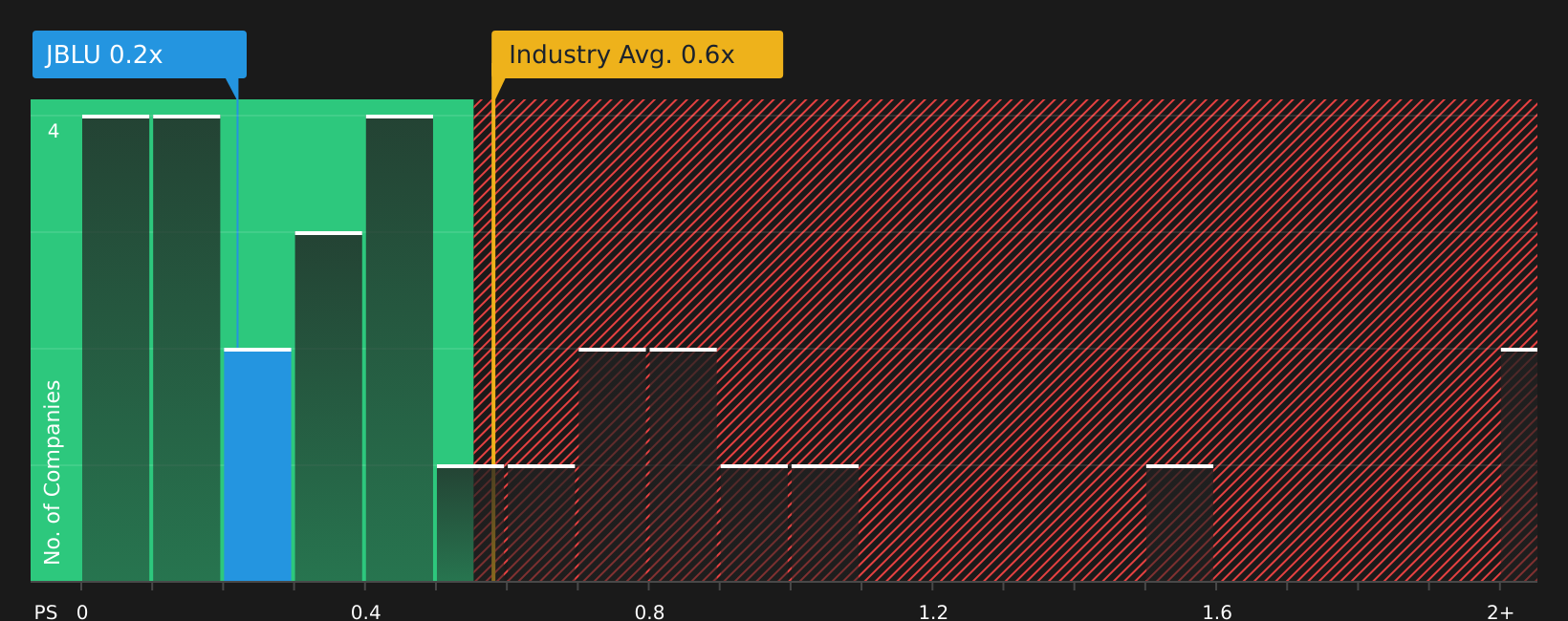

Another way to look at JetBlue's value

The analyst narrative leans on future earnings power, but current trading tells a different story. JetBlue changes hands at a P/S ratio of 0.2x, compared with 0.6x for both peers and the wider global airlines group, while the fair ratio sits at 0.7x. That is a wide gap, and it raises the question of whether the market is pricing in too much earnings risk or offering a potential reset point for patient investors.

Next Steps

Mixed signals on value and sentiment so far? Use the latest data to form your own view, starting with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

Do not stop at one stock when a broader watchlist can reveal better fits for your goals. Use the screeners below to uncover ideas you might otherwise overlook.

- Hunt for potential mispriced opportunities by scanning 44 high quality undervalued stocks that pair quality fundamentals with appealing valuations.

- Target steadier capital preservation by reviewing 71 resilient stocks with low risk scores designed for investors who want resilience front and center.

- Spot earlier stage opportunities with room to grow by checking the screener containing 20 high quality undiscovered gems before they gain wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.