Kinsale Capital Group (KNSL) Stock After 34% Slide Is The Reset Overdone?

Kinsale Capital Group, Inc. KNSL | 0.00 |

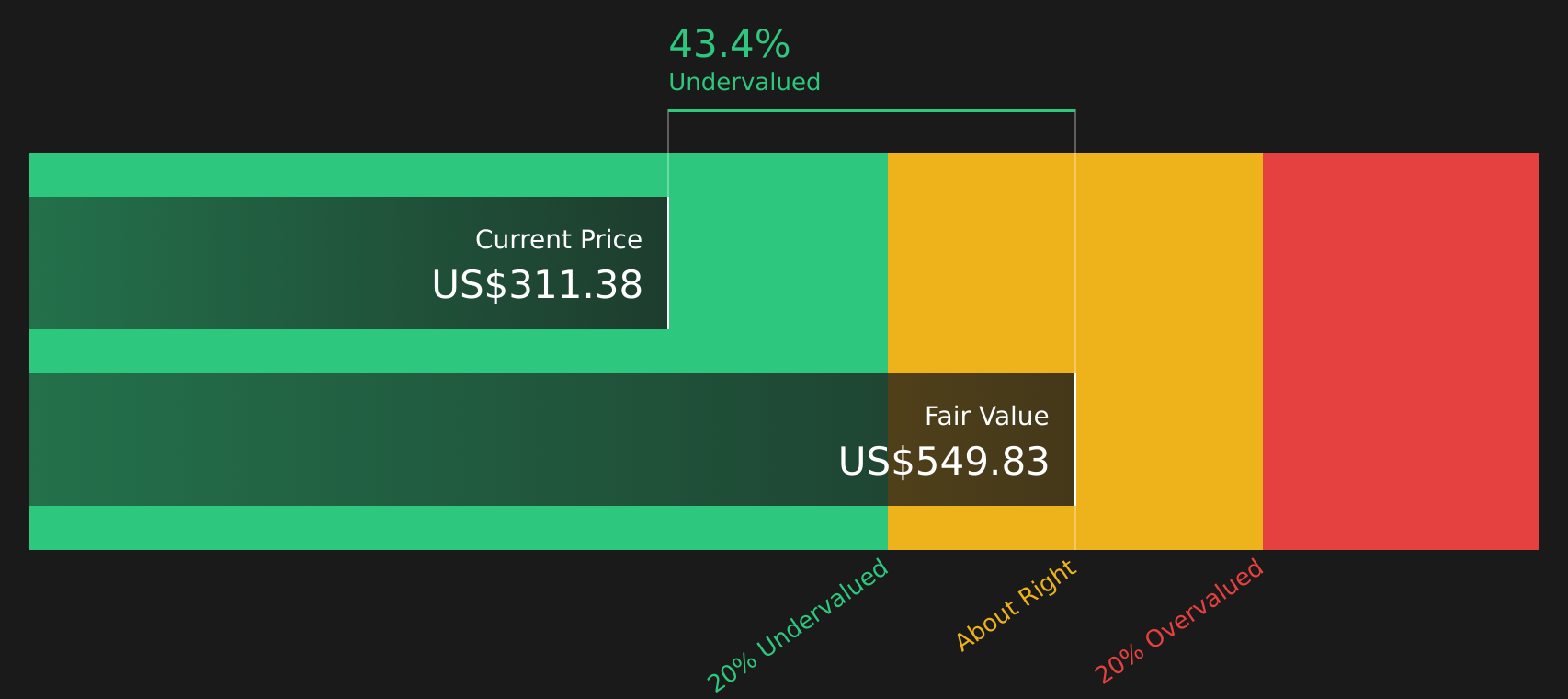

- If you are wondering whether Kinsale Capital Group at around US$311 per share is a bargain or a stock to be cautious about, the key question is how its current price lines up against its underlying value.

- The stock has inched up 1.7% over the last week and 3.6% over the last month, yet it is still down 20.7% year to date and has declined 34.2% over the past year. This may have some investors reassessing both its potential and its risks.

- Recent coverage has focused on Kinsale as a specialist insurer and on how investor sentiment has shifted after a period of strong longer term returns, with the stock up 100.8% over five years. That context helps explain why some shareholders are now questioning whether recent weakness reflects changing fundamentals or simply a reset in expectations.

- On Simply Wall St's valuation checks, Kinsale scores 2 out of 6, which means only some of the metrics point to the stock trading below estimated fair value. Next up is a closer look at different valuation approaches and, by the end of the article, a broader way to think about what that valuation score really tells you.

Kinsale Capital Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Kinsale Capital Group Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to generate over and above the return required by shareholders, then attributes that surplus to each share.

For Kinsale Capital Group, the model starts with an estimated Book Value of $85.31 per share and a Stable EPS of $23.36 per share, based on weighted future Return on Equity estimates from 9 analysts. The Average Return on Equity is 22.09%, which is compared with a Cost of Equity of $7.52 per share.

The difference between the earnings attributed to shareholders and their required return gives an Excess Return of $15.85 per share. That stream of surplus returns, applied to a Stable Book Value of $105.73 per share, is used to estimate what the stock could be worth today.

On this Excess Returns view, the implied intrinsic value is $549.83 per share, which suggests the stock is 43.4% undervalued relative to the current price of about $311.

Result: UNDERVALUED

Our Excess Returns analysis suggests Kinsale Capital Group is undervalued by 43.4%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

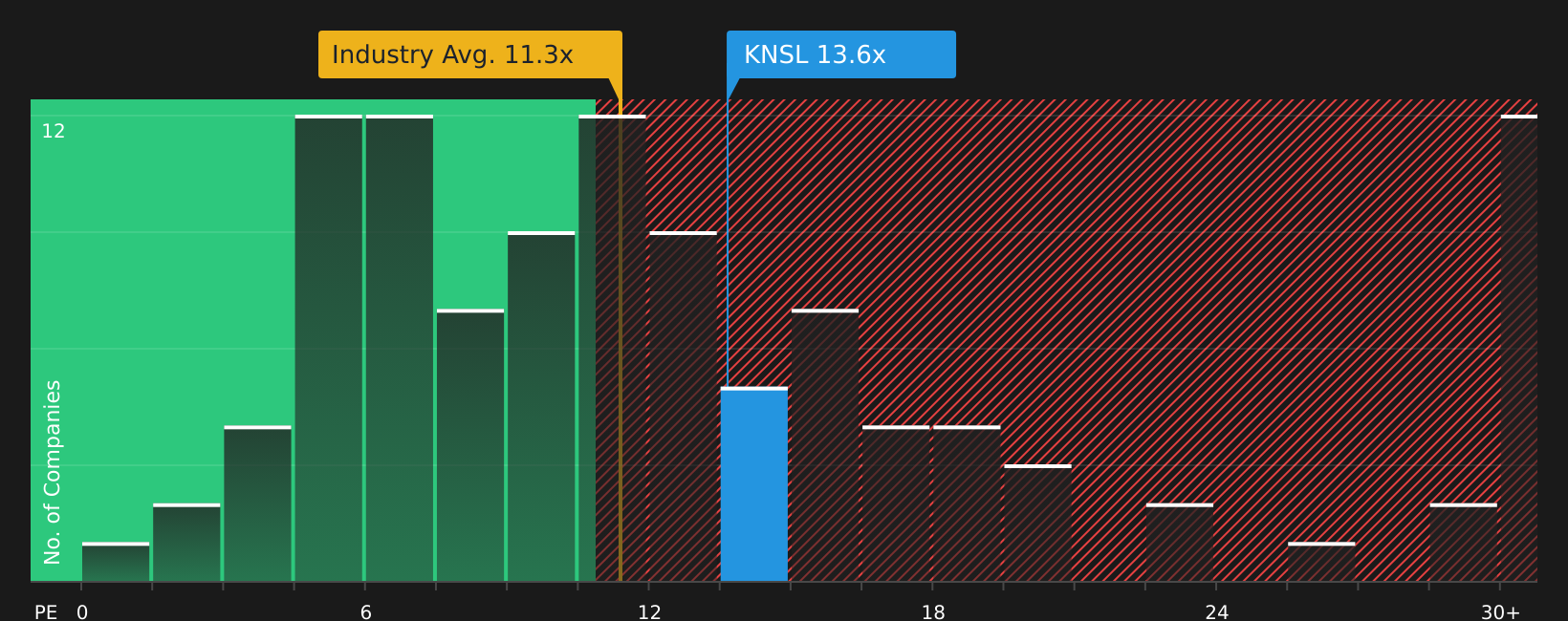

Approach 2: Kinsale Capital Group Price vs Earnings

For a profitable company like Kinsale Capital Group, the P/E ratio is a straightforward way to gauge how much you are paying for each dollar of earnings. This makes it a useful cross check against the earlier intrinsic value estimate.

A higher or lower P/E often reflects what the market is pricing in for growth and risk. Higher expected earnings growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually justifies a lower multiple.

Kinsale currently trades on a P/E of 13.63x. This sits above the Insurance industry average of 11.28x and above the peer average of 8.36x, which on simple comparisons can make the stock look relatively expensive.

Simply Wall St’s Fair Ratio for Kinsale is 10.68x. This proprietary metric aims to estimate a company specific P/E by incorporating factors such as earnings growth, profit margins, risk profile, industry and market cap, rather than relying on broad peer or industry averages that may not closely match the company.

Comparing the Fair Ratio of 10.68x with the current P/E of 13.63x indicates that the stock is trading at a premium to what these fundamentals might justify.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Kinsale Capital Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as simple stories that you create about Kinsale Capital Group, linking your view of its business, revenue, earnings and margins to a financial forecast and then to an assumed fair value that can be compared with the current share price.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors, allowing you to see different fair value estimates side by side, so you can decide whether the current market price looks high or low relative to the story you find most reasonable.

Narratives also update automatically when new information such as earnings or news is added to the platform, so your fair value view of Kinsale can shift in real time as the facts change.

For example, one Kinsale Narrative might lean toward the higher end of analyst assumptions with a fair value around US$450 per share, while another leans toward the lower end near US$267. Comparing those stories helps you choose which set of assumptions about growth, margins and risk best matches your own view before deciding how to act.

For Kinsale Capital Group, however, we will make it really easy for you with previews of two leading Kinsale Capital Group Narratives:

On Simply Wall St, each Narrative links these kinds of assumptions about revenue, earnings, margins and valuation into a joined up story, so you can see how different views of the same company can lead to very different fair value estimates.

Fair value in this bullish Narrative: US$354.67 per share.

Implied discount to this fair value based on the latest close near US$311.38: about 12.2% undervalued.

Revenue growth assumption: 3.29% a year.

- Focuses on expansion in excess and surplus lines, including small business property, high value homeowners and agribusiness, supported by Kinsale's technology platform and low expense ratio.

- Sees conservative underwriting, reserving discipline and a strong operating return on equity as key supports for earnings and capital returns over time.

- Highlights risks from competition, inflation, catastrophe exposure and slower submission growth, but still aligns with the analyst consensus price target of US$354.67.

Fair value in this bearish Narrative: US$309.00 per share.

Implied premium to this fair value based on the latest close near US$311.38: about 0.8% overvalued.

Revenue growth assumption: 6.04% a year.

- Emphasises that Kinsale's cost and technology edge could narrow if peers catch up, which may pressure underwriting margins in more competitive lines.

- Flags risks from AI model errors, litigation heavy casualty lines and expansion into newer segments where the company has a shorter track record.

- Frames US$309.00 as a bearish price target that sits well below prior consensus, assuming margin compression and a P/E of 17.4x on 2029 earnings.

Taken together, these Narratives show how two sets of reasonable assumptions can point to fair values that sit either side of the current share price, which is why it is so important to decide which story you find more convincing before taking any action on the stock.

Once you have a clear view on which Narrative matches your expectations for Kinsale's growth, margins and risk, you can then decide how, or whether, the current price fits into your broader portfolio and risk tolerance.

Do you think there's more to the story for Kinsale Capital Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.