Klarna (NYSE:KLAR): A Fresh Look at Valuation After Stablecoin Launch and Stripe Partnership Expansion

Klarna Group Plc KLAR | 13.35 | +0.53% |

Klarna Group (NYSE:KLAR) has made headlines with the launch of KlarnaUSD, its first stablecoin. This represents a big step into the crypto space for the payments giant. This move expands its partnership with Stripe and positions Klarna among the first banks to innovate at scale in digital currencies.

Klarna’s share price tells a volatile story this year, with a sharp 22% drop over the last month and a year-to-date share price return of -32.4%. Recent momentum hints at renewed optimism, however, after Klarna’s high-profile leap into stablecoins and deeper innovation partnerships with Stripe, which are major moves that could reset perceptions of its long-term growth potential.

If Klarna’s pivot into digital payments has you looking for the next breakout opportunity, it’s a perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With valuations under pressure and new strategy plays on the table, the key question for investors now is whether Klarna is trading at a discount or if the market has already accounted for its bold push into digital assets and growth frontiers.

Price-to-Sales of 3.6x: Is it justified?

With Klarna trading at a price-to-sales (P/S) ratio of 3.6x, the stock is priced at a premium to both its industry and peer group. The current share price of $30.97 reflects this elevated multiple, which exceeds the US Diversified Financial industry average (2.5x) and the peer average (3.4x).

The P/S ratio compares a company’s market capitalization to its total revenue. This makes it a common valuation tool for high-growth or unprofitable businesses like Klarna. It signals what investors are willing to pay for each dollar of revenue generated, especially relevant in sectors where earnings are still ramping up.

For Klarna, being unprofitable but displaying annual revenue growth and narrowing losses is significant. However, the stock’s higher-than-average P/S ratio suggests that the market is pricing in ambitious growth expectations, even as some key financial figures trail sector benchmarks. Without clear evidence that Klarna’s growth will outpace its competitors, this premium may be difficult to justify.

Compared to the industry and its closest peers, Klarna’s P/S ratio stands out as expensive, and there is not currently enough data to support a higher fair value ratio. Valuation could shift if the company’s profit trajectory accelerates or if growth projections are materially upgraded. As it stands, Klarna trades at a notable premium.

Result: Price-to-Sales of 3.6x (OVERVALUED)

However, slowing revenue growth or a lack of profitability improvements could undermine bullish sentiment and put pressure on the stock’s elevated valuation going forward.

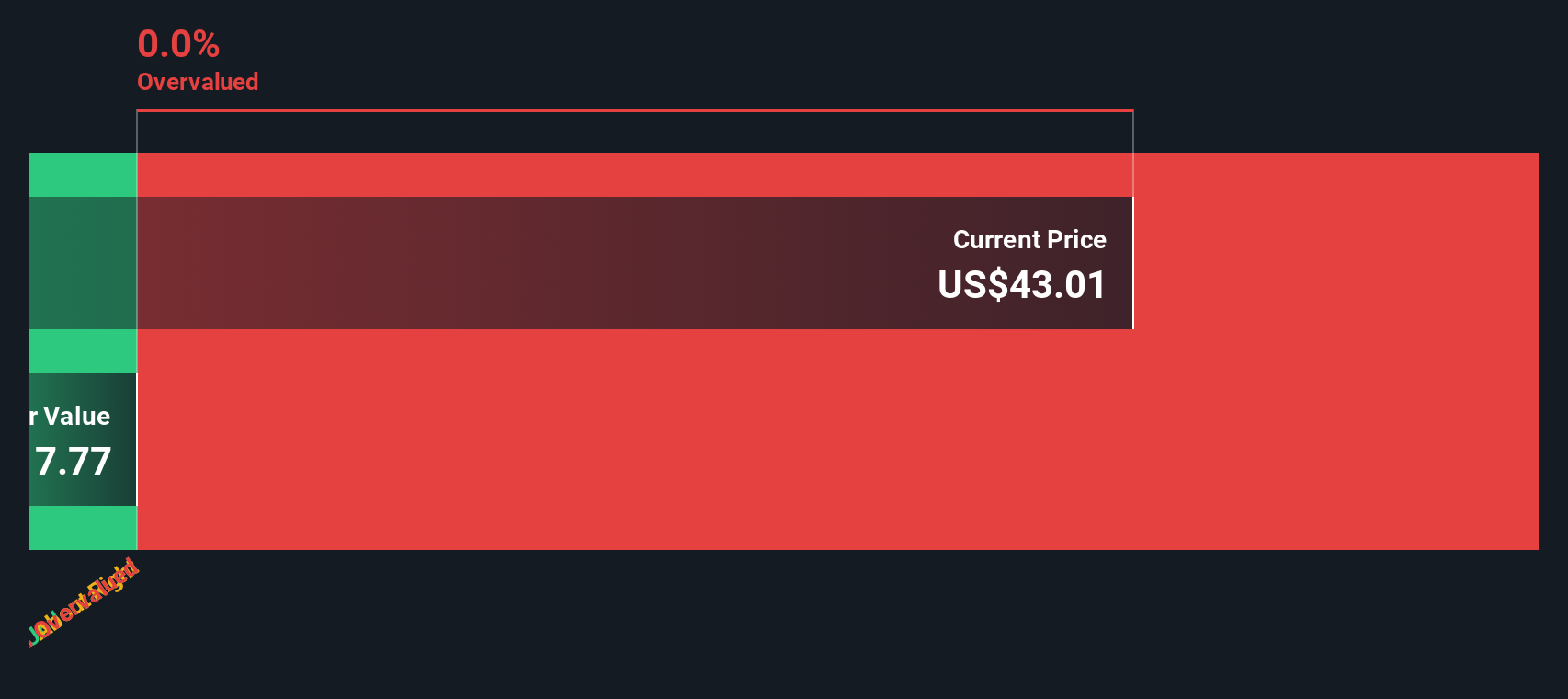

Another View: Discounted Cash Flow Paints a Starker Picture

While Klarna’s price-to-sales multiple points to an expensive valuation, our DCF model takes a very different view. Based on projected cash flows, Klarna’s intrinsic value lands at just $0.17 per share, which is dramatically lower than the current market price. Are investors being too optimistic, or is there a premium on innovation that numbers do not capture?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Klarna Group Narrative

If you see things differently or prefer hands-on analysis, you can build your own perspective on Klarna’s outlook in just minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Klarna Group.

Looking for more investment ideas?

Smart investors always stay a step ahead. Uncover opportunities you might have missed by using specialized screeners and give your portfolio the momentum it needs to grow.

- Boost your potential returns by targeting companies that are trading lower than their cash flow value with these 927 undervalued stocks based on cash flows.

- Capture tomorrow’s tech leaders by getting early access to these 25 AI penny stocks identified for innovation and growth in artificial intelligence.

- Strengthen your income stream by choosing companies offering yields above 3% through these 15 dividend stocks with yields > 3% before the market catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.