Kaiser Aluminum (KALU) Valuation Check After Higher Sales And Net Income Drive Fresh Investor Interest

Kaiser Aluminum Corporation KALU | 131.62 | +0.47% |

Kaiser Aluminum (KALU) just released fourth quarter and full year 2025 results, reporting higher sales and net income than a year earlier. This gives investors fresh numbers to assess the stock’s recent momentum.

The earnings release has come alongside strong recent price action, with a 1-day share price return of 3.70% and a 90-day share price return of 37.29%. The 1-year total shareholder return of 103.76% and 3-year total shareholder return of 88.53% point to momentum that has been building over several time frames.

If Kaiser Aluminum's recent run has caught your eye, this could be a good moment to broaden your search with our screener of 8 top copper producer stocks as another way to find metals and materials names worth a closer look.

With earnings improving and the share price already up sharply, Kaiser Aluminum now trades at a premium to the average analyst target but still screens as materially undervalued on some models. Is this a fresh opportunity, or has the market already priced in future growth?

Most Popular Narrative: 26.7% Overvalued

Compared with the most followed narrative fair value of $106.50, Kaiser Aluminum's last close at $134.96 implies a richer price than those assumptions support.

In order for you to agree with the analysts, you'd need to believe that by 2028, revenues will be $4.2 billion, earnings will come to $172.0 million, and it would be trading on a PE ratio of 13.4x, assuming you use a discount rate of 9.6%.

Want to see what underpins that valuation gap? The narrative leans on faster earnings growth, firmer margins, and a lower future earnings multiple. The exact mix of assumptions might surprise you.

Result: Fair Value of $106.50 (OVERVALUED)

However, if aerospace and packaging margins climb closer to mid to high 20% EBITDA, or free cash flow improves faster than expected, today’s implied overvaluation could look conservative.

Another View: Multiples Paint A Different Picture

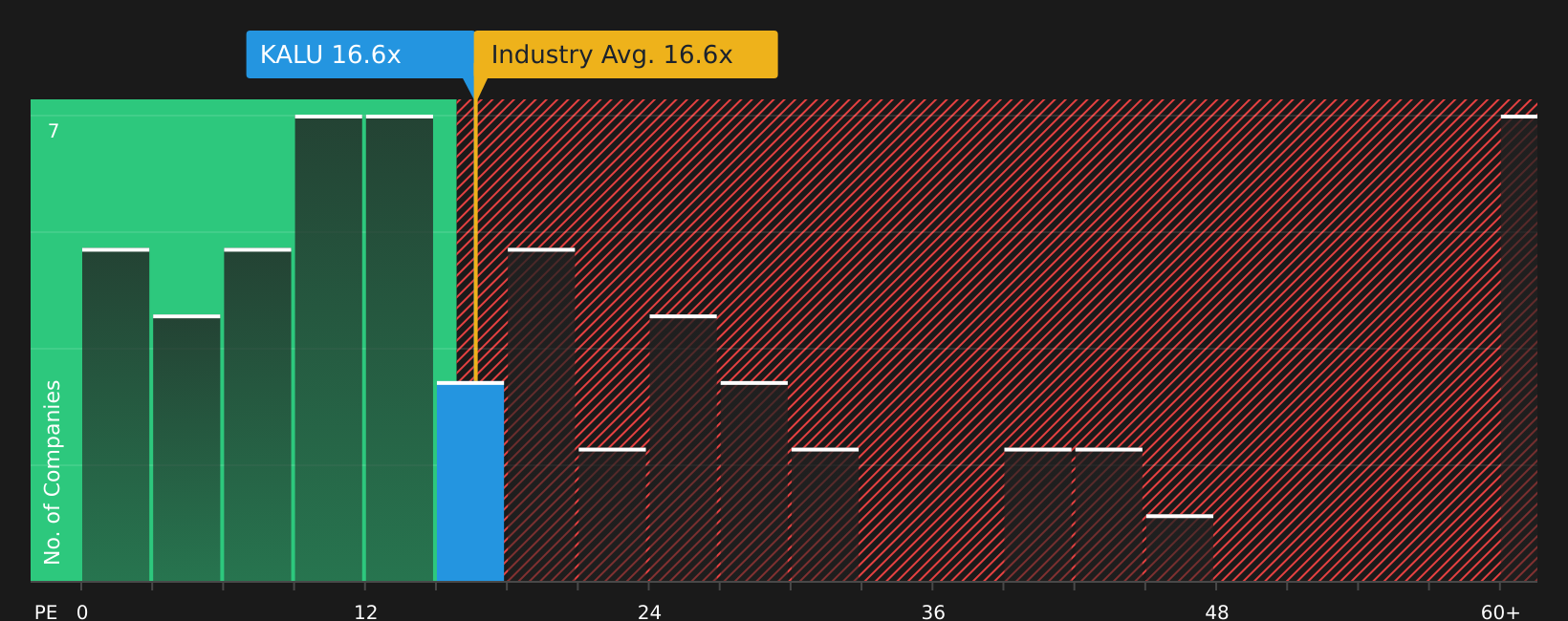

That 26.7% overvaluation signal from the narrative contrasts with how the market is actually pricing Kaiser Aluminum today. On a P/E of 19.3x, the shares sit below the fair ratio of 21.3x, and also below both peers at 74.6x and the US Metals and Mining industry at 23.5x. That gap can hint at either a margin of safety or a sign that expectations are more muted than the story suggests, so which side do you think it sits on?

Next Steps

If this mix of optimism and concern around Kaiser Aluminum feels finely balanced, now is a good time to look through the numbers yourself and decide where you stand. To quickly see how those cross currents stack up, take a look at the 4 key rewards and 2 important warning signs.

Ready for more investment ideas?

If Kaiser Aluminum has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to identify other opportunities.

- Chase value by scanning our list of 45 high quality undervalued stocks that combine quality fundamentals with prices that still look reasonable.

- Support your income objectives by reviewing 13 dividend fortresses designed for investors who want yields that stand out without ignoring balance sheet strength.

- Prioritize resilience by checking 76 resilient stocks with low risk scores that aim to keep overall risk in check while you position for long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.