Kaiser Aluminum (KALU) Valuation Check After Fund Spotlight And Capacity Expansion Progress

Kaiser Aluminum Corporation KALU | 131.98 133.37 | +1.22% +1.05% Post |

Third Avenue Small-Cap Value Fund recently put Kaiser Aluminum (KALU) in the spotlight after reporting quarterly financial results and progress on a multi year capacity expansion in aerospace and packaging.

At a share price of US$125.09, Kaiser Aluminum has seen a 90 day share price return of 17.53% and a year long total shareholder return of 91.11%. This suggests recent momentum following the fund's positive commentary and capacity expansion progress, rather than earlier multi year performance.

If this focus on aerospace and packaging has your attention, it could be a good moment to broaden your watchlist with 8 top copper producer stocks that screen for other materials names tied to industrial demand.

Yet with Kaiser Aluminum trading around US$125 and sitting close to its analyst price target, the key question for you is whether the market is overlooking value in its specialty aluminum portfolio or has already priced in the next stage of growth.

Most Popular Narrative: 17.5% Overvalued

With Kaiser Aluminum closing at $125.09 against a most followed fair value of $106.50, the current price sits above that narrative anchor and puts extra focus on the assumptions behind it.

Completion of the Trentwood Phase 7 plate expansion positions Kaiser to capture rising commercial aircraft and defense build rates, which may lift aerospace conversion revenue and support a return to mid to high 20 percent EBITDA margins as volumes normalize.

Want to see what kind of volume recovery and margin rebuild that sentence is really pointing to? The most followed narrative leans on a specific mix of revenue growth, margin improvement and a future earnings multiple that has to line up precisely with those capacity projects and demand forecasts. If you are wondering how that combination feeds into a $106.50 fair value while the market trades higher, the full narrative lays out the step by step math.

Result: Fair Value of $106.50 (OVERVALUED)

However, there is still a chance that stronger than expected aerospace and packaging margins, or faster balance sheet improvement and cash returns, could challenge that overvalued call.

Another View: Multiples Paint A Different Picture

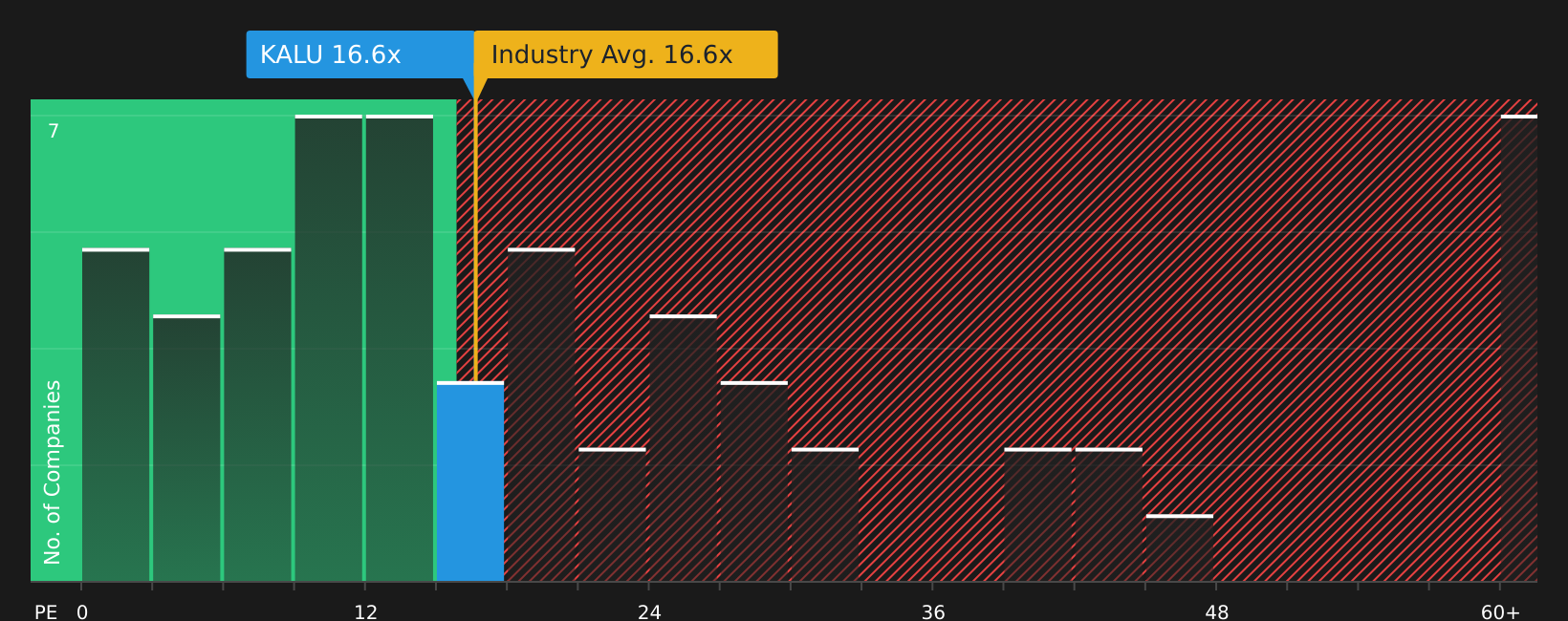

While the most followed narrative pins Kaiser Aluminum at $106.50 and calls the stock overvalued, current pricing at about 17.9x P/E tells a different story. That P/E sits well below peers at 71.5x and under a 21.1x fair ratio. This points to valuation risk that may be more skewed toward missing potential upside than paying too much. So which signal do you trust more: the narrative fair value or the earnings multiple?

Next Steps

With mixed signals on value and plenty of moving parts, consider reviewing the full picture yourself and acting promptly while the market continues to debate, starting with 4 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Kaiser Aluminum has sharpened your interest, do not stop here, use the Simply Wall St screener to quickly surface other focused opportunities that match your style.

- Target quality at a discount by scanning our 48 high quality undervalued stocks that pair stronger fundamentals with prices that may not fully reflect them.

- Build a steadier income stream by reviewing 14 dividend fortresses that aim for higher yields alongside durable payout histories.

- Sleep a little easier by checking 68 resilient stocks with low risk scores designed to highlight companies with lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.