L3Harris Technologies (LHX) Valuation Check After Major Missile Contract Wins And Record Backlog

L3Harris Technologies Inc LHX | 356.00 | +0.59% |

L3Harris Technologies (LHX) is back in focus after confirming it has fully executed a multi year share repurchase program and filed a mixed securities shelf registration, a combination that reshapes its capital flexibility.

The latest buyback completion and new shelf registration come after a strong run, with a 90 day share price return of 20.09% and a 1 year total shareholder return of 78.19%. This suggests momentum has been building around L3Harris as its contract wins, record fuze production and backlog progress feed into investor sentiment.

If you are looking for other defense related opportunities as capital markets activity picks up, our screener of 25 power grid technology and infrastructure stocks is a useful way to spot companies tied to critical infrastructure themes.

With the stock up sharply and trading at roughly a 9% intrinsic discount and about 11% below the average analyst target, the real question now is whether L3Harris is still mispriced or if the market is already factoring in future growth.

Most Popular Narrative: 9.2% Undervalued

L3Harris Technologies' most followed narrative pegs fair value at about $380.63, above the last close of $345.50. This sets up a clear valuation gap for investors to scrutinize.

Analysts expect earnings to reach $2.7 billion (and earnings per share of $15.25) by about September 2028, up from $1.7 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $2.0 billion.

The key question is what earnings path supports that higher fair value tag. The narrative focuses on steady revenue gains, firmer margins and a thinner share count to bridge the gap between the current price and the implied valuation.

Result: Fair Value of $380.63 (UNDERVALUED)

However, that gap could close quickly if U.S. budget debates, fixed price contract pressures, or missile spinout execution issues unsettle earnings expectations and sector sentiment.

Another Way To Look At The Price

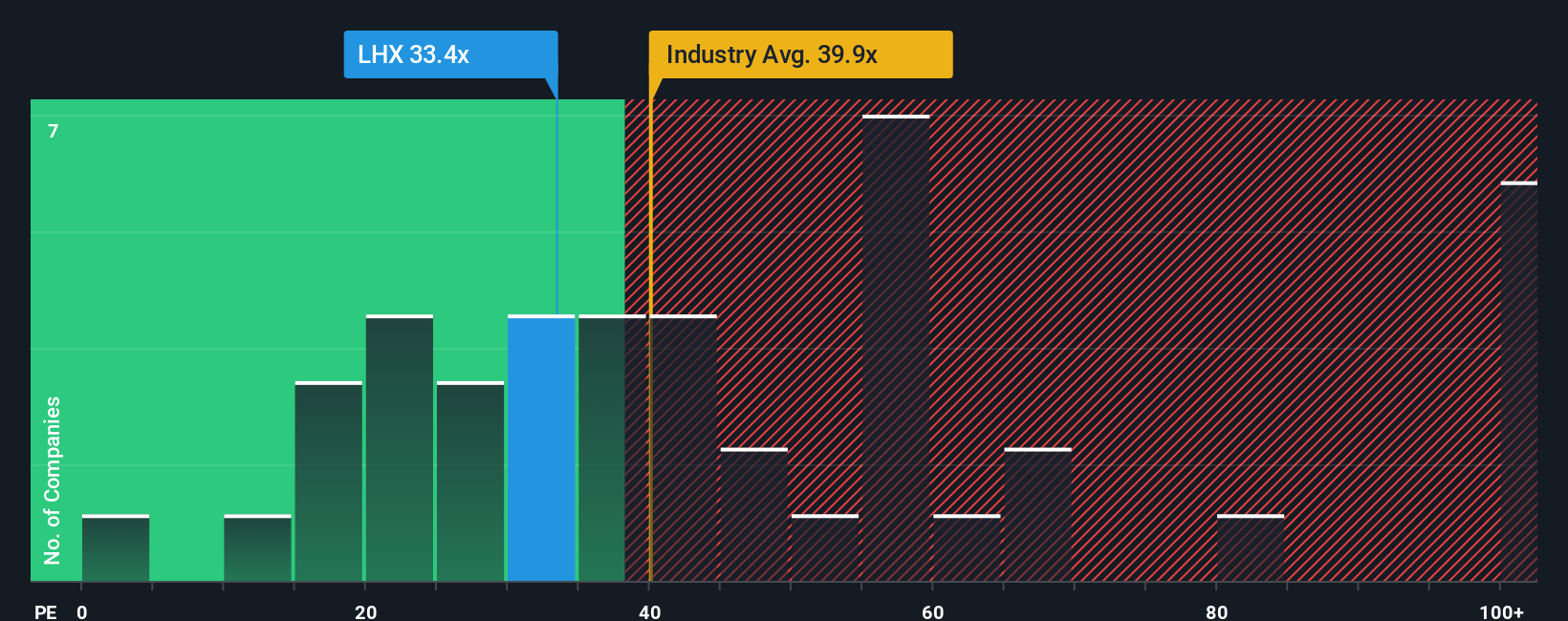

On earnings multiples, the picture looks less forgiving. L3Harris trades on a P/E of 40.2x, slightly above peers at 38.2x and well above its fair ratio of 33.4x. This points to a richer tag than the previous 9.4% DCF based undervaluation suggests. Is the premium justified in your view?

Build Your Own L3Harris Technologies Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a custom L3Harris view in just a few minutes by starting with Do it your way.

A great starting point for your L3Harris Technologies research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready To Find Your Next Idea?

If you stop with just one stock, you could miss opportunities sitting in plain sight. Use the Simply Wall St screener to cast a wider net with focus.

- Target quality at a discount by checking companies our screener tags as 53 high quality undervalued stocks and compare how their fundamentals stack up against your watchlist.

- Secure your income stream by spotting potential yield opportunities in our list of 12 dividend fortresses that stand out for their payout profiles.

- Protect the downside first by starting with our 84 resilient stocks with low risk scores and see which names look resilient on key risk and balance sheet checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.