Klarna Group (KLAR) Could Be 55% Undervalued If Its Growth Narrative Holds

Klarna Group Plc KLAR | 0.00 |

Klarna Group (KLAR) shares have been active after recent trading, with the stock closing at $19.13. Investors are weighing its 15.5% annual revenue growth and a reported net loss of $198 million.

Over the past quarter, Klarna Group has seen a 55.9% 90 day share price return and a 12.7% 30 day share price return, while the year to date share price return remains down 33.0%. This suggests recent momentum is rebuilding after earlier weakness.

If Klarna’s payments story has your attention, it might be a good moment to widen your watchlist and check out 20 top founder-led companies

With Klarna Group combining 15.5% annual revenue growth, a reported net loss of $198 million, and a discount of about 22% to analyst price targets, investors may be wondering whether the recent rebound is a genuine buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 55.5% Undervalued

Compared with Klarna Group’s last close at $19.13, the most followed narrative anchors fair value at $43.01, putting a very large gap between market price and that estimate.

My fair value of $43.01 represents a significant vote of confidence in Klarna’s ability to maintain this trajectory. While the broader market often fluctuates based on interest rate fears, the "narrative of the $43" is one of undervalued efficiency.

Curious what has to happen for that $43.01 figure to hold up? The narrative leans on stronger earnings, firmer margins, and a future profit multiple that assumes Klarna Group matures into a full digital bank and shopping assistant. The exact mix behind that view is where the story gets interesting.

Result: Fair Value of $43.01 (UNDERVALUED)

However, Klarna Group’s reported net loss of $198 million and the intrinsic discount signal that profitability expectations built into this narrative could still prove fragile.

Another View on Klarna Group’s Value

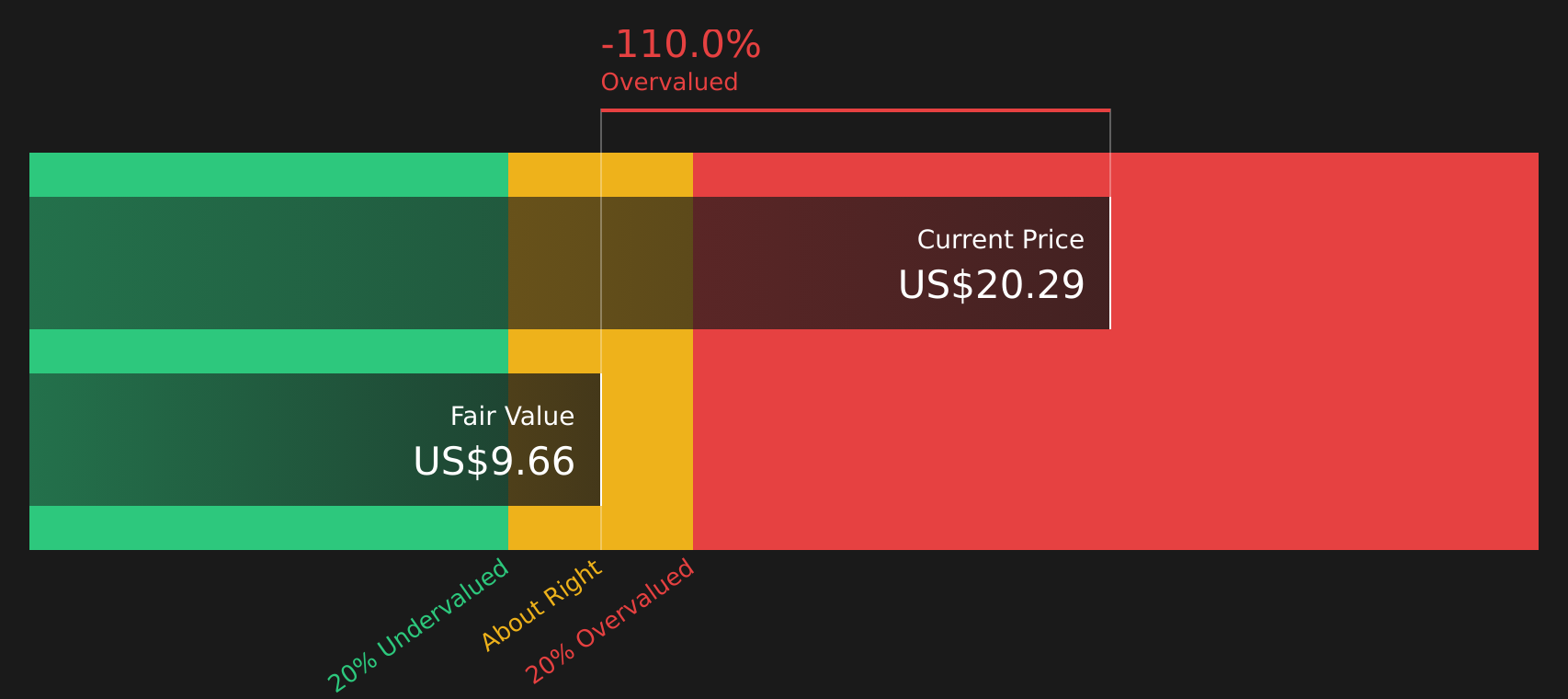

There is a clear tension between the $43.01 fair value narrative and our DCF result. The SWS DCF model estimates Klarna Group’s future cash flows support a value of $9.62 per share, which sits well below the current $19.13 price and flags the stock as overvalued.

That kind of gap raises a practical question for you as an investor: which story of Klarna Group’s future do you trust more, the optimistic narrative or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the split in views on Klarna Group leaves you unsure, do not wait for consensus to form. Review the data, weigh the optimism, and see how its 2 key rewards

Looking for more investment ideas beyond Klarna Group?

If Klarna Group has you rethinking your portfolio, do not stop there. Use the Simply Wall Street Screener to surface other opportunities that fit your goals.

- Spot potential income anchors for your portfolio by reviewing companies in the 9 dividend fortresses.

- Hunt for quality at a discount by scanning the 43 high quality undervalued stocks.

- Strengthen your downside protection by focusing on companies in the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.