JPMorgan’s Helium-Driven Upgrade Might Change The Case For Investing In Air Products (APD)

Air Products and Chemicals, Inc. APD | 293.55 | +1.42% |

- On March 20, 2026, JPMorgan upgraded Air Products and Chemicals to Overweight, citing the company’s resilient earnings profile despite macroeconomic pressures and benefits from tightening helium supply.

- The upgrade also underscored how rising helium prices, driven by geopolitical supply constraints, could support Air Products’ gas portfolio alongside its refinery-linked businesses.

- We’ll now examine how JPMorgan’s helium-focused rationale fits with Air Products’ existing investment narrative and expectations for future earnings.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Air Products and Chemicals Investment Narrative Recap

To own Air Products and Chemicals, you need to believe in its long term role in industrial gases and low carbon hydrogen, supported by large on site contracts and heavy project spending. JPMorgan’s upgrade, tied to tighter helium supply and resilient earnings, supports the near term earnings catalyst but does not materially change the key risk around high capital expenditure and potential project delays.

The most relevant recent announcement here is the new NASA liquid hydrogen contracts worth over US$140,000,000, which reinforce Air Products’ position in long duration hydrogen supply. These contracts sit alongside its broader hydrogen and clean ammonia build out, which many investors see as central to future earnings stability, even as helium volumes and pricing have been a source of uncertainty.

Yet while helium pricing currently supports the story, investors should be aware that...

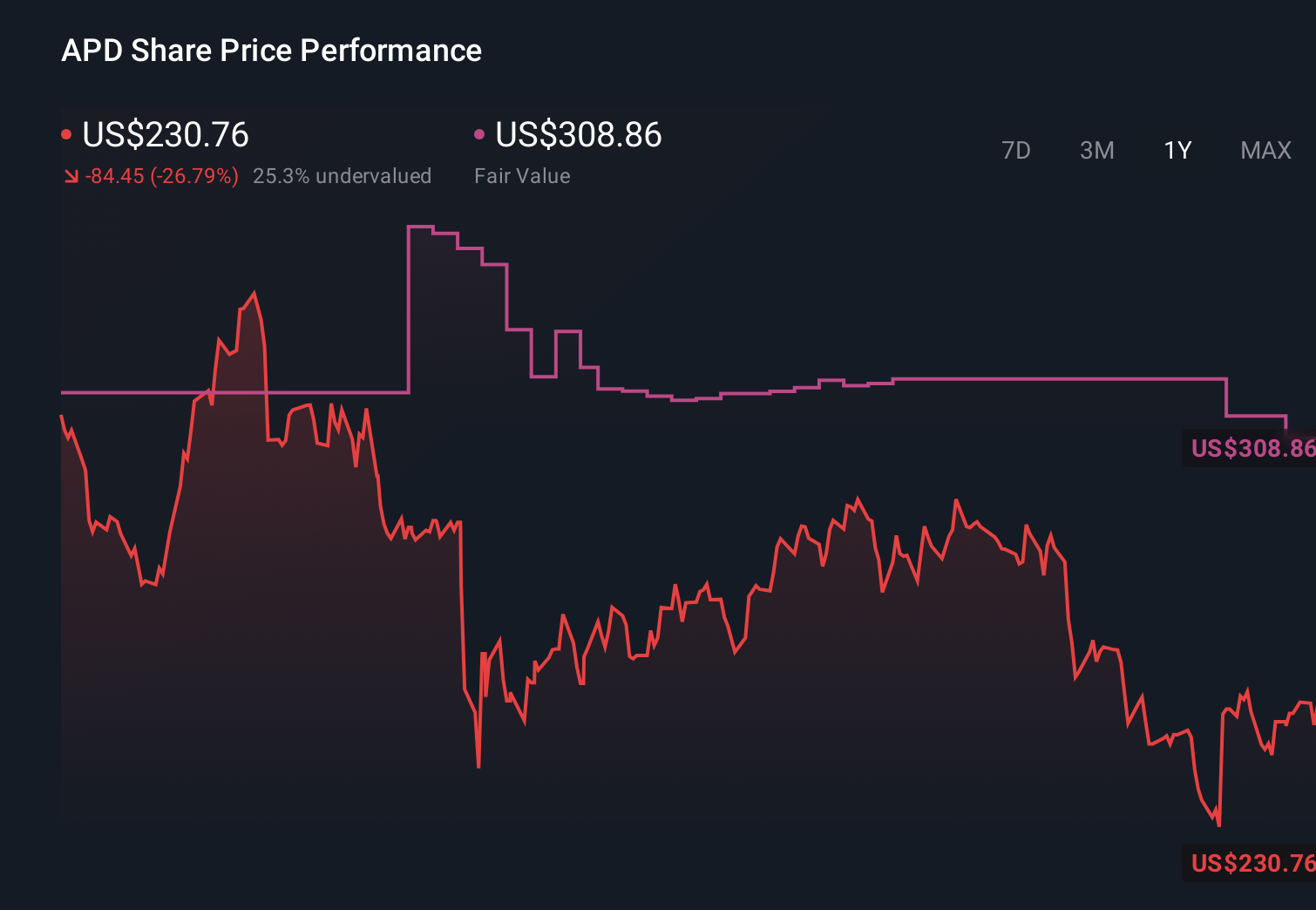

Air Products and Chemicals’ narrative projects $14.9 billion revenue and $3.8 billion earnings by 2028. This requires 7.4% yearly revenue growth and a roughly $2.2 billion earnings increase from $1.6 billion today.

Uncover how Air Products and Chemicals' forecasts yield a $306.77 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between about US$295 and US$307 per share, underscoring how even a small group can see things differently. You can weigh those views against the helium related earnings uncertainty and heavy project spend that could influence how Air Products’ performance unfolds over time.

Explore 2 other fair value estimates on Air Products and Chemicals - why the stock might be worth as much as $306.77!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Air Products and Chemicals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Air Products and Chemicals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Air Products and Chemicals' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 61 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.