KKR Stock And Private Credit Flows What Institutional Buying Could Mean

Apollo Global Management Inc APO | 0.00 |

Institutional capital is flowing into private credit again, with North American direct lending funds attracting at least $16b in Q2 and signaling that big investors are still keen on alternative lenders even as smaller clients pull back. That kind of funding backdrop can reshape how credit is provided, how risk is priced, and which stocks stand to benefit or face pressure. This article explains what that shift in funding might mean for your portfolio and highlights 3 stocks exposed to this private credit news that may warrant a closer look, whether you are focused on potential opportunities or on understanding the risks.

KKR (KKR)

Overview: KKR & Co. Inc. is a global investment firm that raises capital from institutions and wealthy investors and then deploys it into private equity, real estate, private credit and other alternative assets, aiming to grow and manage those investments over many years. It is involved in a wide range of deals including buyouts, growth financing, infrastructure projects and impact investments across North America, Europe and Asia.

Operations: KKR reports most of its revenue from Insurance at about US$12.3b, alongside a Segment Adjustment of roughly US$6.7b.

Market Cap: US$84.3b

Investors watching the renewed surge of institutional money into private credit may find KKR interesting because it sits at the center of that flow, with a large private credit platform and growing exposure to asset-based finance, aircraft leasing and infrastructure. Analysts expect earnings growth of 31.4% a year, although revenue is forecast to decline, which points to a focus on margins and fee mix rather than simple top line expansion. Recent deals in renewables, AI infrastructure and services show KKR continuing to put large amounts of capital to work while maintaining an experienced management team and active buybacks. The company also faces concentration in higher risk funding and sector specific credit risks that could have an impact if defaults rise, so the full picture is more nuanced than the headlines suggest.

KKR’s earnings outlook and private credit engine are accelerating, but the real story sits in how analysts see that playing out over time, so check the analyst forecasts for KKR and what they might be missing.

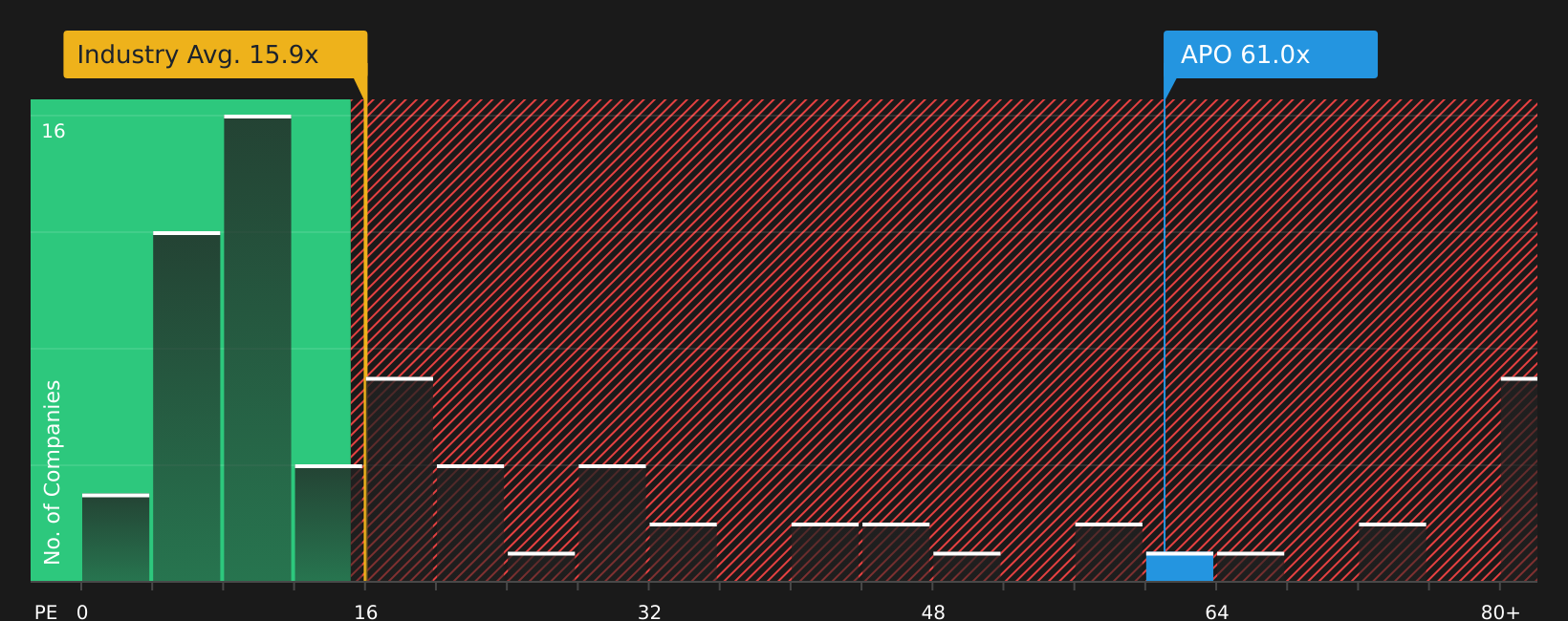

Apollo Global Management (APO)

Overview: Apollo Global Management is a large US based alternative asset manager that puts money to work across private credit, private equity, real estate, infrastructure and related strategies for institutions and individual investors, aiming to earn fees for managing those assets and potential gains on its own investments. The firm backs everything from buyouts and restructurings to income focused credit, often stepping in where traditional lenders are less active.

Operations: Apollo generates most of its revenue from Retirement Services at about US$24.3b, alongside roughly US$5.8b from Asset Management and about US$1.5b from Principal Investing.

Market Cap: US$68.4b

Apollo Global Management sits at the heart of the private credit story, with large direct lending and investment grade credit platforms that can benefit when big institutions commit fresh capital even as some retail investors step back. At the same time, the stock trades on a rich P/E, profit margins have recently compressed to 3.7% and revenue is forecast to decline sharply. Liquidity caps on certain private credit funds and reliance on higher risk external funding underline that this is not a low risk profile. For investors weighing that mix of growth expectations, valuation premium and funding pressures, the full analysis report for Apollo Global Management spells out what is priced in and where expectations could prove too optimistic or too cautious.

Apollo Global Management’s rich P/E and compressed 3.7% margin could be masking where the real earnings engine is heading, so walk through the story in the analyst forecasts for Apollo Global Management and see what might be quietly building.

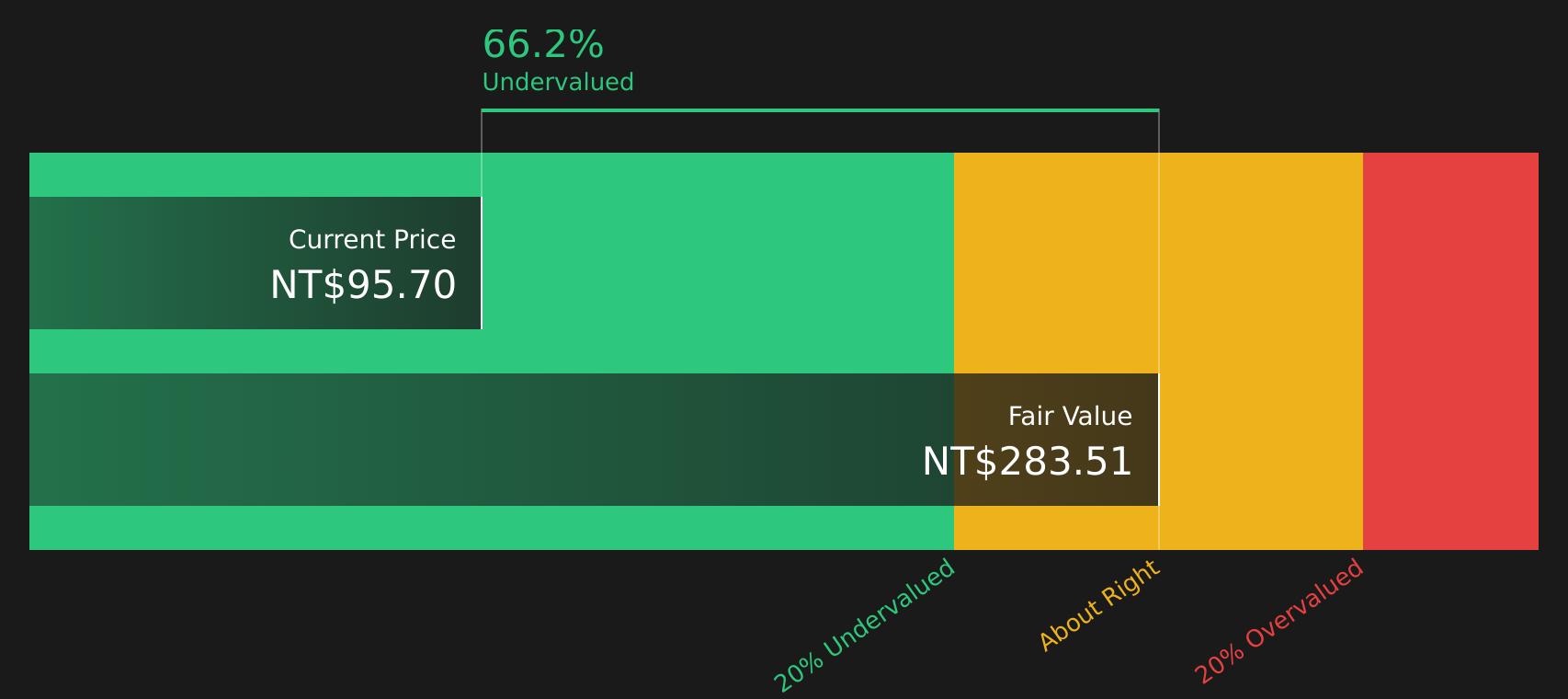

Kuang Hong Arts Management Incorporation (TPEX:6596)

Overview: Kuang Hong Arts Management Incorporation runs live music, arts exhibitions and other cultural events in Taiwan, and also provides supporting services such as stage construction, manpower dispatch and drama production and performances.

Operations: Kuang Hong Arts Management Incorporation generates all of its revenue of about NT$3.2b from recreational activities in Taiwan.

Market Cap: NT$3.6b

Kuang Hong Arts Management Incorporation provides exposure to Taiwan’s live events and cultural sector. Recent earnings growth has been strong and the company reports a 20.1% net margin and a 63% ROE. The stock trades at a P/E of 5.6x and at a large discount to one estimate of fair value. However, it has lagged both the broader TW market and its Hospitality peers, which may draw the attention of investors who focus on potential mispricing. A key consideration is the very high 19.62% dividend yield, which is not well covered by earnings or free cash flow, together with a balance sheet funded entirely by higher risk borrowing. The central question for investors is whether the current valuation appropriately reflects these funding and payout pressures.

Kuang Hong Arts Management Incorporation’s low 5.6x P/E and 63% ROE hint that the market may be misreading the trade off between earnings power and that 19.62% dividend strain, so walk through the analysis report for Kuang Hong Arts Management Incorporation

Take Control of Your Investment Journey

If KKR or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh stock ideas do not stay under the radar for long, and once momentum builds the best entry points can be captured quickly. Scan these curated lists to review potential opportunities at an earlier stage.

- Explore resilient compounding potential with a curated set of defensive businesses screened for strength using the list of solid balance sheet and fundamentals (47 results).

- Review structural demand shifts by focusing on miners screened in the 8 top copper producer stocks that could sit at the center of long term infrastructure and electrification themes.

- Assess opportunities in automation by reviewing companies highlighted through the 29 robotics and automation stocks before increased interest places them more firmly on the market’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.