Klarna Group (NYSE:KLAR) Valuation Check As Short Term Momentum Contrasts With Weaker Year To Date Returns

Klarna Group Plc KLAR | 0.00 |

What Klarna Group’s recent performance tells you

Klarna Group (KLAR) has drawn fresh attention after a recent move in its stock price, with the share closing at US$17.47 and posting mixed short term returns despite a weaker showing year to date.

The recent 1 day share price return of 3.07% sits alongside a 30 day share price return of 21.91% and a 90 day share price return of 27.05%. The year to date share price return has declined 38.85%, suggesting shorter term momentum has picked up even as longer term performance remains weaker.

If Klarna’s move has you looking at other parts of the financial technology space, it could be a good time to scan for 20 top founder-led companies

With Klarna growing revenue and narrowing losses while trading at a discount of about 32% to the average analyst price target, you have to ask: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 59.4% Undervalued

Against Klarna’s last close of $17.47, the leading narrative on the stock pins fair value at $43.01, a sharp gap that frames a very different story from recent trading.

Klarna steps in as the bridge:

Small, Purposeful Loans: Instead of the "revolving door" of high-interest credit card debt, Klarna offers surgical, small-scale loans.

Flexible Payment Plans: By breaking a $400 purchase into four $100 payments, Klarna allows consumers to manage cash flow without the "debt hangover" typical of 20% APR cards.

According to SiwyOgon, this valuation leans heavily on Klarna turning that purchasing power engine into sustained revenue growth, rising margins and a future earnings profile more in line with established digital banks. Want to see exactly how those assumptions stack up to reach $43.01?

Result: Fair Value of $43.01 (UNDERVALUED)

However, this depends on Klarna turning current revenue growth into sustainable profits, and any setback in credit performance or regulation could quickly challenge that optimism.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

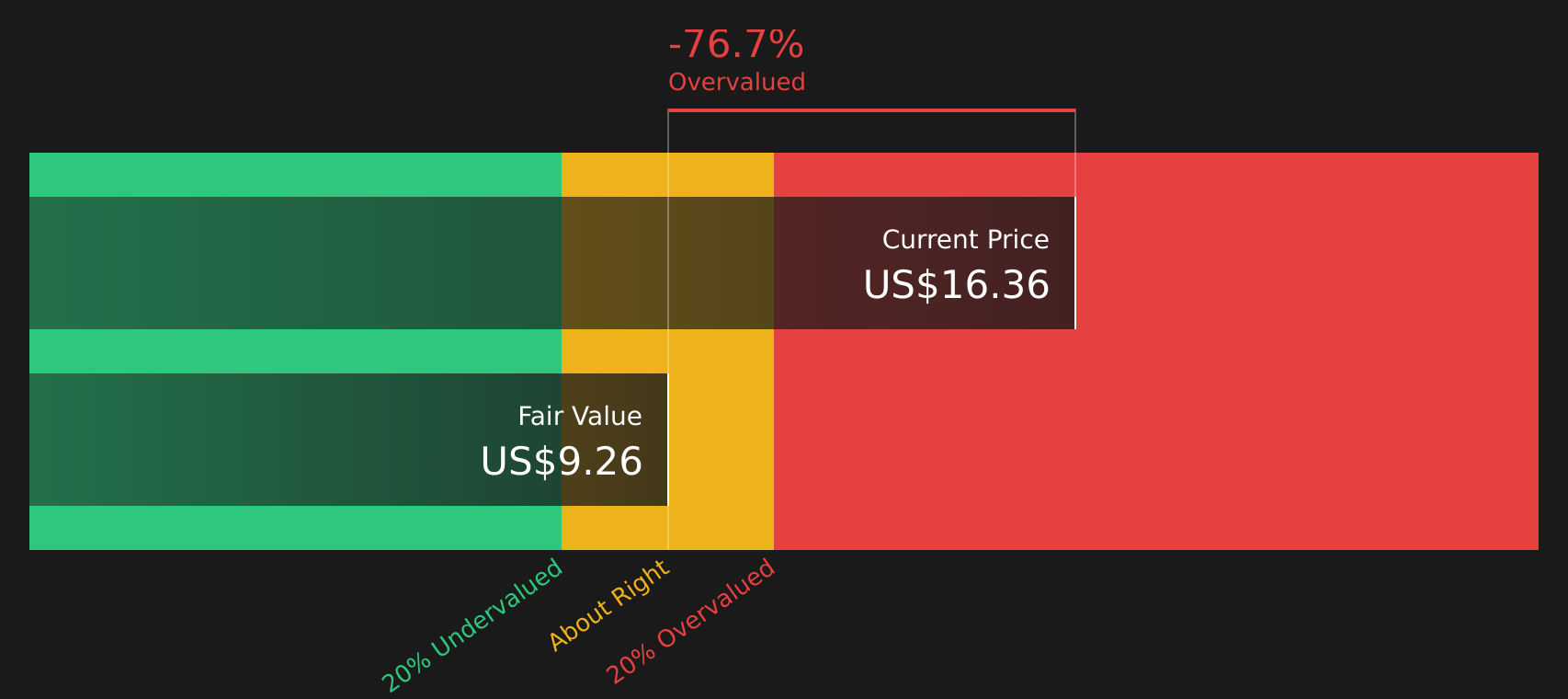

Another view on what KLAR is worth

The community narrative sees Klarna at a fair value of $43.01 and calls the stock undervalued, but our DCF model points the other way, with an estimated value of $9.25. That implies the current $17.47 price sits above this cash flow based view. Which story do you think fits better with your own expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the split between these valuation views leaves you uncertain, that is the point. Use the tools available and assess Klarna on your own terms with 2 key rewards

Looking for more investment ideas?

If Klarna has sparked fresh thinking, do not stop here. Broaden your watchlist with focused stock ideas that match how you like to invest.

- Target growth at a discount by scanning 46 high quality undervalued stocks, which combine solid foundations with prices that sit below many investors' expectations.

- Prioritise resilience by reviewing 65 resilient stocks with low risk scores, which score well on stability so short term swings are less likely to dominate your returns.

- Spot tomorrow's potential standouts early with the screener containing 22 high quality undiscovered gems before they sit firmly on every investor's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.