Klaviyo’s Enterprise AI Push Reshapes Growth Story And Valuation Debate

Klaviyo, Inc. Class A KVYO | 19.14 | -1.54% |

- Klaviyo (NYSE:KVYO) is expanding rapidly in the enterprise market, with a sharp rise in high-value customers.

- The company is rolling out advanced AI agents that support more autonomous customer experiences.

- Doubled million dollar ARR accounts and growing enterprise adoption suggest a meaningful shift in its business mix.

Klaviyo, known for its marketing automation and customer data platform tools, is pushing further into larger enterprise accounts as retailers and brands seek more automated engagement with their customers. The new AI agents sit on top of Klaviyo's existing workflows and data capabilities, aiming to handle more decisions and actions without constant human input.

For you as an investor, these moves raise questions about how far Klaviyo can extend beyond its roots in small and mid sized ecommerce brands. The combination of more enterprise exposure and heavier AI usage could reshape how the company competes with larger marketing and CRM platforms, and may influence how investors assess its long term business mix and risk profile.

Stay updated on the most important news stories for Klaviyo by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Klaviyo.

Quick Assessment

- ✅ Price vs Analyst Target: Shares trade at US$18.60 versus an analyst consensus of US$33.59, roughly 44% below that target.

- ✅ Simply Wall St Valuation: The stock is described as trading 30.5% below an estimated fair value, which screens as undervalued in this model.

- ❌ Recent Momentum: The 30 day return is about 22% lower, so the price has been under pressure despite the enterprise and AI news.

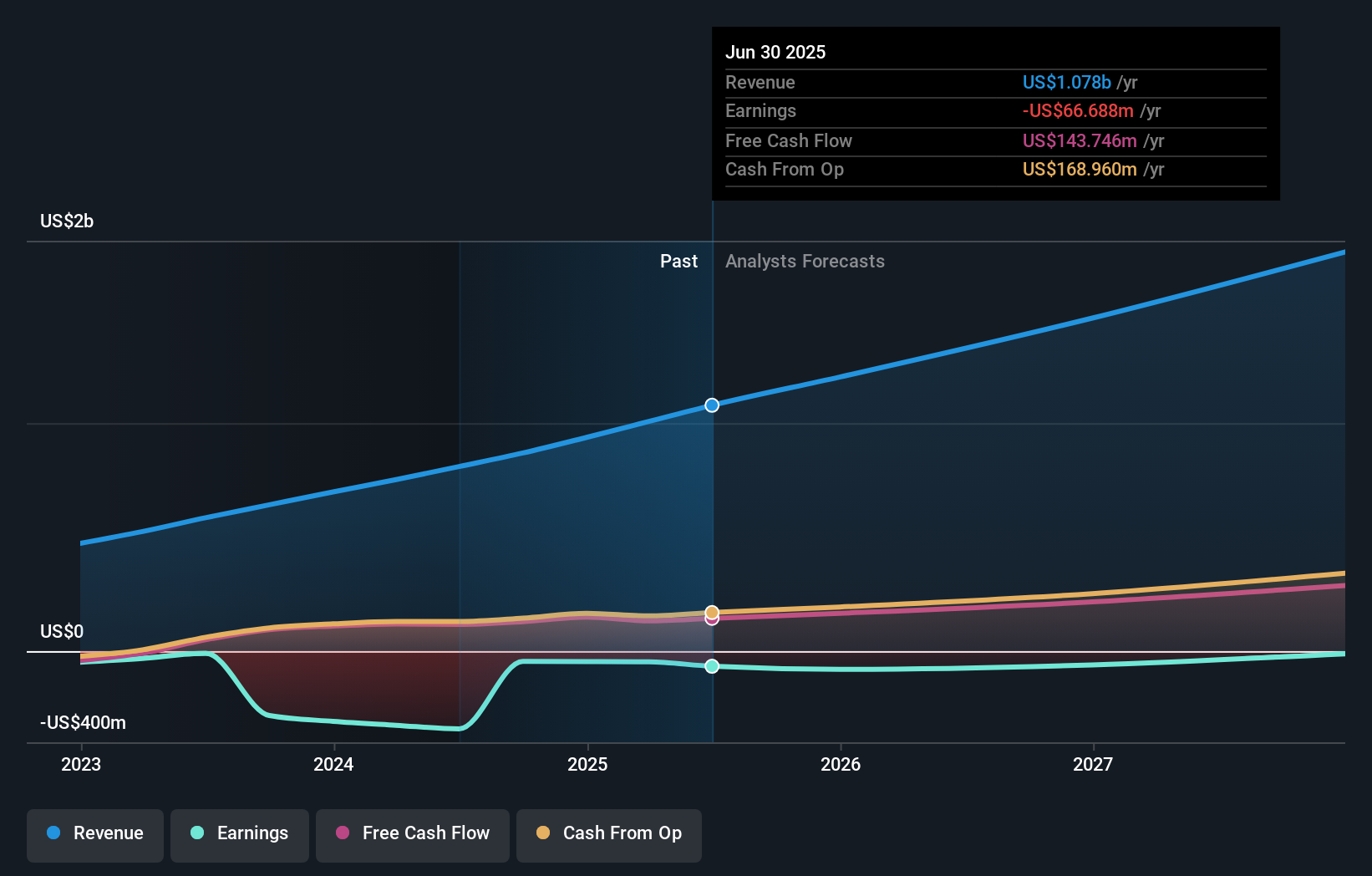

There is only one way to know the right time to buy, sell or hold Klaviyo. Head to Simply Wall St's company report for the latest analysis of Klaviyo's Fair Value.

Key Considerations

- 📊 Enterprise expansion and AI agents suggest a bigger role in higher value accounts, which could change how you think about Klaviyo's revenue mix and customer concentration.

- 📊 With a P/E of 178.4 and a forward P/E of 157.6, many investors will watch whether earnings and AI driven products keep pace with expectations at the current US$18.60 price.

- ⚠️ Rapid AI rollout and a stronger push into large enterprises can bring execution risk if product performance or customer adoption does not track current enthusiasm.

Dig Deeper

For the full picture including more risks and rewards, check out the complete Klaviyo analysis. Alternatively, you can check out the community page for Klaviyo to see how other investors believe this latest news will impact the company's narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.