June 2026's Top Undervalued Small Caps With Insider Action

Betterware de Mexico, S.A.P.I. de C.V. BWMX | 0.00 |

The United States market has shown robust performance, rising 1.2% in the last week and 27% over the past year, with earnings projected to grow by 17% annually. In such a thriving environment, identifying stocks that are undervalued yet exhibit insider action can offer unique opportunities for investors seeking potential growth within the small-cap sector.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.4x | 0.9x | 39.95% | ★★★★★★ |

| Financial Institutions | 9.3x | 3.0x | 28.96% | ★★★★★☆ |

| Angel Oak Mortgage REIT | 12.9x | 5.8x | 26.49% | ★★★★★☆ |

| AVITA Medical | NA | 1.8x | 49.11% | ★★★★★☆ |

| First Bancorp | 9.0x | 3.4x | 30.31% | ★★★★☆☆ |

| PCB Bancorp | 8.7x | 3.0x | 18.17% | ★★★★☆☆ |

| Union Bankshares | 9.2x | 1.9x | 21.81% | ★★★★☆☆ |

| Metropolitan Bank Holding | 13.0x | 3.7x | 39.88% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 34.59% | ★★★☆☆☆ |

| Patria Investments | 26.0x | 4.7x | 3.49% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

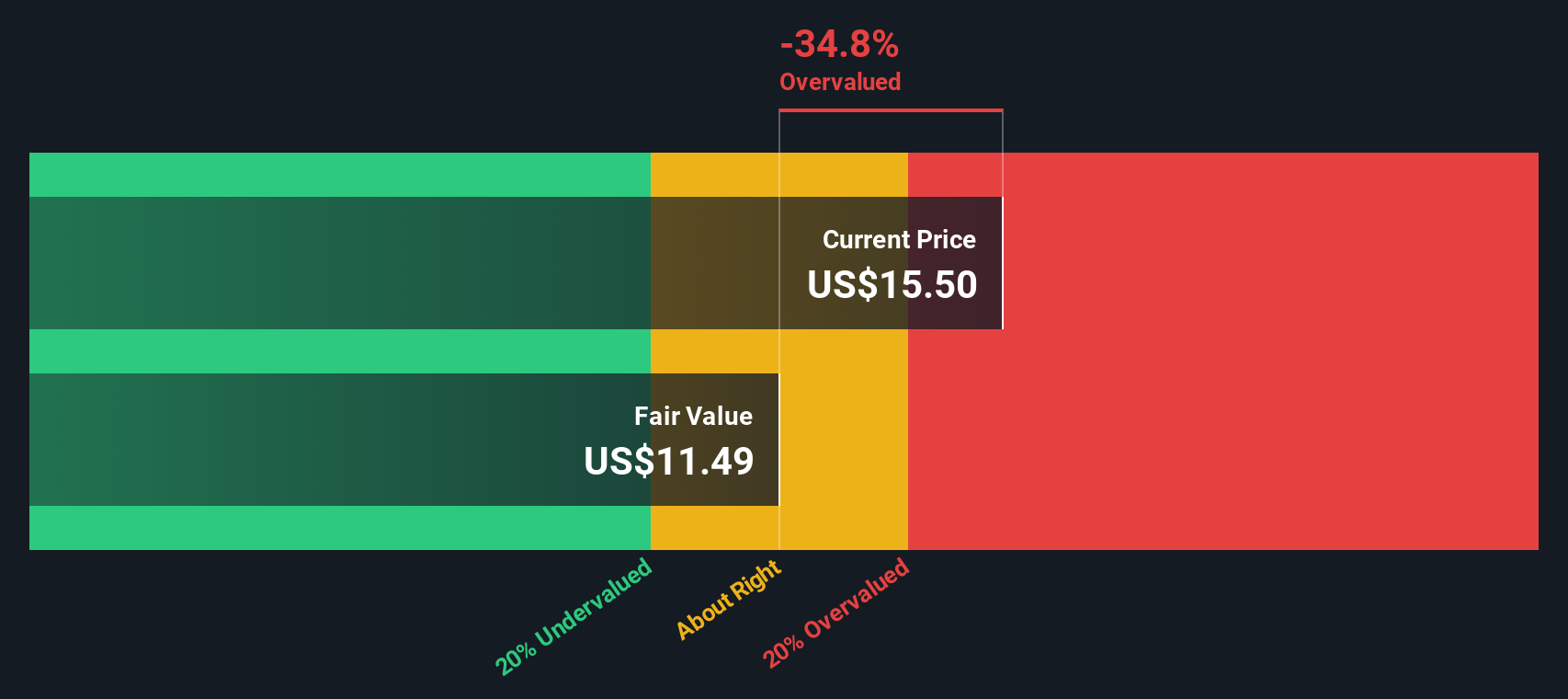

Patria Investments (PAX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Patria Investments is an asset management firm primarily focused on private equity, infrastructure, and credit investments, with a market capitalization of approximately $2.50 billion.

Operations: Patria Investments generates revenue primarily through its asset management segment, with a recent quarterly revenue of $399.23 million. The company experienced fluctuations in its gross profit margin, peaking at 78.37% in December 2020 and reaching a low of 58.07% by March 2026. Operating expenses have shown an upward trend, impacting the net income margins over time.

PE: 26.0x

Patria Investments, a smaller company in the U.S. market, recently reported Q1 2026 revenue of US$97.1 million, up from US$79.6 million the previous year, though net income dropped to US$2.3 million from US$15.7 million due to large one-off items affecting earnings quality. Insider confidence is evident with recent share purchases by insiders in early 2026, signaling potential undervaluation despite reliance on riskier external borrowing for funding and a forecasted annual earnings growth of 35%.

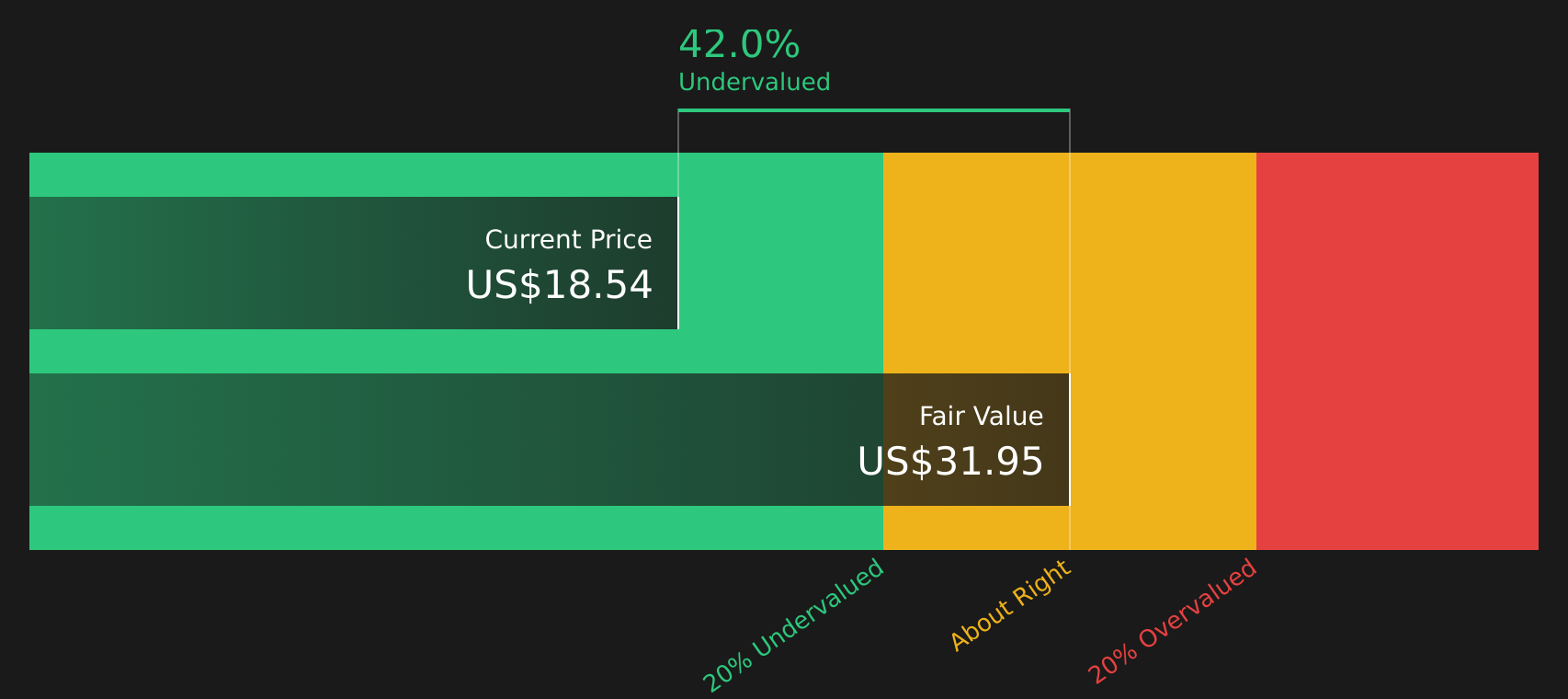

Betterware de MéxicoP.I. de (BWMX)

Simply Wall St Value Rating: ★★★★★★

Overview: Betterware de México is a direct-to-consumer company specializing in home organization and solutions products, with a market capitalization of MX$4.56 billion.

Operations: Betterware de México generates revenue primarily through product sales, with a recent revenue figure of MX$14.28 billion as of June 2026. The company's cost structure includes significant expenses in sales and marketing, which were MX$4.74 billion during the same period. Notably, the gross profit margin has shown variability over time, reaching 66.67% by June 2026.

PE: 10.4x

Betterware de México, a smaller company in the market, recently reported significant growth with net income jumping to MXN 281 million from MXN 151 million year-over-year. Despite high debt levels and reliance on external borrowing, insider confidence is evident as Andres Chevallier purchased 10,000 shares for US$168,062 between April and June 2026. The company's earnings are projected to grow by over 26% annually. However, a reduced dividend of US$0.2757 per share reflects cautious financial management amidst these dynamics.

CS Disco (LAW)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: CS Disco is a technology company that provides cloud-based legal solutions to law firms, corporations, and government agencies with a market cap of $1.11 billion.

Operations: CS Disco generates revenue primarily through the sale and support of its legal product offerings, with recent figures reaching $162.08 million. The company has experienced a gross profit margin trend peaking at 74.88% in March 2026, indicating efficient cost management relative to revenue generation. Operating expenses are significant, driven by sales & marketing and research & development costs, impacting net income margins over time.

PE: -6.4x

CS Disco, a player in the legal tech sector, is drawing attention for its potential as an undervalued stock. Despite a net loss of US$9.62 million in Q1 2026, revenue rose to US$41.88 million from US$36.65 million year-over-year. Insider confidence is evident with recent share purchases, suggesting faith in future prospects despite current volatility and reliance on external funding sources. A new partnership with Mound Cotton expands DISCO's reach in AI-powered eDiscovery solutions across the U.S., hinting at growth opportunities ahead.

Taking Advantage

- Discover the full array of 77 Undervalued US Small Caps With Insider Buying right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.