Jones Lang LaSalle (JLL): Valuation Insights Following Strong Q2 Results, New UK Leadership, and $1.1B Deal

Jones Lang LaSalle Incorporated JLL | 308.52 | +1.38% |

Jones Lang LaSalle (JLL) has investors buzzing after releasing second-quarter 2025 results that topped expectations, coupled with some bold moves on the leadership and dealmaking fronts. Not only did the company surpass earnings forecasts, but recent headlines have included a $1.1 billion multi-housing transaction and a series of leadership appointments aimed at fortifying its regional presence in the UK. These coordinated efforts appear tailored to assure shareholders that JLL’s mix of operational execution and long-term planning is functioning effectively.

That confidence has shown up in the stock price. JLL reached an all-time high of $316.89 following these developments, and momentum has steadily built throughout the year. The stock is up over 21% year-to-date and is showing especially strong returns over the past month and quarter, suggesting that the market is increasingly optimistic about the company’s growth strategy. Leadership changes and headline-grabbing deals have also contributed to the sense that JLL is actively shaping its next chapter rather than relying on past successes.

So where does all this momentum leave investors now? Is Jones Lang LaSalle undervalued at these levels, or has the market already priced in its next wave of growth?

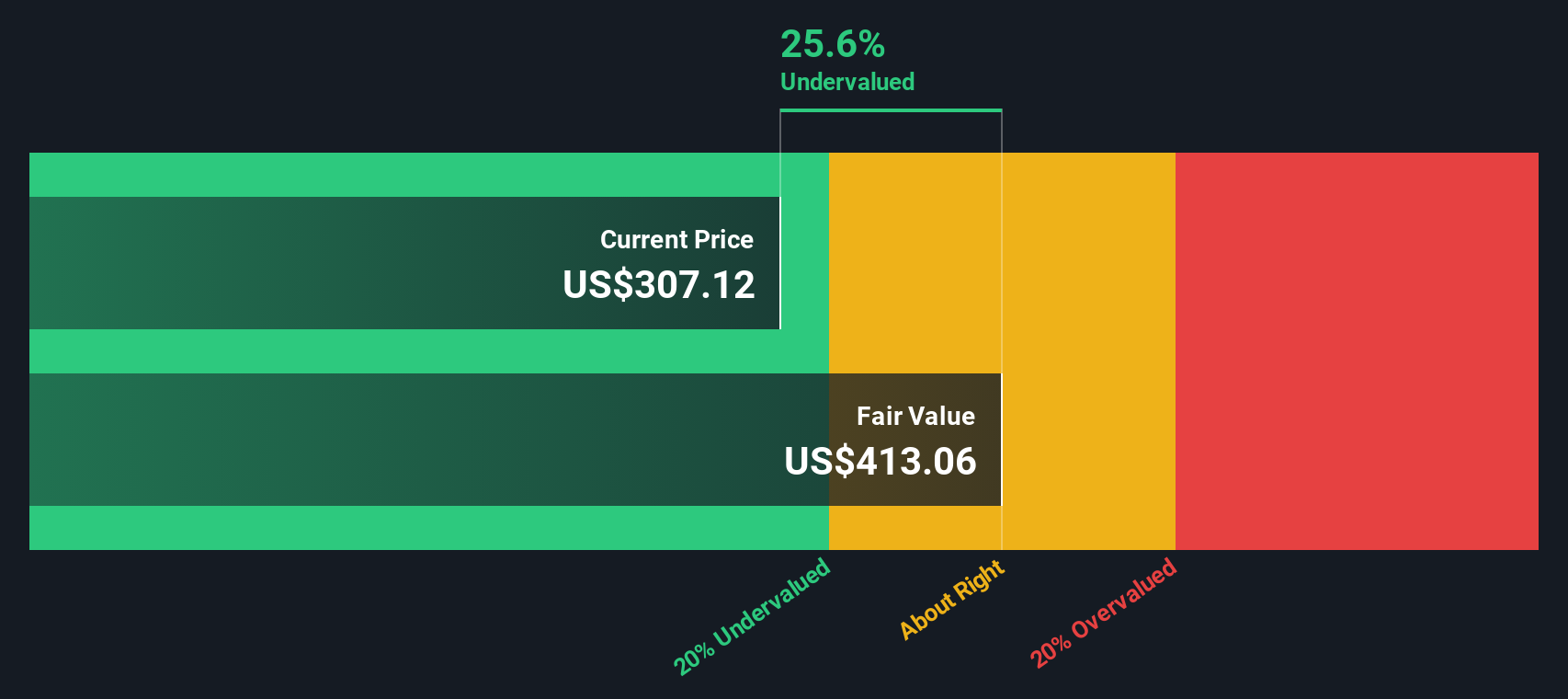

Most Popular Narrative: 4.9% Undervalued

The prevailing analyst consensus suggests Jones Lang LaSalle is trading nearly 5% below fair value, indicating mild undervaluation based on future earnings growth and improved margin outlook.

Continued investment in artificial intelligence, data technology, and unified global operating platforms is improving cost discipline, platform leverage, and operational efficiency. This is directly contributing to net margin and adjusted EPS expansion.

Curious about why analysts are so bullish on JLL's future? There is a hidden engine of recurring revenues, cutting-edge technology rollouts, and ambitious margin expansion plans at the heart of this valuation. Want to discover the financial levers that could push this premium even higher? The fair value math here relies on assumptions you will not want to miss.

Result: Fair Value of $335.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, a slowdown in office leasing or unexpected volatility in transactional markets could quickly dampen optimism around JLL’s growth story.

Find out about the key risks to this Jones Lang LaSalle narrative.Another View: What Does Our DCF Model Say?

Taking a step back from market-based ratios, our SWS DCF model suggests JLL could be even more undervalued than the preceding analysis implies. Could long-term cash flow trends be telling a different story about the company’s true potential?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Jones Lang LaSalle Narrative

If you see things differently or want to dig into the data yourself, building your own JLL narrative is quick and straightforward. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Jones Lang LaSalle.

Looking for More Investment Ideas?

Great investing opportunities are everywhere if you know where to look. Accelerate your next move by checking out handpicked stock ideas perfect for bold investors aiming for more than just average returns.

- Unlock high-growth potential in a sector reshaping medicine and patient care when you browse healthcare AI stocks.

- Capitalize on the latest tech trends by targeting innovative companies advancing the future with AI penny stocks.

- Boost your portfolio’s cash flow with companies offering attractive yields through dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.