Klaviyo (KVYO) Valuation Check As New AI Integrations Deepen Its Marketing And Personalization Toolkit

Klaviyo, Inc. Class A KVYO | 19.14 | -1.54% |

Klaviyo (KVYO) is back in focus after launching a Klaviyo app in ChatGPT and welcoming Wunderkind to its marketplace, a pair of AI focused integrations that sharpen its marketing data and personalization toolkit.

These AI integrations arrive after a tough stretch for the stock, with a 7 day share price return of a 13.31% decline, a 30 day share price return of a 31.60% decline and a 1 year total shareholder return of a 51.73% decline. This suggests recent momentum has been fading even as Klaviyo leans harder into AI centric products.

If this kind of AI themed update has your attention, it could be a good moment to look beyond a single name and scan high growth tech and AI stocks for other ideas in the space.

With Klaviyo shares around US$22.21 and a value score of 3, plus a wide gap to the US$43.39 analyst target, you have to ask: is this a mispriced AI marketing platform, or is the market already baking in future growth?

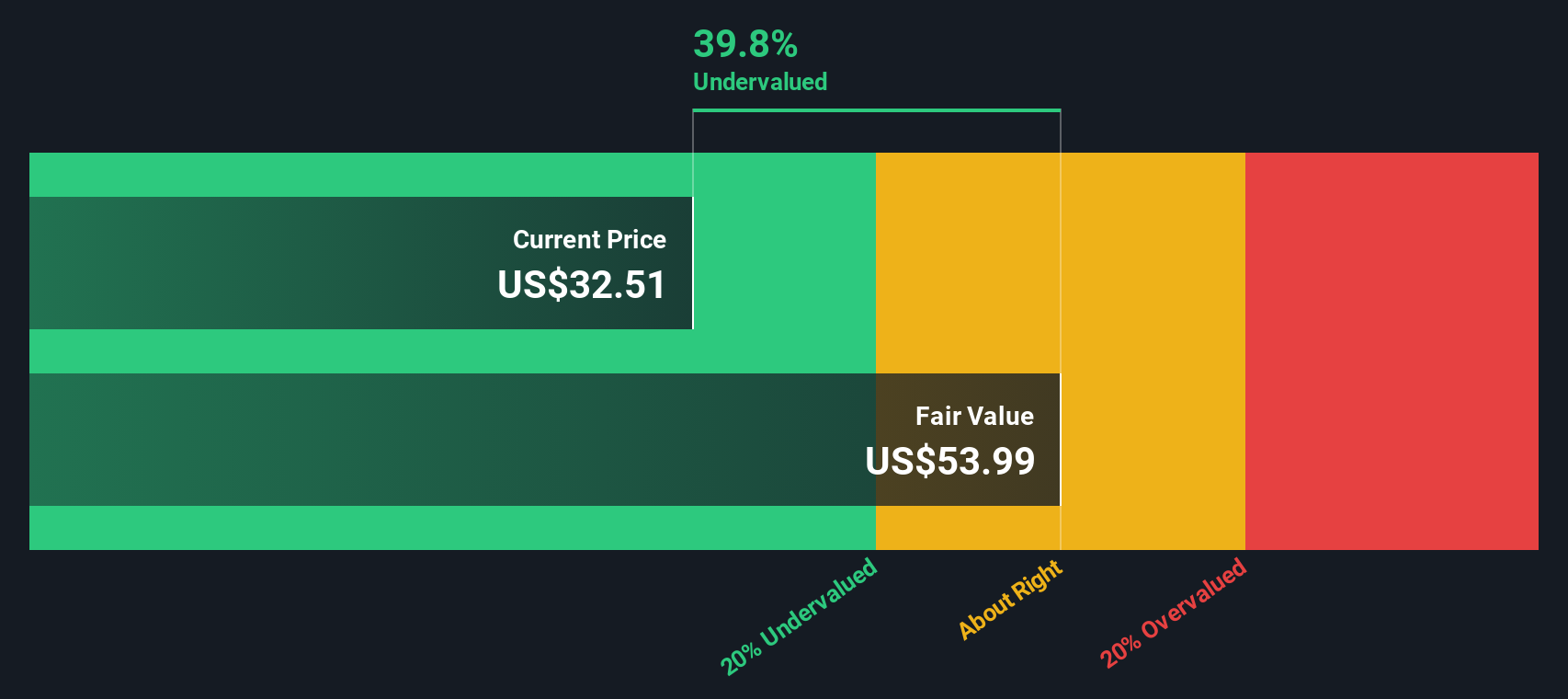

Most Popular Narrative: 48.7% Undervalued

At a last close of $22.21 versus a narrative fair value of $43.30, Klaviyo screens as materially cheaper than the story its followers are pricing out.

The rapid innovation and rollout of new AI first products including Conversational Agent, Helpdesk, and analytics expands Klaviyo's addressable market from just marketing automation into broader B2C CRM and customer service, setting up significant opportunities for higher ARPU and long term revenue growth.

Want to see what justifies that higher fair value line? The narrative leans on steady revenue compounding, rising margins, and a future earnings profile that assumes much richer profitability. Curious how those moving parts stack up over time and what kind of earnings multiple ties it all together?

Result: Fair Value of $43.30 (UNDERVALUED)

However, that upbeat story still leans heavily on new AI products gaining real traction, and on competition from larger software suites not squeezing Klaviyo's pricing power.

Another Angle on Value: Cash Flows Tell a Tougher Story

That $43.30 fair value narrative presents Klaviyo as undervalued. Our DCF model, however, comes out closer to $11.64 per share, which puts the current $22.21 price well above its estimated future cash flow value. If cash actually matters more than the story, how much weight do you give this gap?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klaviyo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Klaviyo Narrative

If you see the data differently or prefer to test your own assumptions, you can plug in your views and build a full Klaviyo story in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Klaviyo.

Ready for more investment ideas?

If Klaviyo has you thinking about what else might be out there, do not stop at one ticker. Put a few focused shortlists to work for you.

- Scan for potential income candidates by checking out these 14 dividend stocks with yields > 3% that may suit a yield focused watchlist.

- Hunt for growth stories in cutting edge automation and machine learning with these 25 AI penny stocks that fit your risk and return preferences.

- Add a different angle to your research by reviewing these 18 cryptocurrency and blockchain stocks that connect listed companies to digital assets and blockchain themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.