Klarna Group (KLAR) Valuation Reassessed After IPO Lawsuits And Credit Loss Reserve Concerns

Klarna Group Plc KLAR | 13.35 | +0.53% |

Klarna Group (KLAR) is back in focus after a series of securities class action lawsuits tied to its September 2025 IPO, centered on alleged understatement of credit and loss reserve risks.

The recent wave of class action filings, together with reaction to proposals to cap credit card interest rates, has kept Klarna Group in the spotlight. The share price reflects that tension, with a 90 day share price return of a 20.5% decline versus a year to date share price return of 5.1%, suggesting momentum has been fading after a stronger start to the period.

If this kind of legal and regulatory noise has you reassessing your options, it could be a good time to broaden your search and check out fast growing stocks with high insider ownership.

With the share price down 20.5% over 90 days but still up 5.1% year to date, and analysts' targets sitting higher than the last close, you have to ask: is there real upside here or is the market already pricing in future growth?

Price-to-Sales of 3.5x: Is it justified?

With Klarna Group closing at US$30.02 and trading on a P/S of 3.5x, the shares screen cheaper than direct peers on this metric but richer than the broader US Diversified Financials industry.

P/S looks at what investors are paying for each dollar of revenue, which can be especially useful for a company that is still loss making but growing its top line.

Here, Klarna Group’s 3.5x P/S sits below the peer average of 3.8x. This suggests the market is not assigning a premium against that narrower group, even though revenue is forecast to grow 17.9% a year and earnings are expected to advance rapidly from a current loss making position.

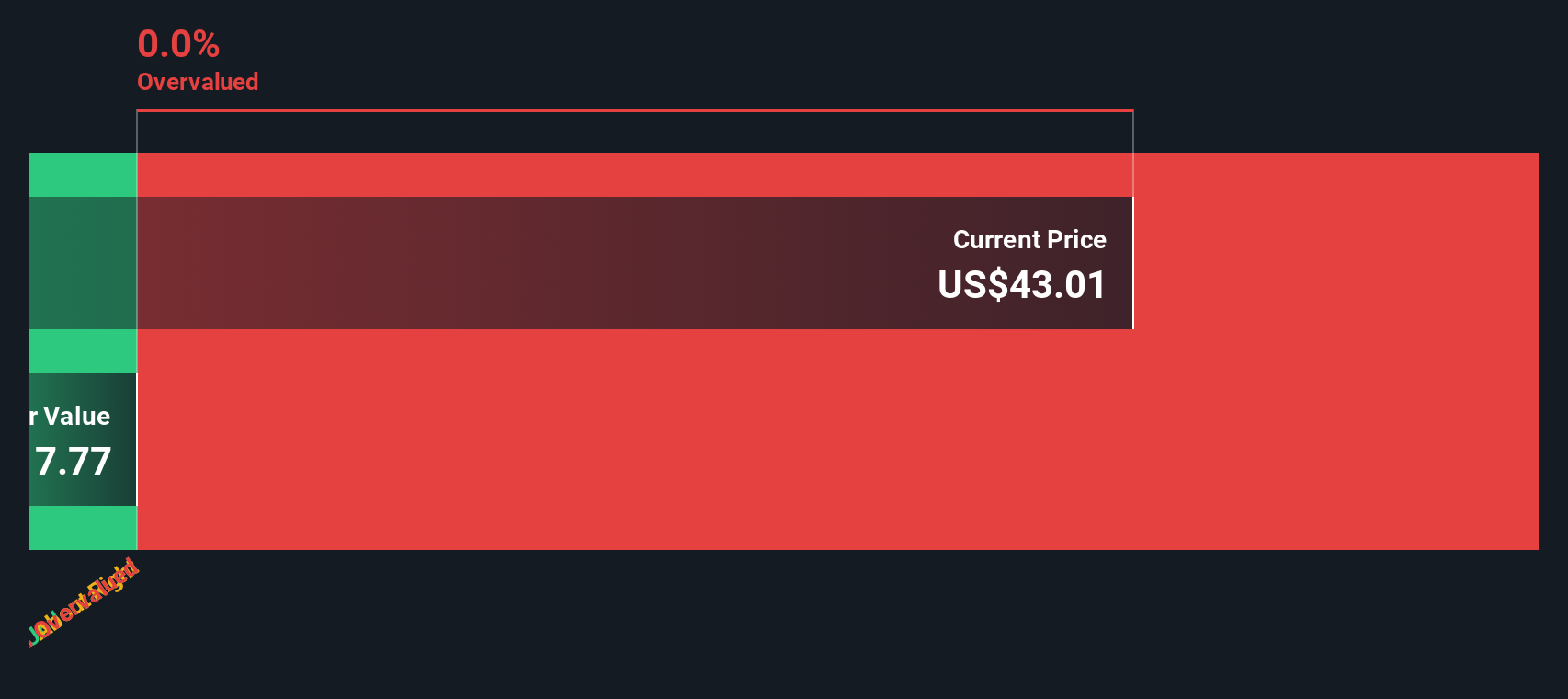

Against the wider US Diversified Financials industry, where the average P/S is 2.8x, Klarna Group trades at a clear premium. This implies investors are already paying more per dollar of sales than they do for the sector as a whole, while our DCF work indicates the shares are trading above an estimated fair value of US$15.31.

Result: Price-to-Sales of 3.5x (OVERVALUED)

However, ongoing class action lawsuits and the company’s current net loss of US$224 million could quickly change how investors view the recent valuation debate.

Another View: Our DCF Model Points Lower

While the 3.5x P/S ratio paints Klarna Group as expensive against the wider US Diversified Financials sector, our DCF model goes further. It puts fair value at US$15.31 per share versus the current US$30.02, which implies the shares are trading well above that estimate. The real question is whether you think the market is right to look past that gap.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Klarna Group Narrative

If you see the numbers differently, or simply prefer to weigh the data yourself, you can build a custom Klarna Group view in minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Klarna Group.

Looking for more investment ideas?

If Klarna Group is on your radar, do not stop there. The Simply Wall St screener can surface plenty of other possibilities that fit your style.

- Target potential value opportunities by scanning these 884 undervalued stocks based on cash flows that could offer more for every dollar you put to work.

- Ride major tech trends by zeroing in on these 25 AI penny stocks positioned around artificial intelligence themes.

- Lean into income by reviewing these 13 dividend stocks with yields > 3% that may help you build a steadier cash flow profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.