Judge’s Dismissal of MINISO’s Securities Case Could Be A Game Changer For MINISO Group Holding (MNSO)

MINISO Group Holding Ltd. Sponsored ADR MNSO | 0.00 |

- In early May 2026, a federal judge in the Southern District of New York dismissed a securities lawsuit against MINISO Group Holding, ruling that investors had not sufficiently supported their claims around the Retail Partner Model and joint venture disclosures.

- This legal outcome removes a potential liability overhang and clarifies the company’s disclosure practices, which may influence how investors assess its governance and risk profile.

- With the lawsuit dismissed at the district court level, we’ll examine how this reduced legal overhang affects MINISO’s earnings-focused investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

MINISO Group Holding Investment Narrative Recap

To own MINISO, you need to believe its design led, IP heavy, largely offline retail model can keep drawing traffic and monetizing global store growth. The dismissal of the U.S. securities lawsuit removes a legal overhang, but it does not directly change the near term focus on earnings quality and margins, or the key risks around expansion, cost control and competition.

The most relevant recent disclosure here is MINISO’s April 2026 Form 6 K, which confirmed a stable share count, ongoing employee share incentives and compliance with Hong Kong public float rules. Together with the lawsuit dismissal, this helps clarify governance and capital structure at a time when investors are watching how buybacks, dividends and profit trends interact with store expansion and IP investment.

Yet even with the legal risk eased, you still need to weigh how rising costs and competition could affect MINISO’s margins and cash flows over time...

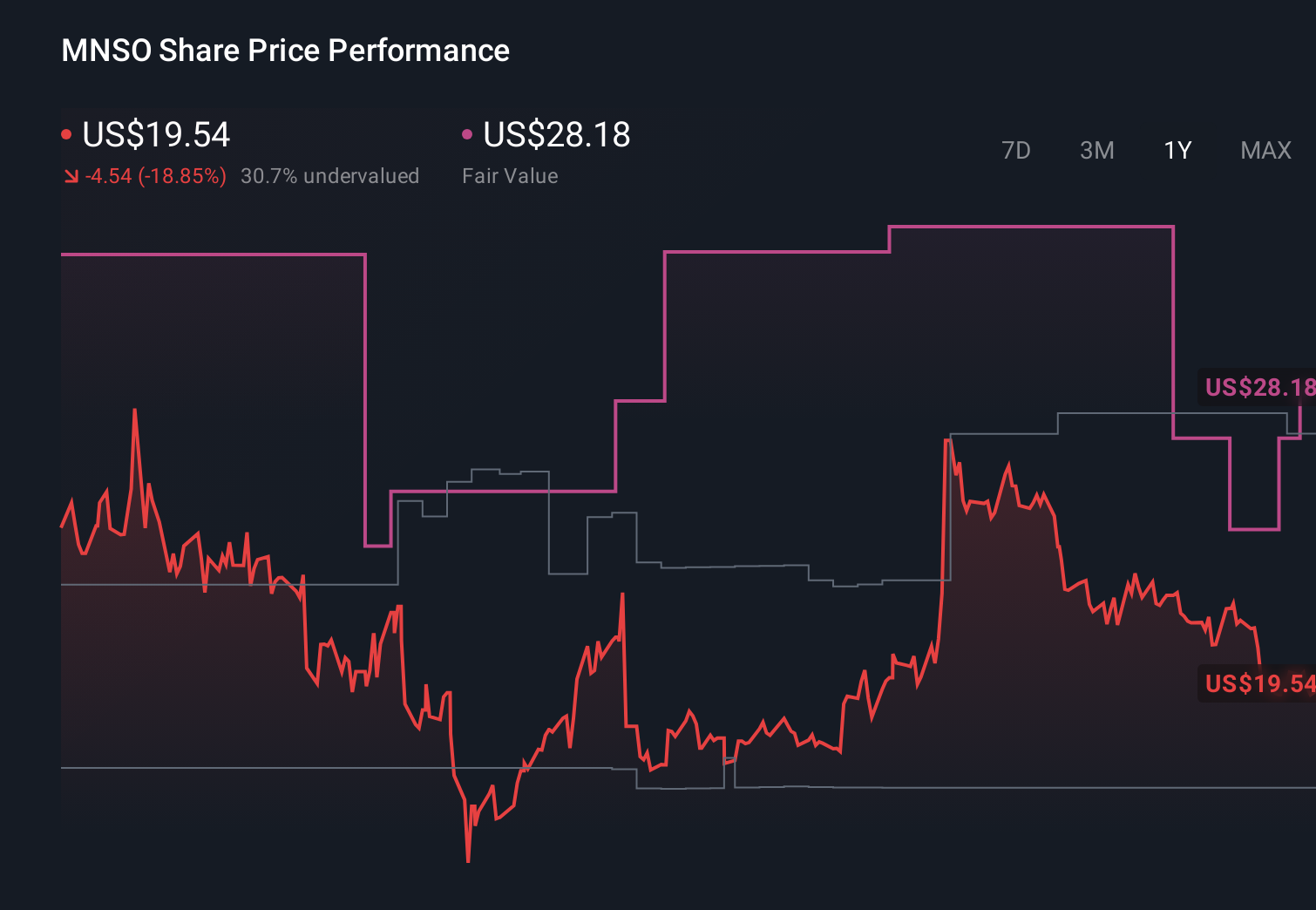

MINISO Group Holding's narrative projects CN¥33.1 billion revenue and CN¥3.9 billion earnings by 2029. This requires 15.6% yearly revenue growth and about CN¥2.7 billion earnings increase from CN¥1.2 billion today.

Uncover how MINISO Group Holding's forecasts yield a $23.25 fair value, a 60% upside to its current price.

Exploring Other Perspectives

The most cautious analysts were already assuming revenue of about CN¥32.3 billion and earnings of roughly CN¥3.6 billion by 2029, which bakes in slower growth and margin pressure than the consensus, so if you worry about online shopping eroding foot traffic, this more pessimistic view may feel closer to your own starting point, especially now that the legal news could shift how different investors weigh these competing narratives.

Explore 7 other fair value estimates on MINISO Group Holding - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MINISO Group Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MINISO Group Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MINISO Group Holding's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.