June 2026's Top Stocks Estimated Below Intrinsic Value

Everpure, Inc. Class A P | 0.00 |

In the last week, the United States market has stayed flat, yet it has experienced a significant 26% increase over the past year with earnings forecasted to grow by 16% annually. In such a robust environment, identifying stocks that are estimated to be below their intrinsic value can offer investors potential opportunities for growth and value appreciation.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Rayonier (RYN) | $21.02 | $40.87 | 48.6% |

| Oracle (ORCL) | $236.34 | $461.80 | 48.8% |

| Live Oak Bancshares (LOB) | $37.58 | $74.21 | 49.4% |

| Klaviyo (KVYO) | $15.78 | $31.17 | 49.4% |

| Inter & Co (INTR) | $5.76 | $11.10 | 48.1% |

| First Merchants (FRME) | $40.10 | $76.25 | 47.4% |

| FB Financial (FBK) | $53.12 | $101.61 | 47.7% |

| Coastal Financial (CCB) | $70.28 | $134.79 | 47.9% |

| BillionToOne (BLLN) | $104.59 | $203.29 | 48.6% |

| AbbVie (ABBV) | $224.94 | $439.38 | 48.8% |

Below we spotlight a couple of our favorites from our exclusive screener.

Coupang (CPNG)

Overview: Coupang, Inc. operates a retail business through mobile applications and internet websites in South Korea and internationally, with a market cap of $29.47 billion.

Operations: The company's revenue is primarily derived from Product Commerce, generating $29.90 billion, and Developing Offerings, contributing $5.23 billion.

Estimated Discount To Fair Value: 40.8%

Coupang is trading at 40.8% below its estimated fair value and more than 20% below its future cash flow value of US$27.93, suggesting potential undervaluation based on cash flows. Despite a recent net loss of US$266 million in Q1 2026, the company is expected to become profitable within three years and shows high return on equity forecasts. Coupang's strategic initiatives, including international expansion and AI-driven logistics enhancements, may bolster future revenue growth despite current slower-than-market projections.

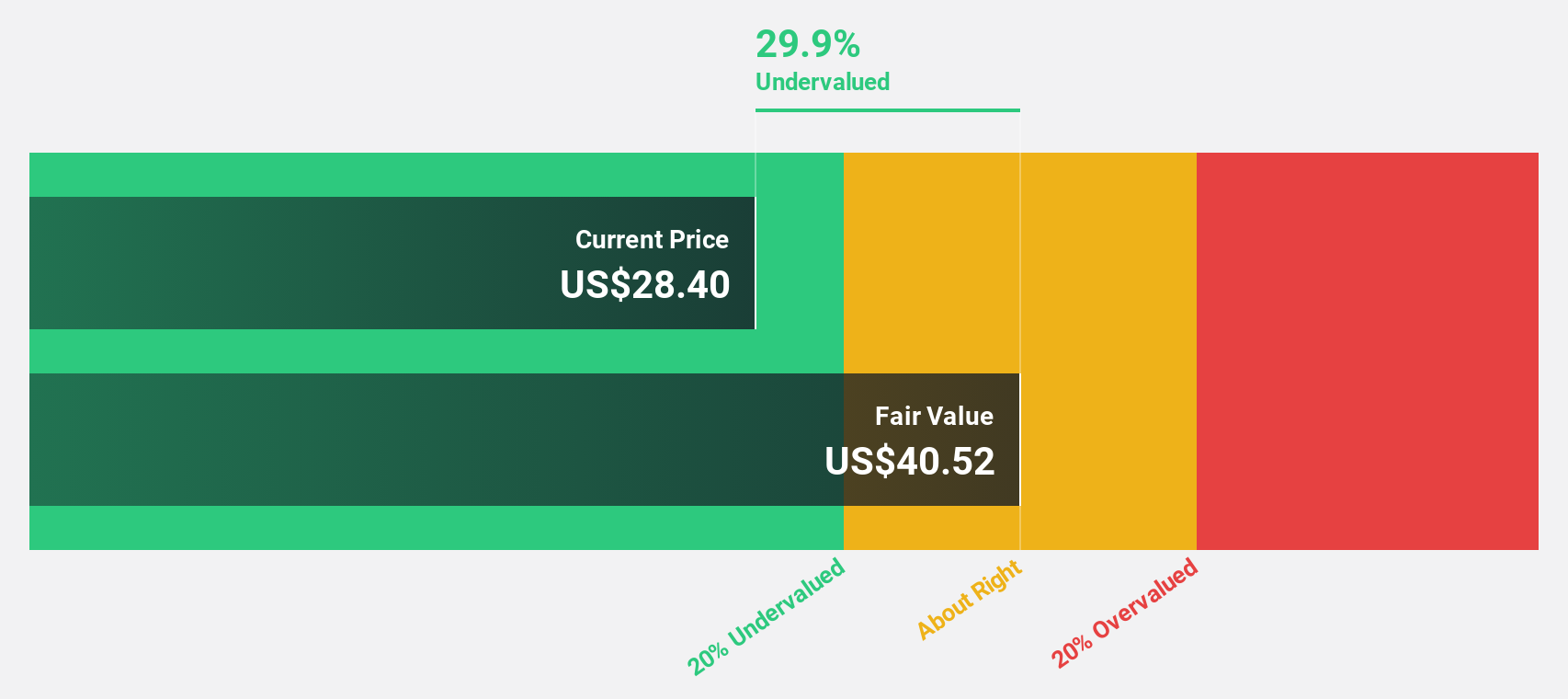

Everpure (P)

Overview: Everpure, Inc. offers data storage and management technologies, products, and services both in the United States and internationally, with a market cap of $26.85 billion.

Operations: The company's revenue is primarily generated from its Computer Storage Devices segment, amounting to $3.94 billion.

Estimated Discount To Fair Value: 36.1%

Everpure is trading 36.1% below its estimated fair value and over 20% below its future cash flow value of US$122.94, highlighting potential undervaluation based on cash flows. The company reported a significant earnings turnaround in Q1 2026 with net income of US$24.08 million compared to a loss last year, and raised its revenue guidance for fiscal year 2027. However, insider selling has been substantial recently, which could be a concern for investors.

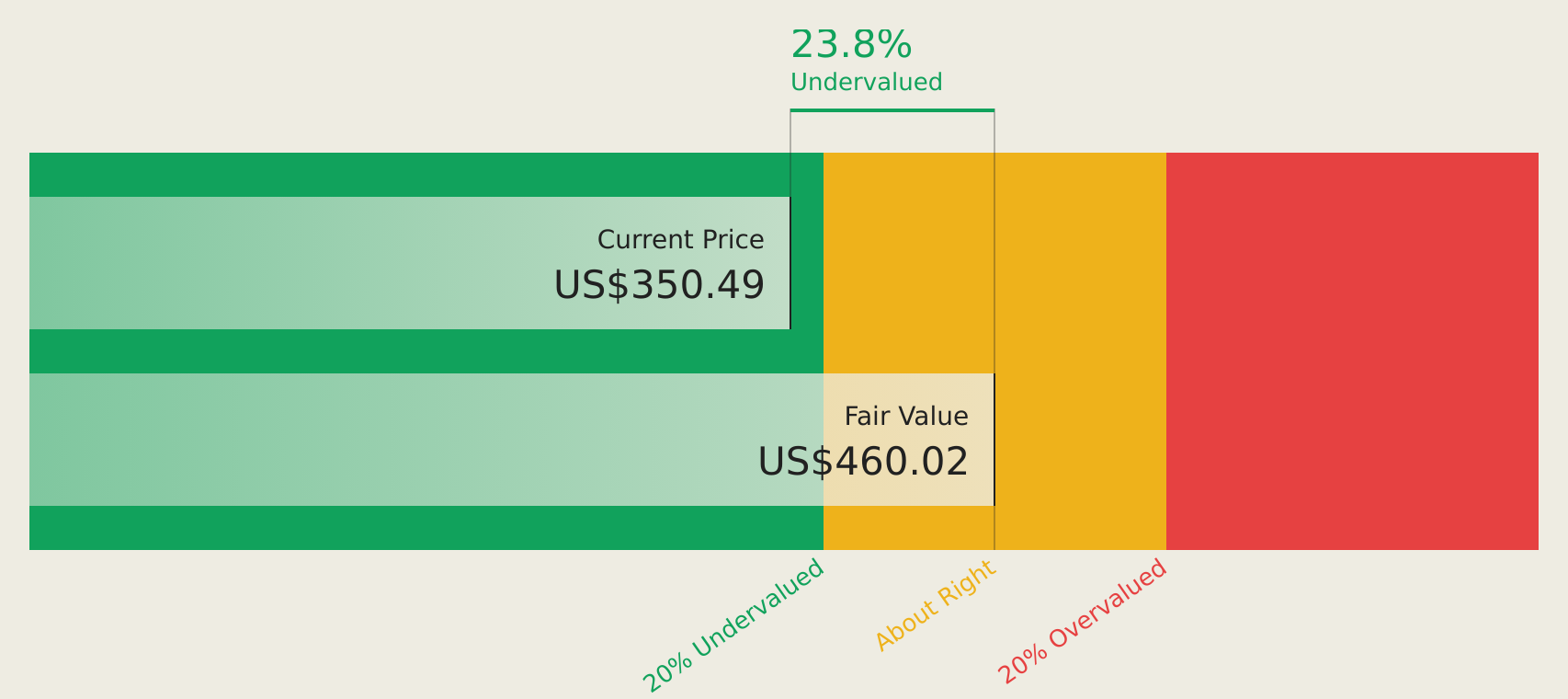

Waters (WAT)

Overview: Waters Corporation provides analytical workflow solutions across Asia, the Americas, and Europe, with a market cap of approximately $37.29 billion.

Operations: The company's revenue segments include Waters Division at $2.40 billion and TA Instruments Division at $0.28 billion.

Estimated Discount To Fair Value: 22.1%

Waters is trading 22.1% below its estimated fair value and over 20% below its future cash flow value of US$483.3, suggesting potential undervaluation based on cash flows. Despite a recent net loss of US$72 million in Q1 2026, revenue and earnings are forecast to grow faster than the market. However, profit margins have declined from last year, and shareholder dilution has occurred recently, which may be concerns for investors.

Key Takeaways

- Navigate through the entire inventory of 132 Undervalued US Stocks Based On Cash Flows here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.