Kohl’s Stock Rally Puts LVMH Target And Macy’s In Focus

Macy's, Inc. M | 0.00 |

Department store stocks are back in the spotlight after Kohl’s share price climbed more than 130% over the past year, helped by early signs of a turnaround and fresh interest from investors. For you as a retail investor, this kind of reset in value driven retail can punish weaker competitors and create openings for stronger operators or key partners. This article breaks down three stocks exposed to the same news catalysts as Kohl’s, showing one that may be benefiting from the shift and two that could face tougher questions as middle income shoppers reassess where they spend.

LVMH Moët Hennessy - Louis Vuitton Société Européenne (ENXTPA:MC)

Overview: LVMH Moët Hennessy - Louis Vuitton Société Européenne is a Paris based luxury group that owns a wide portfolio of premium brands across fashion and leather goods, perfumes and cosmetics, wines and spirits, watches and jewelry, selective retailing and hospitality.

Operations: LVMH generates most of its revenue from Fashion and Leather Goods at €37.8b, followed by Selective Retailing at €18.3b, Watches and Jewelry at €10.5b, Perfumes and Cosmetics at €8.2b and Wines and Spirits at €5.4b, with the United States and Asia (excluding Japan) among its largest regional contributors.

Market Cap: €246.1b

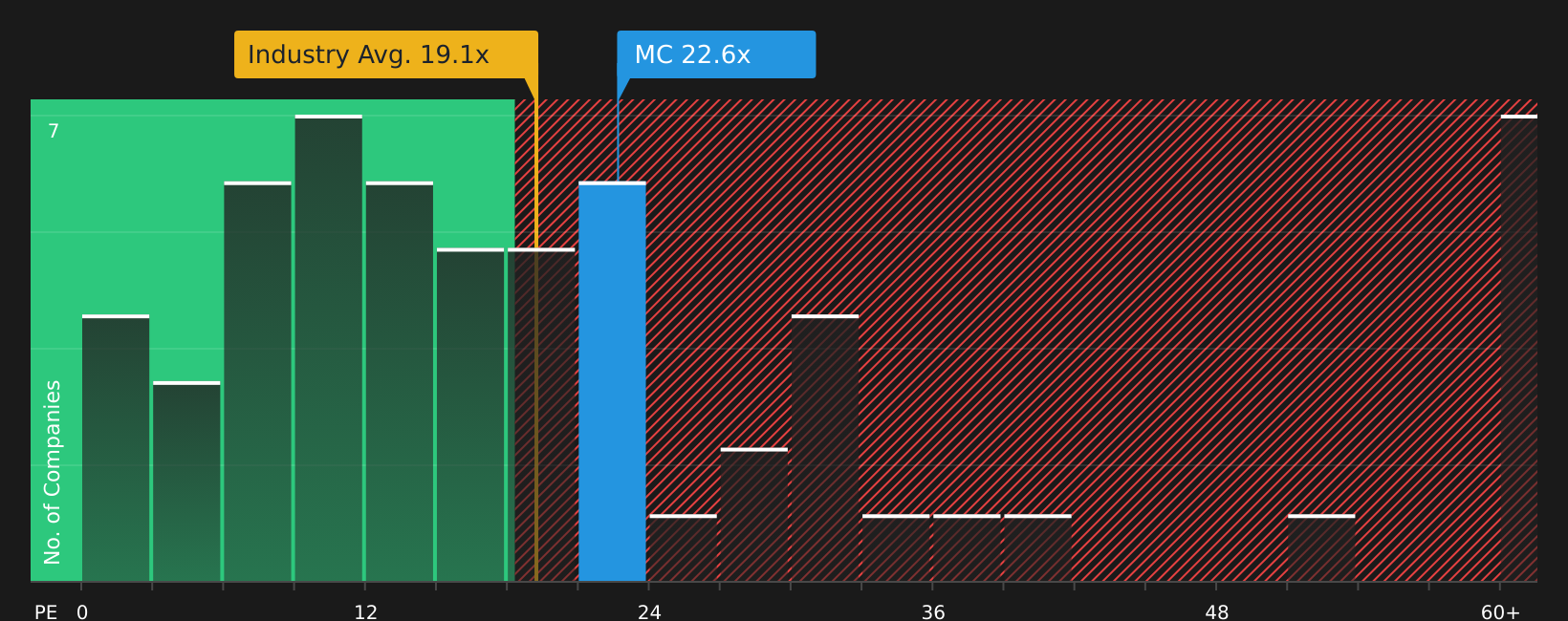

LVMH stands out in this department store themed screen because it not only supplies Sephora shop in shops inside Kohl’s, it also fully controls the underlying beauty retailer, giving it a direct link to any improvement in foot traffic and beauty spend. The group combines powerful brands with a wide reach across the US and Asia, but investors still have to weigh moderate earnings growth forecasts, a P/E that screens slightly above some fair value estimates and a funding structure that leans on external borrowing. At the same time, its scale in selective retailing, active portfolio moves around businesses like Fenty Beauty, and ongoing cash returns keep LVMH firmly on the radar of investors watching value driven retail shifts.

LVMH’s grip on beauty and luxury is strong, but its slightly rich P/E and reliance on external funding raise questions about what the market is really pricing in. As a result, it is worth scanning the 2 key rewards and 1 important warning sign

Target (TGT)

Overview: Target is a large U.S. general merchandise retailer that combines big box stores with a strong online offering, selling everything from apparel and beauty products to groceries, home goods, electronics, and everyday essentials under both national and owned brands.

Operations: Target generates all of its US$106.4b in annual revenue from U.S. retail operations, with all sales coming from its domestic market.

Market Cap: US$63.4b

Target sits in direct competition for the same value focused middle income shopper that Kohl’s is trying to win back, which means an improved Kohl’s experience could siphon off exactly the customer traffic Target is counting on to revive its own sales. At the same time, analysts and management are describing a multi year turnaround, while recent history includes weaker discretionary demand, margin pressure, high leverage, and meaningful insider selling that point to execution and balance sheet risk. With the stock already screening as fairly valued on cash flow estimates and growth forecasts that are modest, investors may want to assess whether recent enthusiasm is running ahead of what Target can realistically deliver before giving it significant weight in a turnaround oriented portfolio.

Target’s turnaround story looks energetic, yet high leverage, modest growth expectations and insider selling suggest some investors may be missing a key tension in the setup. It is worth reading the 4 key rewards and 2 important warning signs

Macy's (M)

Overview: Macy's is a long established U.S. retailer that runs Macy's, Bloomingdale's and Bluemercury stores, websites and apps, selling apparel, accessories, cosmetics, homewares and other goods to a broad consumer base.

Operations: Macy's generates about US$22.7b in revenue from its department store retail business, all of which comes from the United States.

Market Cap: US$6.8b

Investors looking at Macy's are getting a classic department store turnaround with a twist, as omni channel upgrades, the Reimagine 125 store program and stronger Bloomingdale's and Bluemercury trends coincide with forecasts for revenue to decline about 4.6% a year and only modest earnings growth. The stock screens as inexpensive on earnings and cash flow estimates; yet management is closing roughly 150 stores, dividend history is unstable, insider selling has been meaningful and all liabilities are funded by external borrowing, which raises funding and income risk if consumer demand weakens. Put simply, Macy's may appear to some investors as a value play on the surface, but the mix of shrinking top line expectations and structural pressure on physical retail suggests the margin for error is thin.

Macy's turnaround pitch looks inexpensive on the surface, yet shrinking revenue expectations and full reliance on external borrowing could be masking a deeper pressure point. Get the context behind that tension in the 3 key rewards and 2 important warning signs

Take Control of Your Investment Journey

If Target or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves

Fresh stock ideas can break out fast, and by the time momentum is flying, the best entry points are often gone. Scan what others miss while it matters, act now.

- Spot resilient income plays before yields get compressed by latecomers by scanning the 487 dividend fortresses built to highlight companies that aim to combine strong payouts with stability.

- Chase early momentum in companies riding the AI build out using the curated 51 AI infrastructure stocks so you see potential beneficiaries of rising compute demand while they are under the radar for now.

- Track potential compounding stories with solid finances through the carefully filtered 199 high quality undervalued stocks and avoid getting caught chasing stocks after the market has already repriced them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.