Klaviyo, Inc. (NYSE:KVYO) Shares May Have Slumped 25% But Getting In Cheap Is Still Unlikely

Klaviyo, Inc. Class A KVYO | 19.14 | -1.54% |

Klaviyo, Inc. (NYSE:KVYO) shareholders won't be pleased to see that the share price has had a very rough month, dropping 25% and undoing the prior period's positive performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 41% in that time.

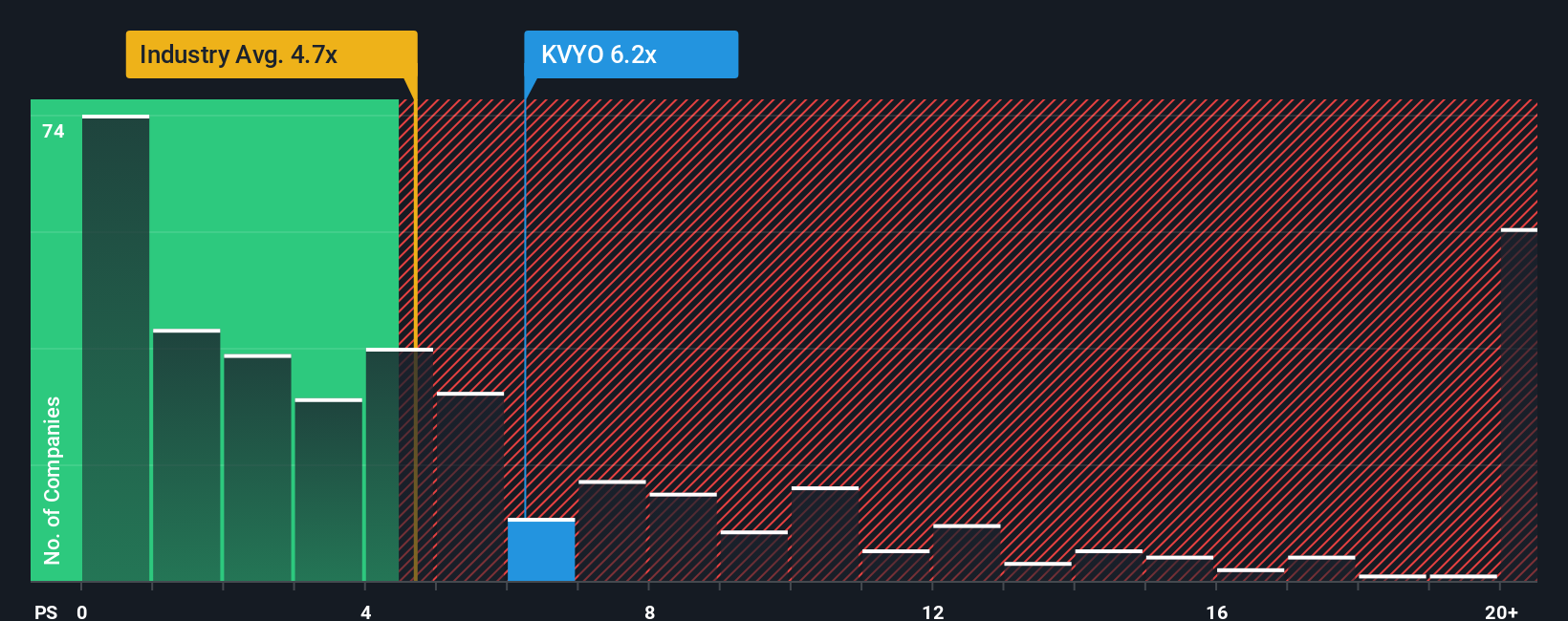

In spite of the heavy fall in price, Klaviyo's price-to-sales (or "P/S") ratio of 6.2x might still make it look like a sell right now compared to the wider Software industry in the United States, where around half of the companies have P/S ratios below 4.7x and even P/S below 1.9x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

What Does Klaviyo's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Klaviyo has been doing relatively well. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Klaviyo's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Klaviyo would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered an exceptional 33% gain to the company's top line. The latest three year period has also seen an excellent 144% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 21% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 33% per annum growth forecast for the broader industry.

With this information, we find it concerning that Klaviyo is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Klaviyo's P/S

There's still some elevation in Klaviyo's P/S, even if the same can't be said for its share price recently. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

It comes as a surprise to see Klaviyo trade at such a high P/S given the revenue forecasts look less than stellar. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Klaviyo with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.